Eagle Plains Resources (EPL.V) has been busy this summer as we count no less than ten press releases since July 1st with about half of those updates published in September. Plenty of reason for us to sit down with Tim Termuende, CEO of Eagle Plains Resources.

Termuende also is the CEO of Taiga Gold (TGC.C) which was actually spun out of Eagle Plains a little while ago as its gold discoveries and joint venture with SSR Mining in the shadow of the latter’s Seabee gold mine in Saskatchewan warranted the company to become a standalone entity.

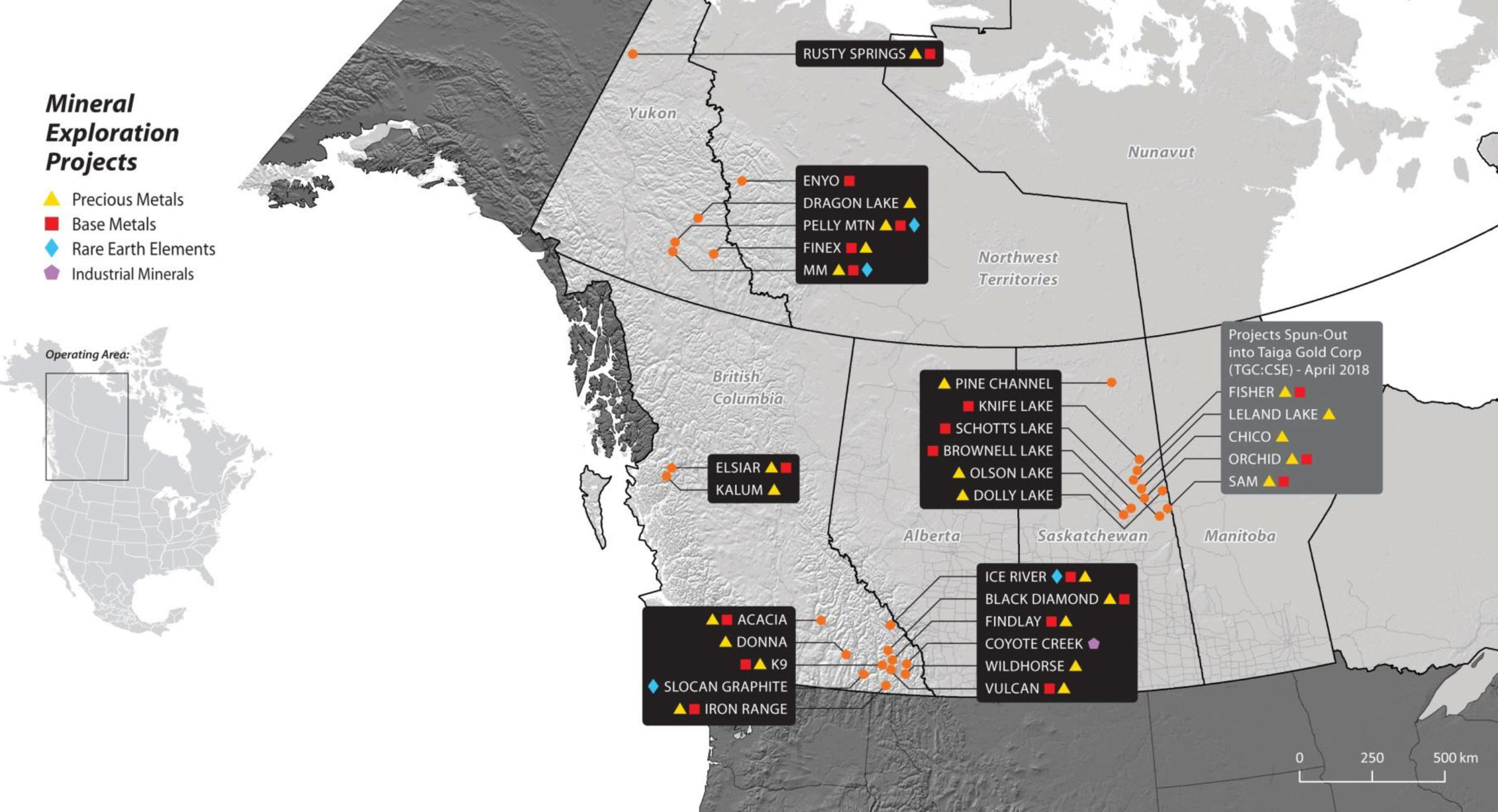

While Taiga needs to wait for SSR Mining to share its exploration results with them, Eagle Plains is in a different position. As a prospect generator with numerous assets and partners, there will be a continuous news flow while Eagle Plains has decided to drill-test some projects themselves.

We sat down with CEO Termuende to discuss the recent events, why he is so excited about the upcoming drill program on the BC-based Donna project, and how Eagle Plains’ history of spinning out assets in new companies has created shareholder value.

