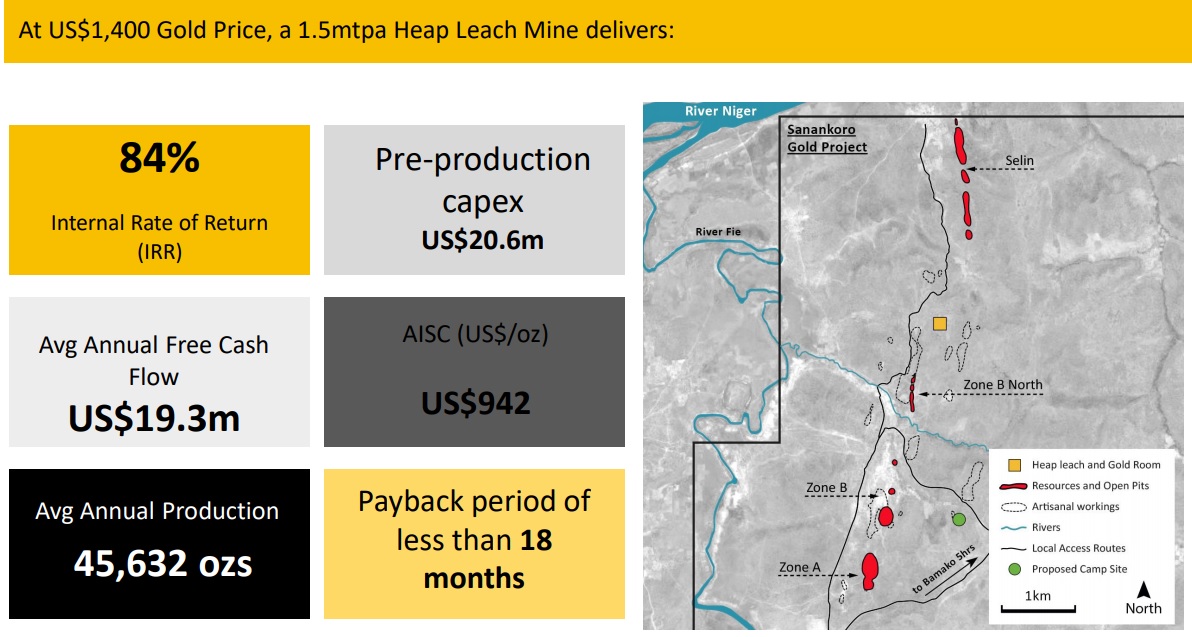

Cora Gold (CORA.L) has released the outcome of a scoping study it conducted on its 95% owned Sanakoro permit. We noticed the company doesn’t mention the traditional 10% stake the Malian government takes in gold mining projects so although Cora Gold has the option to purchase the remaining 5% of the Malian subsidiary that owns the project (for US$1M), we will assume Cora Gold will end up with an effective 90% economic interest in the project.

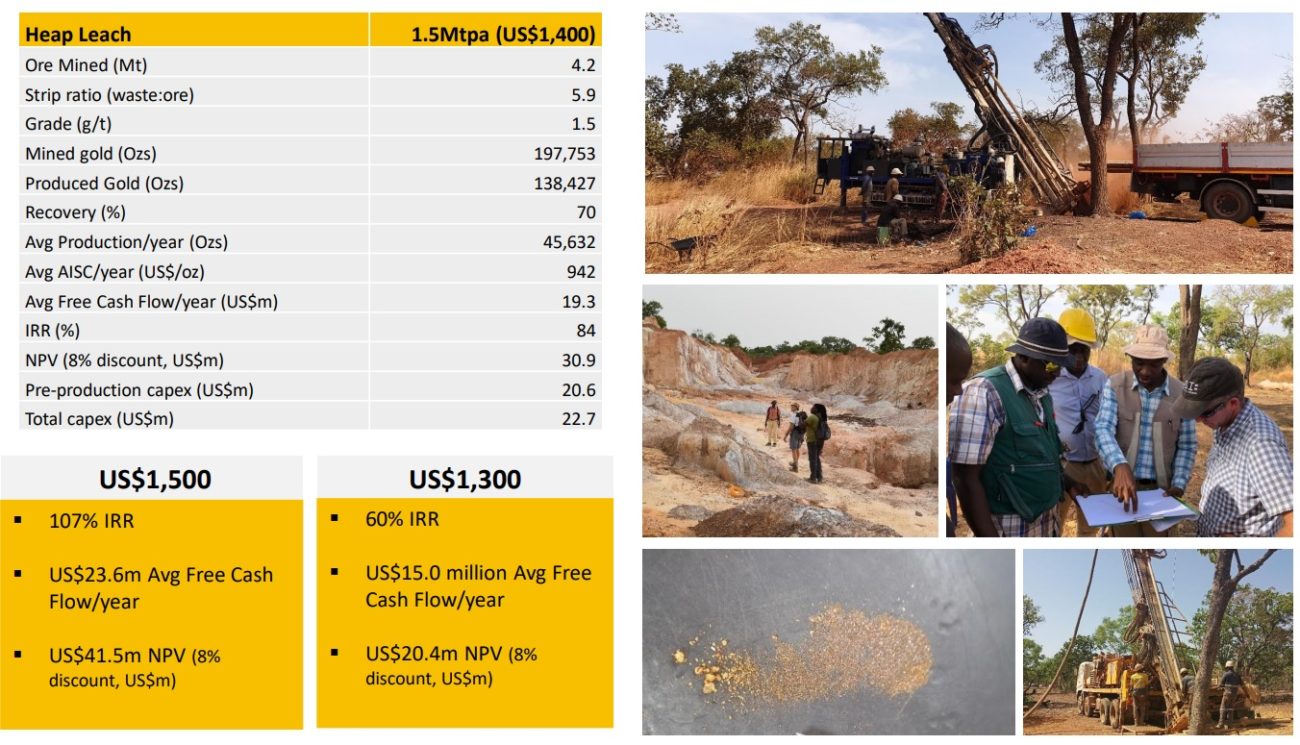

We have to admit the Cora Gold press release is quite detailed (as we aren’t used to such a level of detail for scoping study results of UK based companies). And there is plenty to be proud about. The mine plan calls for an average production rate of just over 45,000 ounces of gold per year that could be produced at an all-in sustaining cost of US$942/oz and a payback period of less than 18 months considering the initial capex is estimated at just below US$21M. The average recovery rate appears to be very high for a simple heap leach operation as Cora Gold estimates 91-95% of the gold could be recovered.

The initial NPV of US$31M might seem low as the mine life is currently just 3 years, producing 138,000 ounces of gold from the 198,000 ounces that will be in the ore that will be mined, but Cora Gold confirms it has explored just 25% of the strike length and SRK, its independent consultant, has been guiding for an exploration target of 1-2 million ounces of gold to a depth of just 100 meters (as Cora Gold is predominantly interested in the oxide zones at Sanankoro). Adding to the resources could have a positive impact on the economics as well as the current mine plan envisages a strip ratio of 5.9 which is quite high. Bringing the strip ratio down to 4 and cutting the mining cost by 5% while maintaining the same average grade would reduce the mining cost per tonne by over 30%.

It’s a small operation which means Cora Gold will have no margin of error for teething problems during the first few months of the mine life, so perhaps it is a good idea for the company to first explore for additional tonnes/gold to extend the mine life and then subsequently use those parameters for an updated economic study. The scoping study is a good start, but nothing more than just ‘a start’ for Sanankoro.

Disclosure: The author has no position in Cora Gold.