Earlier this summer, Voyager Metals (VONE.V) released the results of the Preliminary Economic Assessment on its flagship Mont Sorcier iron ore – vanadium project. The mine plan now consists of a 21 year mine life with an average production of roughly 5 million tonnes of iron ore concentrate with a grade of 65% with a 0.52% V2O5 content in the concentrate.

Using a base case price of US$100/t for the benchmark 62% Fe product and an effective price of US$120/t for the 65% product and including a $15/t credit for the vanadium content, the after-tax NPV8% came in at US$1.6B with an Internal Rate of Return of approximately 43%. The initial capex is estimated at US$574M, including about US$118M in contingency.

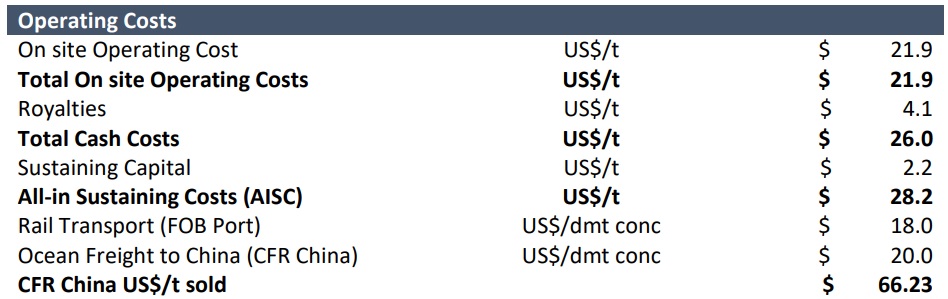

A very interesting base case scenario, as Voyager estimates its production costs (including the transportation cost to ship the concentrate to China) will be just US$66/t resulting in a net margin of approximately $69/t.

That sounds good, but there are a few rather optimistic assumptions. Voyager’s consultants used a $20/t shipping cost to China and that’s rather optimistic. Most shipping routes from the Americas to China use the C3 Tubarao shipping cost and that benchmark has been pretty volatile lately (while the C3 cost is just $18/t right now, it exceeded $30/t just a few weeks ago). Additionally, the shipping cost is based on a dry metric tonne while the company will ship a wet metric tonne so using $20/dmt basically represents about $22 per wet metric tonne.

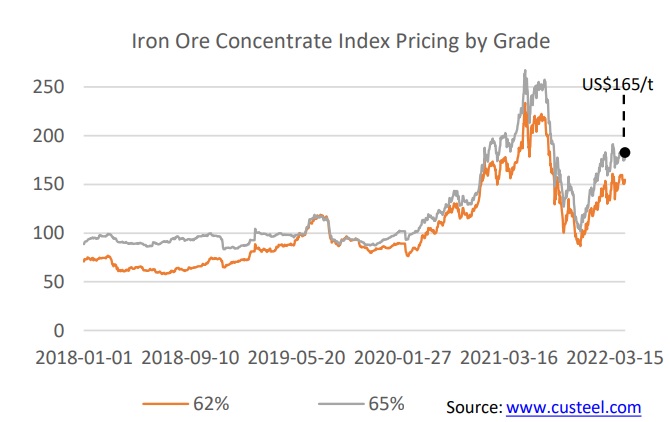

Secondly, the base case iron ore price scenario is just applying the current price. Right now, the spot price for 65% product is US$114/t as the premiums for the 3% higher Fe content has decreased so while using US$120/t can easily be justified, do keep in mind the base case scenario already includes a small premium to the spot price. The iron ore price chart shown in the corporate presentation (above) is ‘conveniently’ cut off in March when iron ore was trading almost 50% higher than where it is trading at right now. A 10% reduction in the iron ore price based on the 62% benchmark would result in an average realized price of US$110/t, resulting in an after-tax NPV8% of US$1.26B.

Disclosure: The author has no position in Voyager Metals. Please read our disclaimer.