A sit-down with Tim Termuende, CEO of Eagle Plains Resources

Recent project announcements

Let’s talk about your recent acquisition first, the Nyberg Lake iron project. It’s interesting to see you getting involved in an iron ore project in a landlocked province. As iron ore projects typically require bulk tonnage hauling capacity, could you elaborate on the existing infrastructure (like railways)? Is the iron ore presence a plan-B in case your plan-A (exploring for iron formation hosted gold mineralization) doesn’t work out?

A fair question. Truth is, we are not interested in iron at all, especially in — as you noted — land locked, relatively low grade deposits. We are interested in gold though, and in this part of the world, gold is often associated with iron formation deposits such as this.

An excellent example is the Lupin Deposit, located in the Northwest Territory. The deposit was originally made in the 1960s and operated by Echo Bay Mines, a subsidiary of Kinross Gold Corp (KGC, K.TO) and in production from 1982 to 2006. Historic production at Lupin came from four zones — West, Central, East and McPherson — and a limited amount from the West Zone South of Shaft. The latter zone has an historic estimate of 1.1 million inferred tonnes at 11.32 grams gold for 403,000 oz.

To date over 3.4 million ounces of gold have been mined and recovered from Lupin with an average mill-head grade of 8.9 grams per tonne (0.259 ounces per ton) (WPC Resources news release Nov 1, 2016). Of course we can’t guarantee anything like those results, but they certainly give us a target to shoot for.

The initial resource estimate of 115 million tonnes at 35% Fe (from 1981, so this resource needs to be treated as a historical resource) is interesting albeit small. Could you perhaps provide some background on how you got the project and what kind of exploration potential you see for both gold and iron ore?

The acquisition of the Nyberg Lake project is another example of Eagle Plains doing what it does best-solid research and looking for value where others might have missed it. Looking through all the existing data, it appears that there was little or no sampling done for gold. Our plan is to send a team in this fall and take a lot of samples of every different rock type we can find. If we get a sniff, it’s “game on”- if not, then we see if there is a chance at development as an iron resource.

If neither of these approaches work, then we move on-you have to be prepared to kiss a lot of frogs in this business.

Our acquisition costs were low and once the fieldwork is completed, our investment overall will be minimal, but if successful, then this could easily be a company-builder. Without saying too much, we were already approached by a major player in the gold business about it soon after releasing the news.

You seem to have developed close ties with SKRR Exploration, which already optioned projects from Taiga Gold and now has also signed a deal to purchase the Manson Bay South project from Eagle Plains. Given your (well, Taiga’s) and their focus on the Trans Hudson corridor, is this a case of ‘great minds think alike’?

Absolutely. SKRR stands for “Saskatchewan”, “Ross” and “Ron”, namely Ross McElroy and Ron Netolitzky, both legendary Saskatchewan explorers who know what they’re looking for.

Ross and his team are credited with discovering the PLS uranium deposit in Saskatchewan in 2013 (for which he was awarded the Bill Dennis Award for Prospecting and Exploration) and Ron is an inductee into the Canadian Mining Hall of Fame. Both of these gentlemen have worked in Saskatchewan for decades and were very much aware (as was Eagle Plains and Taiga) of the exploration potential and the paucity of exploration activity there.

We were actively acquiring solid projects in Saskatchewan for over the past 10-15 years and they were watching (Ron was actually a director of Eagle Plains for years). Finally, President Sherman Dahl is a seasoned investor and financier who is well versed in finance and marketing strategies for small cap private and public Canadian companies. When SKRR was formed early this year, it was a natural fit to merge their experience and financial capabilities with our exploration and acquisition abilities. Having EPL’s 100%-owned TerraLogic available to carry out the fieldwork to advance these projects also serves as an important piece of the puzzle.Collectively, the group is quick to point out that despite Saskatchewan being rated as one of the best places for investment in the world, and with geology and mineral potential rivalling world class belts such as the Red Lake district in Ontario and the Abitibi Belt in Quebec, the annual exploration expenditures in Saskatchewan are a fraction of those in the other districts. This group is determined to change that.

