Last month, Granite Oil (GXO.TO) provided an updated reserve estimate, and it was great to see the company was able to add 190% of its production level back to the 2P reserves. These 2P reserves now contain 18.65 million barrels oil-equivalent, of which approximately 80% is real oil.

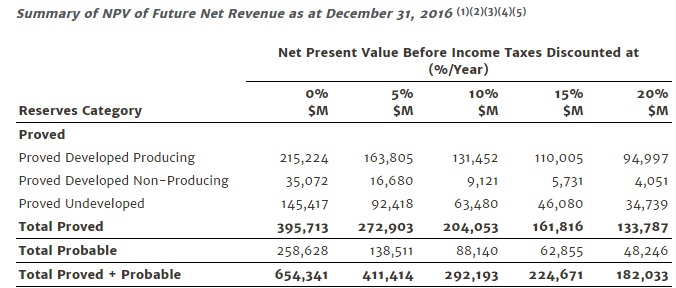

The PV10 value (pre-tax) is approximately C$292M, but we would like to use the given sensitivity table a little bit more nuanced. We will value the PDP (Proved Developed Producing) at the PV5%, the remaining proved reserves (developed and undeveloped) using a discount rate of 10%, whilst using a discount rate of 15% for the probable reserves.

Using this alternative method, the total PV value of the anticipated cash flows from the proved reserves comes in at C$236M, and on a 2P basis, the total value is approximately C$299M. That’s actually slightly higher than using the PV10 value for all reserve categories, thanks to the high ratio of PDP reserves versus 2P reserves.

Based on the company’s net debt of C$32M, the PV per share is approximately C$7.85, so Granite is currently trading relatively cheap based on these metrics as Granite Oil is a low-cost producer. We are also looking forward to see Jericho Oil’s (JCO.V) updated reserve update and PV-10 results, which should be released any day now!

The author holds a long position in all stocks mentioned in this article. Please read the disclaimer