It’s been a while since we caught up with Group Eleven Mining’s (ZNG.V) CEO Bart Jaworski. As the zinc price is moving up and as the company recently announced additional high-grade discoveries on its land package, we thought this was an opportune time to catch up on all things zinc, Ireland and exploration.

Q&A with CEO Bart Jaworski

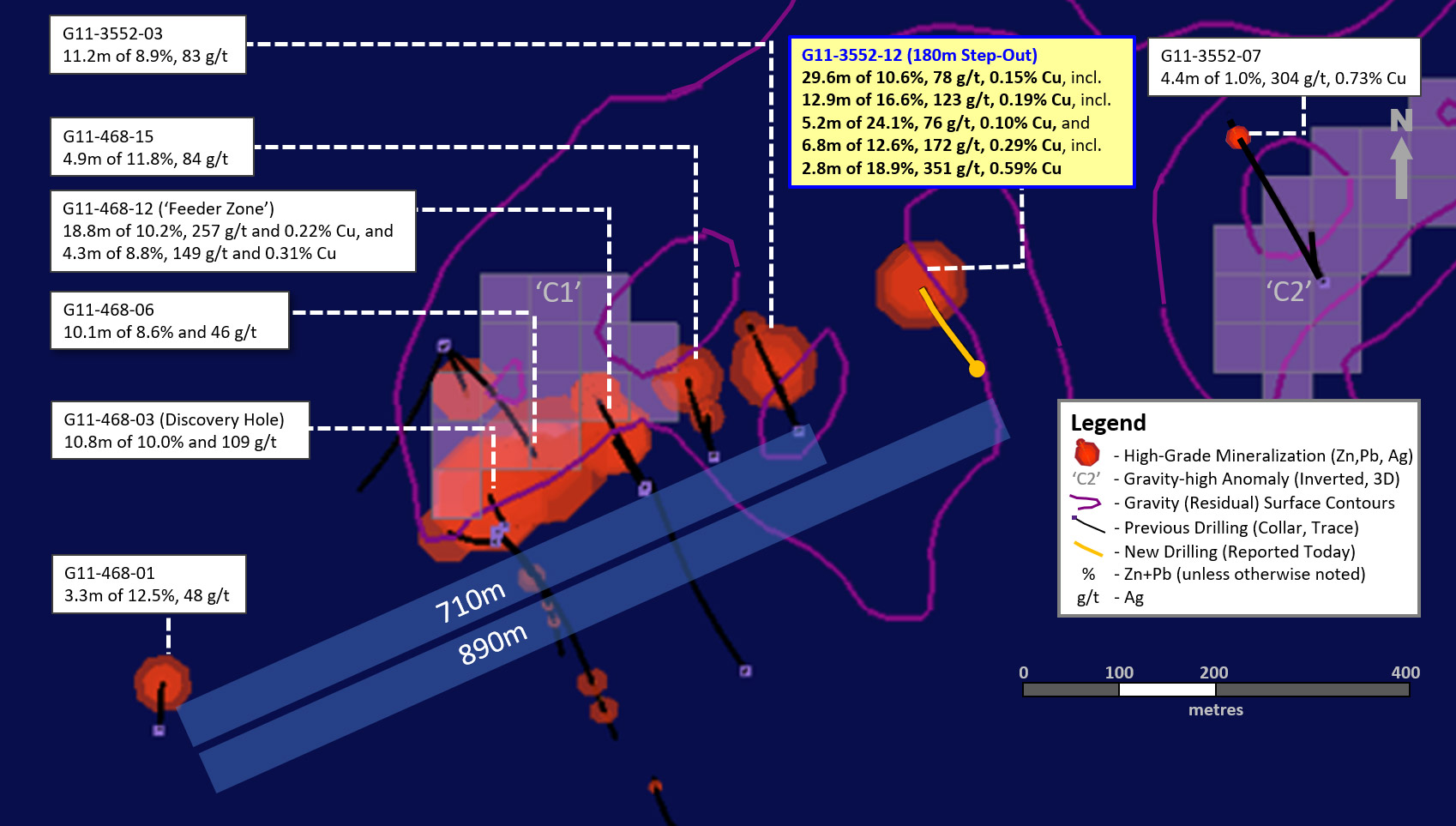

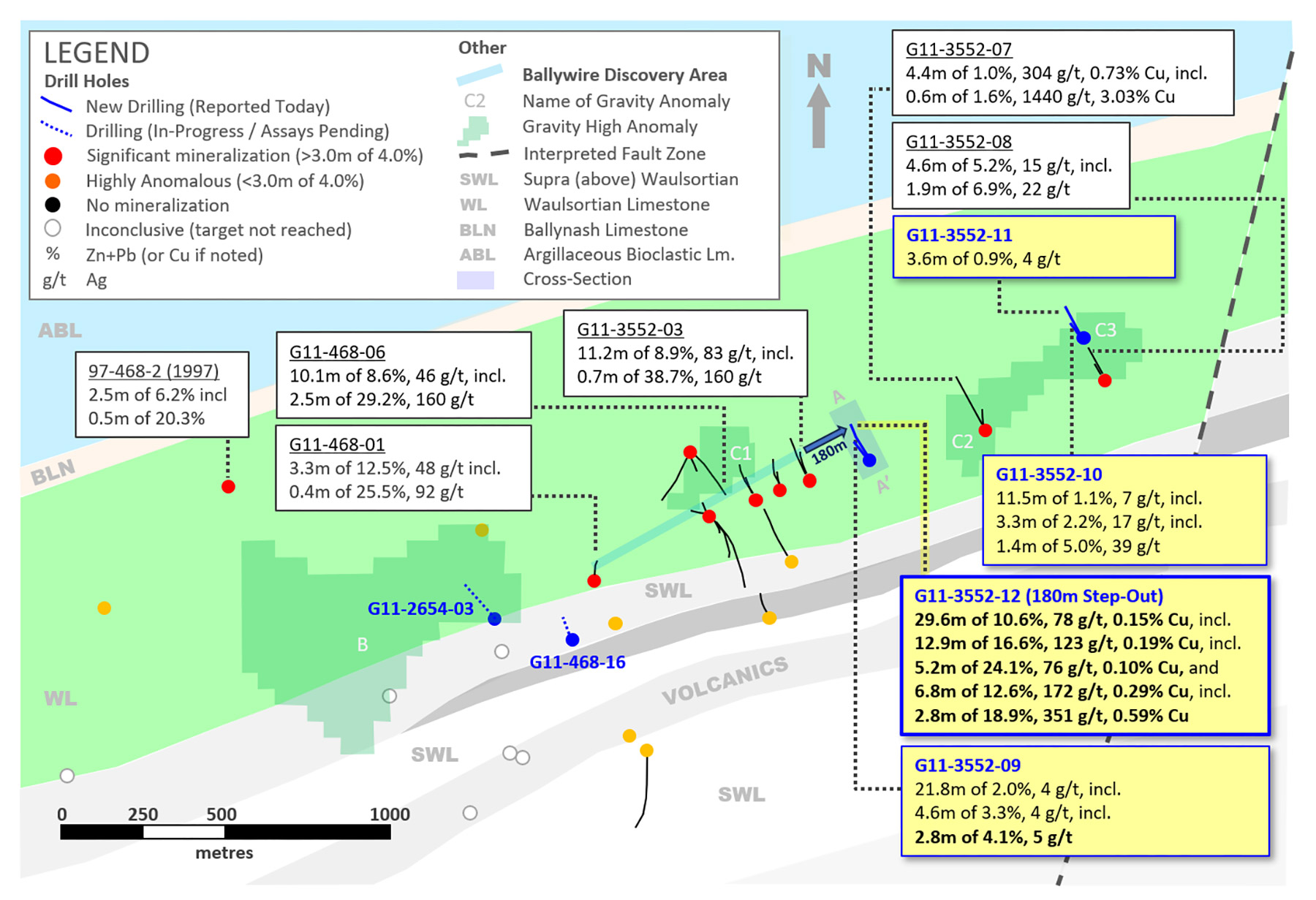

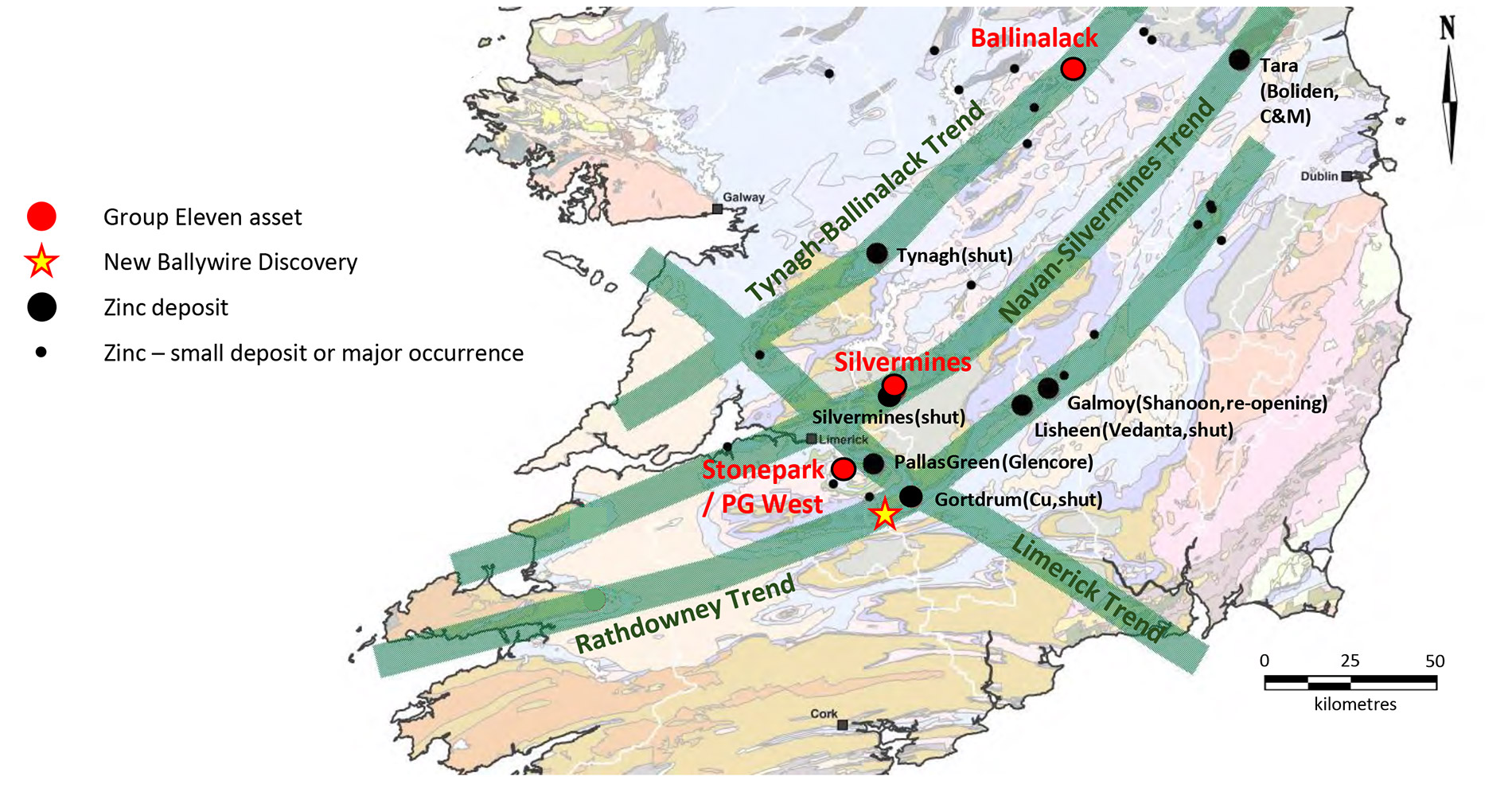

In June, you released your best assay results yet on your 100%-owned Ballywire discovery, which is part of the PG West project in Ireland. Your headline result of almost 30 meters containing 10.6% ZnPb and in excess of 2.5 ounces of silver per tonne of rock is indeed astonishing. Could you elaborate on how the location of that drill hole was determined, and how the previously drilled holes played a role?