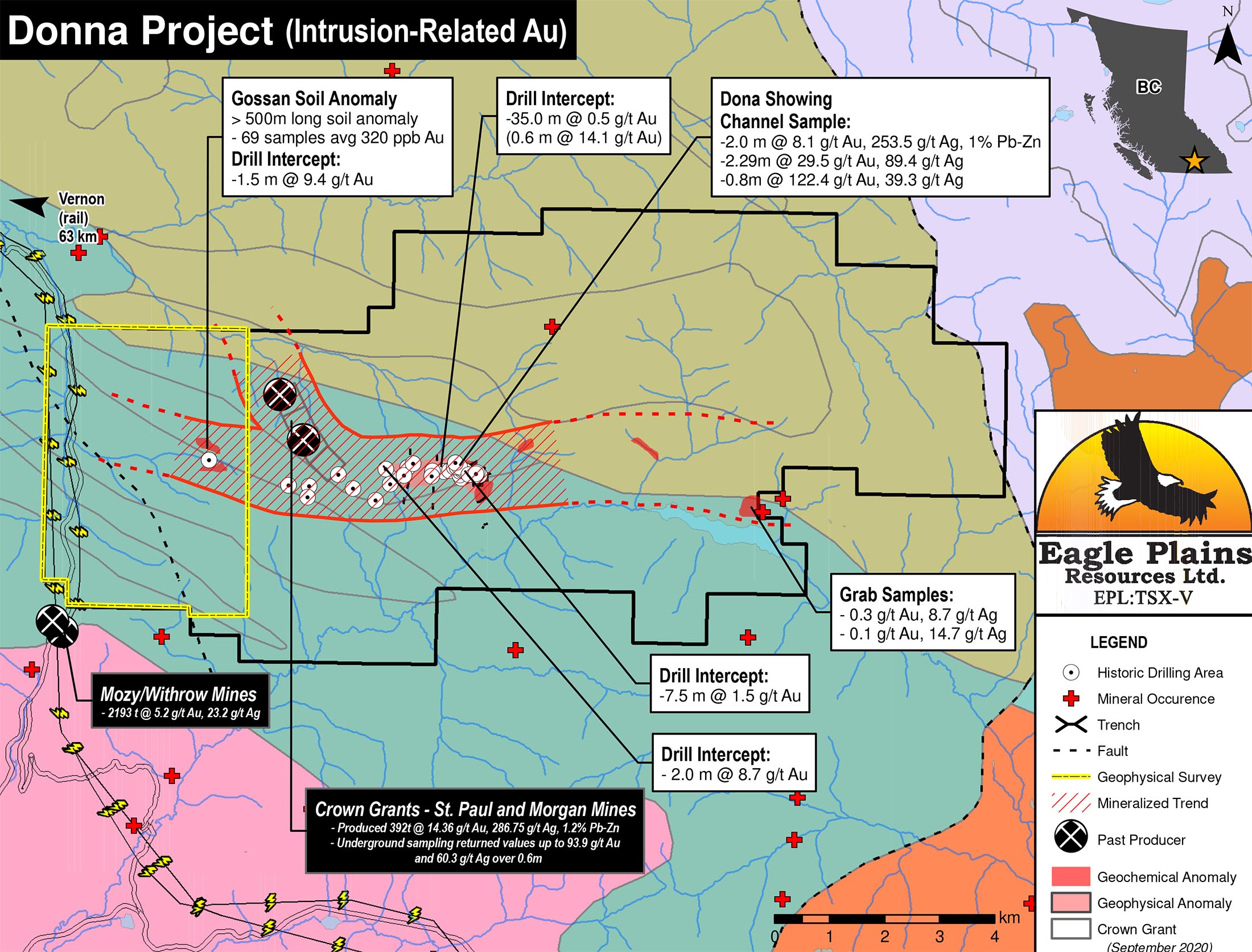

Let’s move over to your drill-ready Donna project in BC. How did you originally bump into the project, and what was the purpose of this summer’s airborne survey?

The Donna project came our way back in 2015 and was actually a swap with ALX Resources (formerly Alpha Minerals) for a uranium project we staked in Saskatchewan. ALX had a focus on uranium projects, while we were more bullish on the future of gold, especially in our back yard of southern British Columbia. We did some work on the property in the first couple of years, and Mike McCuaig, a really bright young geologist on our team noticed a lot of similarities to the geologic setting of some of BC’s world class porphyry deposits such as Highland Valley, Gibraltar, and others.

We also realized that the property is located in a sliver of the Quesnellia Terrane, which is the same geologic belt that hosts these behemoth deposits and many more. It’s elephant country for porphyry deposits. Oddly enough, the area is extremely under-explored, though access and infrastructure are excellent. The BC government has done extensive regional geoscience in all other areas of the province containing Quesnellia rocks, but oddly enough has completed only minimal work in this area.

Again, that is where we see the opportunity- looking for value where others might have missed it. We earlier optioned the property to Summa Silver, which was turning their focus to a silver project they had in Nevada, so we arranged to get back a 100% interest in the property, and now plan on hitting it hard.

In your press release from earlier this month, you mention you are aiming for a 3-4 hole drill program at Donna. Will this be sufficient to drill-test your theory? What would be an encouraging find in a small drill program like that?

One of the pieces to the puzzle at the Donna property was the historical workings that were located almost in the center of the claims. These were old crown grants, issued in the early 1900s and owned by the same small company for over 75 years. They were essentially the “hole in the donut” of our land package. The two mines, called “St. Paul” and “Morgan” were in production in 1915 and were closed when one of the owners died. The mines were reopened again and closed in 1961.

