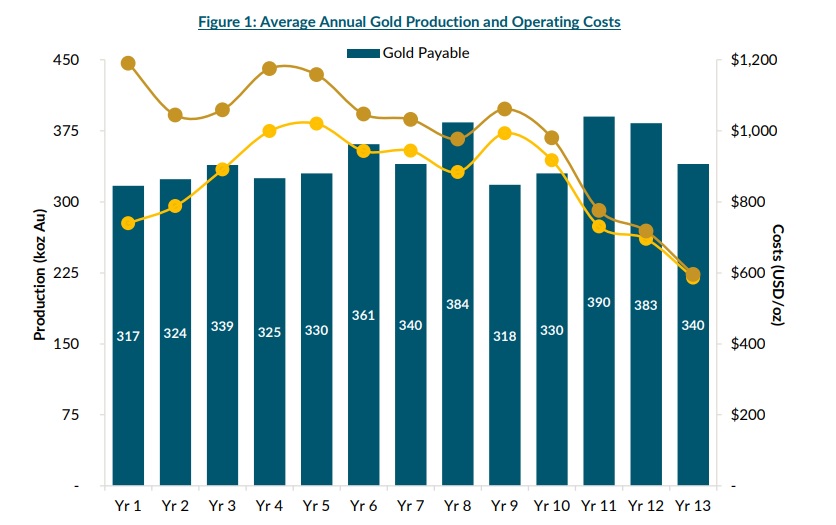

G Mining Ventures (GMIN.TO) has been active in September, as the company acquired the CentroGold project from BHP (BHP), but the company also published the results of a preliminary economic assessment on its Oko West gold project in Guyana. The study focuses on a pretty large scale operation with an initial capex of $936M (and almost $540M in sustaining capex), which should deliver an annual output of 353,000 ounces of gold for a period of just under 13 years. The anticipated all-in sustaining cost is low, at just $986/oz.

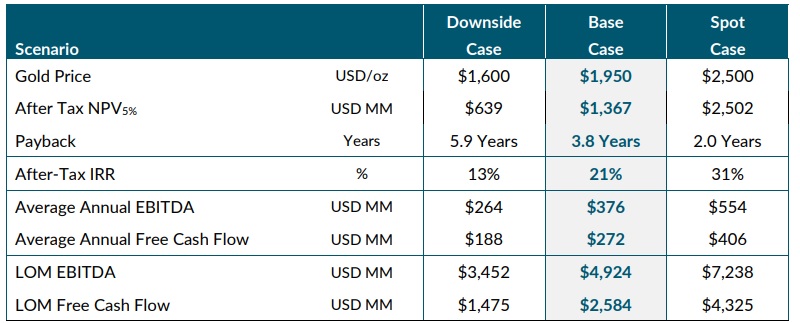

At a gold price of $1950/oz, this results in an after-tax NPV5% of $1.4B and an IRR of 21%, which is perhaps a bit on the lower end of the spectrum, but the sensitivity analysis shows the project offers quite a bit of leverage to the current gold price. At $2500 gold, for instance, the after-tax NPV5% increases to $2.5B while the IRR jumps to in excess of 30%. While of course pretty much every gold project should work well at $2500 gold, even at a more reasonable gold price of $2200/oz, the after-tax NPV5% is approximately $1.9B with a 26% after-tax IRR.

Disclosure: The author has no position in G Mining Ventures. Please read the disclaimer.