Shanta Gold (SHG.L) has just published an updated mine plan for its Singida gold mine in Tanzania. The average annual production at Singida is estimated to be approximately 26,000 ounces of gold, which would lift Shanta’s consolidated production profile to 100,000 ounces.

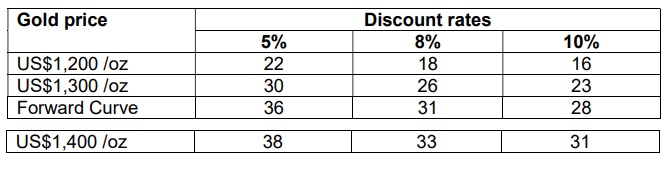

Notwithstanding the low capex of just US$16M, the after-tax NPV8% is estimated at just $31M despite using a very optimistic gold price in the base case scenario, so the NPV is materially lower when using a lower gold price. Using a gold price of $1200/oz and a 10% discount rate (to reflect the risk of doing business in Tanzania), the after-tax NPV10% decreases to $16M while the Internal Rate of Return drops from 67% to 47%.

So while the results at Singida look good at first sight, keep in mind the calculations are based on an optimistic forward curve where the gold price gradually increases from $1296 to $1472 towards the end of the mine life. It would indeed be great to see a higher gold price, but it’s a bit premature for companies to start using gold prices that are 15-20% higher than the spot price as a base case scenario.

Shanta could try to extend the mine life at Singida by bringing (a part of) the 344,000 ounce gold resource into the mine plan, but as the average grade of the inferred resource is approximately 25% lower than the 2.3 g/t used in the current mine plan, it remains to be seen of those ounces could be profitable at the current gold price.

Go to Shanta’s website

The author has no position in Shanta Gold. Please read the disclaimer