These mines consisted of a network of tunnels and shafts with an aerial tramway and a stamp mill. There was limited production (reported at 392 tonnes containing 5,630 grams of gold, 112,406 grams of silver, 3,720 kilograms of lead and 1,258 kilograms of zinc). Various geological reports and government publications report underground sampling returning values ranging from trace quantities to highs of up to 93.9 g/t (2.74 oz/t) gold and 60.3 g/t (1.76 oz/t) silver over a 0.6m sample width.

Oddly enough, there has never been a single drill hole reported in the area of the mines. This is not really unique to these old operations, as drilling long ago was very slow and not overly cost-effective. The old-timers often just tunneled their way in when they found something that might pay the bills. This approach often meant that they “lost the ore” due to small fault offsets, etc.We had been trying to get these claims for the past couple of years and not really getting anywhere, but earlier this year, one of the principals of the company “St Paul Mines Ltd” called us up and said that they would part with the claims on very reasonable terms. This is the first time in over 100 years that the area can be explored as a single project.

Our upcoming drill program is designed to achieve 2 objectives:

1. To test the area around the Morgan Mine shafts and tunnels.2. To test a very prominent gold in soil anomaly that our crews located during the last couple of years.

While this is not expected to be a large or costly program, we feel that a couple of holes in the area of the old workings will generate a lot of information for us, which we expect to help guide further work. Also, if our theory of gold mineralization proximal to an inferred buried intrusive holds together, then we will have a pretty good argument that we may be on top of a buried porphyry deposit, again, a potential company-builder.

Corporate Strategy

You’re based in Cranbrook, BC, and have recently announced several updates on projects in Saskatchewan and Manitoba. Is it fair to assume you are relatively ‘province-agnostic’ but will retain a focus on the western half of Canada? Would you ever venture out to other provinces or perhaps the States, or do you feel it’s important to maintain your focus on your core region?

We are big believers in exploring in our backyard. After-all, we are located in one of the richest mineral belts in the world in both BC and Saskatchewan. In addition, we have a huge competitive advantage in that gold (and all other metals) are bought in US dollars, but we pay all of our cost in Canadian dollars.

. Also, we are essentially a publicly-traded prospecting company-we are prospectors. To be effective as prospectors, we have to know the lay of the land: the geology, the geography, the politics and the people. Networks and relationships are critical to success. In my opinion, this is only earned over a long time and by keeping a focus. We have no intention of straying far from western Canada-there is no need to; there is a lot to chew on here!In addition, we are based in the East Kootenay’s-one of the most beautiful and remarkable places in the world. Being nestled in the Canadian Rockies, we are able to maintain a very low overhead, but still attract the type of people necessary to do what we do. We typically employ young, energetic, smart, outdoor-loving people that flock to this area and its lifestyle and who are very happy to have the opportunity to have a steady income and still call the area home. It may seem like a small thing, but it has been one of our secrets to success over the past years and decades.

Are all your projects available for joint venture and earn-in agreements, or are there some that you would like to keep for yourself and drill out for Eagle Plains’ account?

Generally as a Prospect Generator, we like to find partners for our projects. This serves five important purposes:

1. Cash and shares generated from our option deals pays the bills, and keep us from having to go to the market constantly to keep moving ahead. As far as I know, we are one of the few companies in our space that have been publicly trading for over 25 years and have not done a rollback. Today, we still have less than 95M shares outstanding, yet have a healthy treasury and no one has had to lick their wounds from a roll-back. We are very proud of this fact.

2. By bringing partners to our projects, we share the marketing burden with our partners. This is important, as we are unable to realistically talk about 30-40 projects at a time, but having our projects spread out through the various companies, they help keep the spotlight on each project themselves. This is especially apparent with SKRR and Rockridge Resources. These groups are especially effective at marketing and as significant shareholders, we get to go along for the ride.

3. By bringing in funding from other sources, we can carry out a “shotgun approach” to exploration and hit a number of projects hard, without suffering dilution. This is a trade-off of course, but we proved with Copper Canyon in 2011 that we didn’t need to have 100% of a project to reward our shareholders. We originally acquired the Copper Canyon property for less than $10,000, but after optioning the property and eventually owning a 40% interest (at zero cost to us for exploration), we were able to monetise that 40% interest for $65M-a pretty good risk-free investment by any measure.

4. Risk mitigation: as I mentioned before, you have to be prepared for the occasional disappointment as an explorer-this is the nature of an extremely high-risk business. By bringing in partners, we shed the risk but maintain access to the reward-simple as that. In 2010 we had over $10M spent on our projects by third parties, in turn, Eagle Plains only spent about $500K of our own money. As the cycle turned downward, we ended up getting most of those project back, all in much better shape than before we had brought in partners.

