Thomson Resources (ASX:TMZ) has completed a total of 1,800 meters of drilling at its Bygoo tin project (10 holes for 762 meters were completed at Bygoo North, while the Big Bygoo area, just two kilometers away, was the subject of an additional 15 holes for a total of 1036 meters) indicating the average depth was just 75 meters per hole.

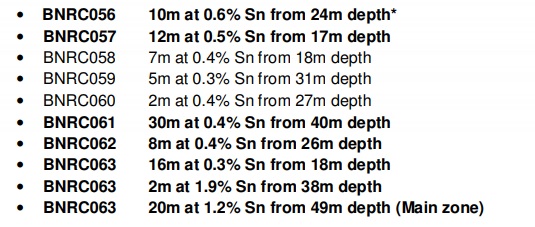

Thomson didn’t have to drill deep to discover what it was looking for: relatively thick intervals of economic-grade tin mineralization. At Bygoo North, all ten holes encountered shallow zones of tin with the worst intercept being 2 meters at 0.4% tin starting at a depth of 27 meters, but with excellent assay results of 20 meters at 1.2% tin and 30 meters at 0.4% tin. 0.4% doesn’t sound overwhelming but considering tin is currently trading around $20,000/t, it represents a gross rock value of $80/t which isn’t too bad for shallow mineralization.

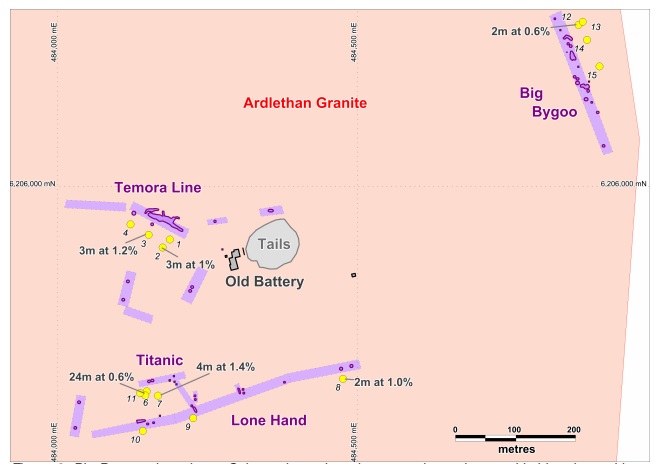

Considering the holes were drilled over a total strike length of what appears to be 200 meters, there appears to be quite a bit of tin at and around the old Dumbrells pit. If one would use a strike length of 200 meters and a width of 30 meters (note: the width of the mineralization is still unknown at this point, so this is merely meant to be a back-of-the-envelope calculation) and an average thickness of 10 meters would contain close to 200,000 tonnes of rock. That’s not too impressive just yet, but it will be interesting to see what else Thomson will pull out of the ground there. It’s also very interesting to see the thicker and higher-grade intervals around the old pit, so this will very likely be a zone of interest for Thomson, going forward.

The drill results at Big Bygoo were less impressive as the intervals appeared to be much shorter (2-4 meters with one longer interval of 24 meters) but at a higher average grade of around 1% Sn.

Tin is an interesting commodity and Thomson Resources may very well be sitting on something interesting, but the company will have to focus on proving up the potential size of the deposit as a few hundred thousand tonnes of mineralized rock won’t be sufficient to develop a mine. Thomson’s tin efforts are currently funded by a private Canadian company which could earn an initial 51% stake by completing A$3 in exploration expenditures before the end of April, where after it can acquire an additional 25% stake for A$22M. At this point in time, we doubt the partner will exercise the option to increase its stake to 76% as the implied project value of A$88M appears to be a bit too optimistic right now.

Go to Thomson’s website

The author has no position in Thomson Resources. Please read the disclaimer