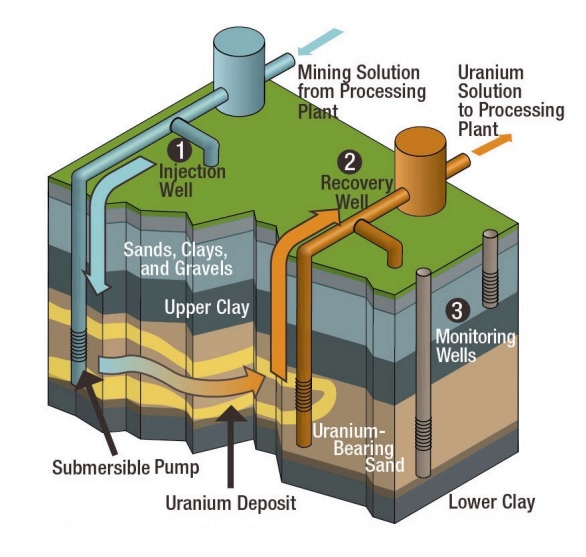

Azarga Uranium (AZZ.TO) continues to work on its flagship Dewey Burdock ISR uranium project in South Dakota and has now published the results of a Preliminary Economic Assessment on the project.

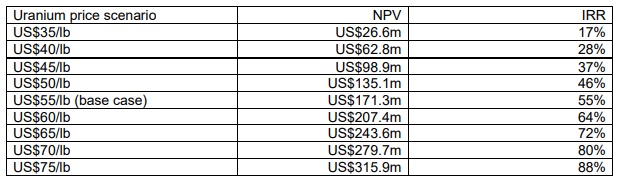

A total of 14.3 million pounds of uranium is expected to be recovered over a 16 year mine life, and the average production rate of 1 million pounds per year will be achieved in the third year of operations. With a low capex (US$32M) and low opex (a direct production cost of just below US$10.5 per pound), the economics are acceptable with an after-tax IRR of 50% and NPV8% of US$147.5M, but keep in mind the company used a $55 uranium price as its base case scenario. Unfortunately the company has not published a sensitivity analysis of the after-tax NPV and IRR, but looking at the pre-tax numbers, the NPV should still be (barely) positive at $35 uranium while maintaining a 17% IRR.

Additionally, Azarga confirmed the Atomic Safety and Licensing Board in the US has issued its Final Initial Decision on the Dewey Burdock project, 4 years after the Partial Initial Decision making the project now contention free.

As of the end of September, Azarga had a working capital deficit of approximately US$0.6M but the expected cash income of US$230,000 related to the sale of its 93% owned UrAsia subsidiary combined with the removal of US$335,000 of current liabilities that were part of the Kyrgyz subsidiary will almost make the working capital deficit disappear and the year-end working capital deficit will depend on Azarga’s Q4 expenses. Azarga will very likely have to tap the equity markets again in Q1 2020 and the results of the PEA and the ASLB decision should help the company to drum up interest.

Disclosure: The author has a long position in Azarga Uranium