5. Finally, our team is comprised of young, keen, very competent geologists and technicians. Anyone familiar with the business will tell you that the more projects a geologist experiences, the better geologist he or she becomes. By using other company’s funds to explore our various projects, we are slowly but surely building up our own internal brain-trust.

Having said all of the above, we still like to take a shot ourselves every now and then. There are always projects in our portfolio that have a certain appeal, often based on geology or commodity, but occasionally the risk/reward ratio is just too attractive, based on location, infrastructure, etc. The upcoming Donna project is a good example-it gives us the opportunity for a home run hit in an underexplored area that has excellent infrastructure and offers a relatively inexpensive test of a compelling gold target in a gold bull market. I think that many of our investors want to see that from us from time to time.

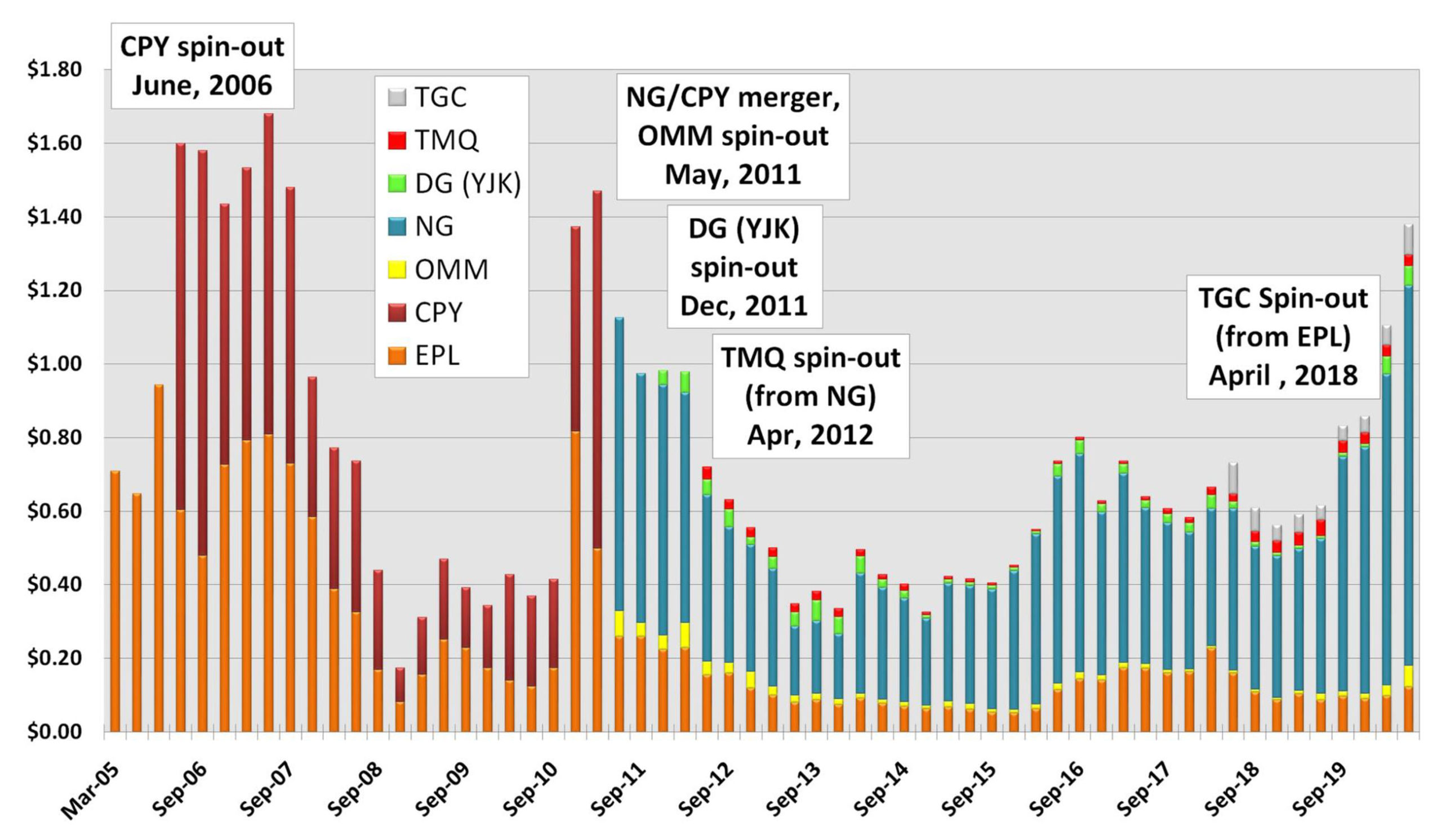

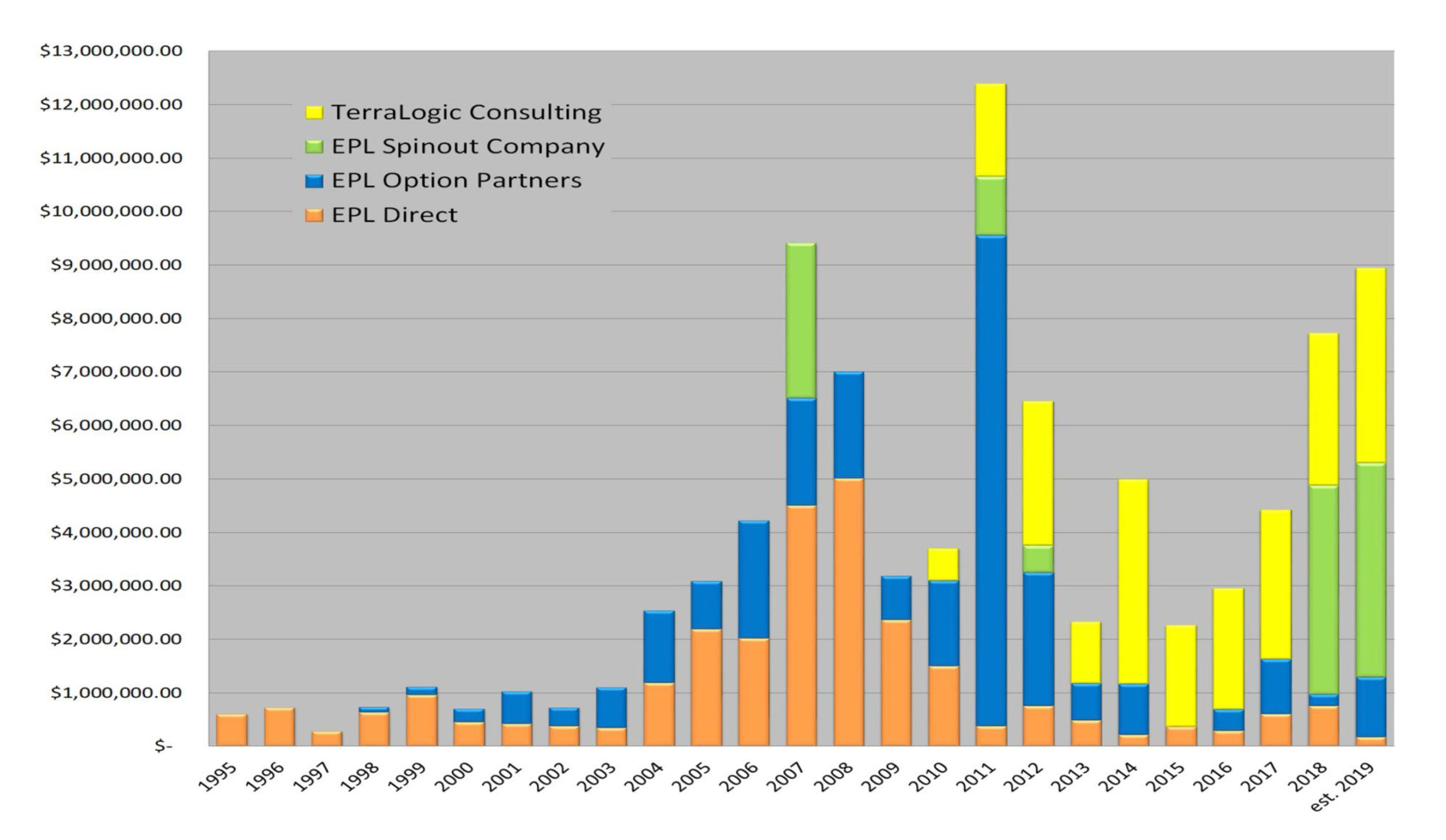

Could you elaborate on how Terralogic Exploration (yellow in the chart above) is an important part of Eagle Plains and how this revenue-generating subsidiary has been able to help pay your bills?

TerraLogic was set up in 2003 as Bootleg Exploration in order to separate our public company activities from our fieldwork. TerraLogic is owned 100% by Eagle Plains, but operates independently. It was a good call and we have never looked back. By keeping TL active and healthy, it ensures that we have a core team of experienced geologists available to us through thick and thin, and also have a steady stream of income that makes its way to our treasury.

Originally TL was mandated with doing work exclusively for Eagle Plains on Eagle Plains’ projects (with or without option partners). When the mining cycle experienced a decade-long slump that started in 2011, TerraLogic’s ability to seek work from unrelated third-parties helped Eagle Plains not only survive the downturn, but seize dozens of opportunities that only come to well-funded companies with the financial, technical and human resources to act on them.

