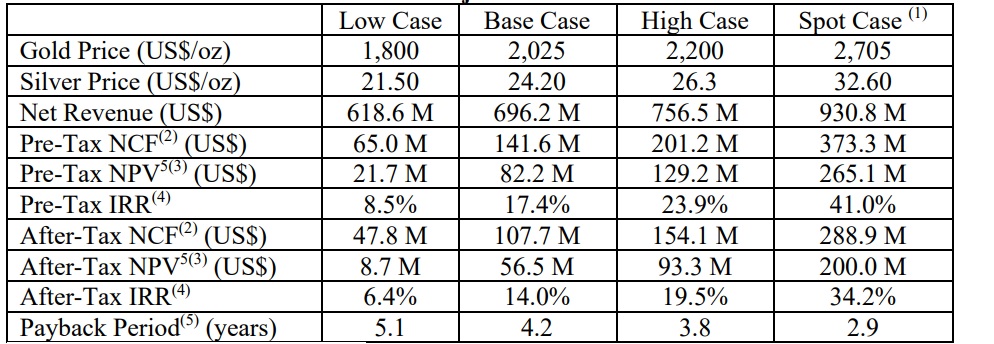

While the headline of the company’s press release reads ‘positive PEA’ and the company is ‘pleased to announce’, there is no way of sugarcoating what essentially is a very poor Preliminary Economic Assessment published by Lahontan Gold (LG.V) on its Santa Fe project. Using the word ‘positive’ likely refers to the ‘absolute’ result which was (slightly) higher than zero but under no circumstances could an economic study with an after-tax NPV5% of just US$56.5M and an IRR of 14% at $2025 gold be seen as ‘positive’. At $2025 gold, the payback period is estimated at 4.2 years which of course kills a project that has a mine life of just 6.5 years in the current mine plan.

As the sensitivity table above shows, even at $2200 gold the IRR is less than 20% on an after-tax basis and although you could argue the current gold price of around $2600/oz provides additional upside, one should compare oranges to oranges and most gold companies publish studies using $2000 or $2200 as a base case gold price. Even in the company’s spot case scenario, using $2705 gold and $32.6 silver (the silver production is pretty limited so using a higher silver price doesn’t have much of an impact), the after-tax NPV5% is just US$200M.

We had higher hopes and expectations for the Santa Fe PEA but with just under 340,000 ounces of gold being produced, the project makes very little sense to build right now. As per the current mine plan, only 345,000 gold-equivalent ounces will be produced, which is just a fraction of the 2 million gold-equivalent ounces across all resource categories (with 1.54 million gold-equivalent ounces in the indicated category and 411,000 ounces gold-equivalent in the inferred resource category).

Disclosure: The author has a long position in Lahontan Gold. Please read the disclaimer.