As we continue along in this bull market, we expect TerraLogic to do much more work for Eagle Plains and its partners, which will serve to not only advance our projects with a crack exploration team, but also to continue to keep our geologic information and revenues generated from this work under our own umbrella. Again, living where we do in the East Kootenay’s, we find it relatively easy to attract talent and to retain it. A number of our key personnel have been with the company for over 20 years and don’t appear to be in any hurry to leave. That sort of loyalty, experience and devotion is hard to find in most companies.

We all know you from Taiga Gold (TGC.C) which attracted SSR Mining (SSRM, SSRM.TO) as an important JV partner on the Fisher Gold project where several gold discoveries have been made in the vicinity of the Seabee mine. Taiga was spun out off Eagle Plains, and in our previous discussions you indicated ‘the time was right’ for Taiga to become a separate company. Taiga wasn’t your first spinoff as you have completed several spinoffs before. Let’s take a minute to talk about what’s required for a project (or a group of projects) before you could decide it has the potential to continue as a standalone company? What’s your methodology and thought process here?

Being a prospect generator, we often have many projects being advanced simultaneously. This is a fantastic situation to be in, but a major downside is that we generate a lot of information that the marketplace has a hard time absorbing. One analyst noted that 90% of a prospect generator’s value comes from one project, while the rest get lost in the background noise. This is certainly true.

It’s hard to manage (and project) excitement about 10 projects at once, believe me. For this reason, when we find a project that seems to “rise above” the rest, we have been successful in separating this project from the herd and putting the spotlight solely on this project, while rewarding our shareholders with spin-out shares directly in this new company. This effectively acts as a ”dividend” to our shareholders.

It’s a different approach, and not many companies do it, but we’ve found it to be very effective.

I like to joke that it’s like taking a perfectly healthy person and putting them through chemotherapy-we strip Eagle Plains of an awesome project and give it directly to our shareholders. Naturally, Eagle Plains takes a hit and has to rebuild (which we are more than capable of doing), but our shareholders benefit immensely. In fact, if you take the cumulative value of our spin-outs over the years, these shares collectively are worth rough $1.40 per original Eagle Plains share, though we are currently trading at around $.15. This is not lost on our long-term shareholders and is part of the reason why we have such a loyal shareholder base. Eagle Plains is like a mutual fund for mineral exploration, without the inherent risk

Another function served by separating a project into a new company is that it makes it relatively easy for a partner company to acquire the entire asset, usually through M and A activity. We like to say that our spin-out companies are “built to be bought”. This was certainly the case with Copper Canyon, out first spin out. Copper Canyon was bought out by NovaGold (NG, NG.TO) in 2011 as a hostile takeover that eventually turned friendly in a $65M deal. We were told by our lawyers and advisors at the time that this transaction may have made Canadian M and A history, as we were trading at $.40 when we were approached as a hostile target and eventually settled at over $1.20 per share. This was an exceptional experience for management, one that we would love to try and repeat 😉

Finally, creating a spin-out company and getting shares in these companies directly to our shareholders provides liquidity for them while allowing them to keep their Eagle Plains shares. This is especially true in the event of a takeover event.

As for what our next spin-out will be, nobody really knows. Whatever it is though, I’m sure it will be found at the end of a drill string. Stay tuned.

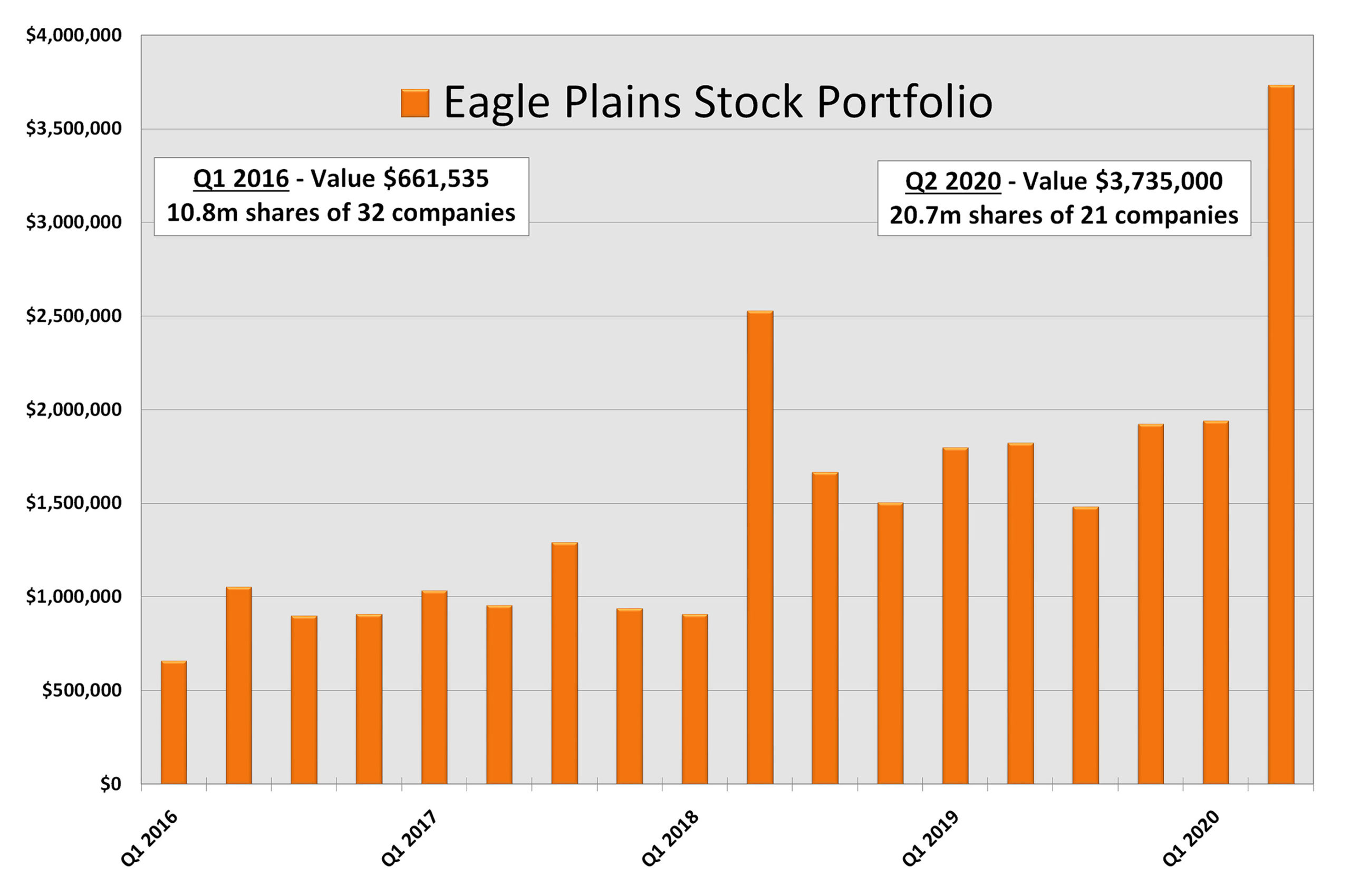

Your treasury remains exceptionally healthy with C$3.9M in cash but also almost C$3.6M in investments which mainly consists of shares you received from optionees. What’s your thought process on monetizing (some of) those shares further down the road? Additionally, your presentation mentions investments in 21 companies. Could you highlight in which non-related companies Eagle Plains has a position?

Part of our business model as a prospect generator involves receiving cash and shares from other companies. Obviously the cash goes to work maintaining the company, but the shares are also an important component. Our largest shareholding is in Taiga Gold itself, where we held back 19.9% of the company when we completed the spin out. Eagle Plains now hold over 12M shares of Taiga for a value of over $2M.

We learned over the years that it is important to keep an interest in our spin-out companies. Not only do that the shares have a very real chance of appreciating over time, but they also help us maintain voting control in the event of a hostile takeover. This was one of the critical lessons learned along the way.

We are not afraid to sell shares we hold, but we also are very mindful of our partners and are careful not to negatively impact their market. If we do decide to liquidate shares, we usually will contact management first and advise them of our plan, and work with them to minimize any negative impacts. This is part of our relationship-building efforts, and goes a long way to maintaining strong ties.

Another key aspect of our business that doesn’t get a lot of attention are our extensive royalty holdings. Years ago we decided to keep a residual interest in most of the projects that we sell or farm out in the form of Net Smelter Returns (“NSRS”). These are effectively an overriding 1-2% royalty on the finished product from production , meaning that no matter how marginal or successful a producing asset is, we get to take the cream off the top. Royalty companies have been very successful lately, and many show very strong financials on their royalty interests alone. We have done many deals with big names in the uranium business such as Cameco, Denison, Orano and others, and also have gold royalties with companies such as SSR Mining, Alexco, SKRR and others.

These royalties don’t not cost us anything to maintain, so are basically “sleeper” assets that may one day have considerable value. I don’t believe we are getting any value for them currently, though I expect that to change over time.

Conclusion

It looks like Eagle Plains is active on several fronts and over the next few months we can very likely expect a consistent flow of news and updates as both the portfolio of projects that have been partnered out and the 100% owned Donna project will see exploration dollars being spent.

Looking at the company’s financial statements, the TerraLogic revenue of C$1.4M in the first six months of the year helped Eagle Plains to keep the cash outflow to an absolute minimum. With a market capitalization of just over C$15M and an enterprise value of less than C$10M, any future discoveries, be it on a fully owned project or a project that has been joint ventured out, have the potential to increase the value of the company.

Disclosure: The author has a long position in Eagle Plains Resources. Eagle Plains Resources is currently not a sponsor of the website but could become one. Taiga Gold is a sponsor of the website.