We are lucky that a strong linear trend has emerged from the massive sulphide intercepts to date at Ballywire. In other words, all our hits to date line up. The big-hit announced in June was a 180m step-out to the east along this trend, underpinned by our knowledge of the geology (i.e. continuation of the target horizon, Waulsortian Limestone) and the continued presence of a gravity high anomaly (stemming from our recent detailed gravity survey).

In your press release, you mentioned the strike length has now been extended to 890 meters although you have traced mineralization over a distance of 2.6 kilometers. Can you elaborate on what the remaining 1.7 kilometers of mineralized strike length exists and how it ties in with the high grade discovery?

The 890m-long trend at Ballywire is the best drilled part of the entire Ballywire prospect. Specifically, it is where we’ve stepped out 60-80m from the discovery hole and consistently hit high-grade massive sulphides over good widths. The larger 2.6km includes the 890m zone, but also a well mineralized hole drilled in 1997 located to the west, as well as, our recent 530m and 930m mineralized step-outs to the east.

Circling back to your 890 meter strike length, how should we interpret the other two dimensions of the mineralized block?

The 890m zone trends roughly east-west. On the west side, the drilled downdip extent of mineralization (i.e. in a roughly north-south direction) is over 900m (including lower grade and narrower zones). The down-dip extent of the next drill fence to the east (hosting our discovery hole) is about 510m. The fences further to the east have consisted of more focussed drilling – so those down-dip extents are less well known at this stage, however, so far show that high-grade mineralization is at least 50-100m along dip. We are hoping that the 30m thick zone you mentioned above will be part of an even more laterally extensive zone of mineralization. We are currently drilling to test this theory.

You have now disclosed the assay results of 29 holes, and the drill program is ongoing. What do you think would be the critical mass (tonnage-wise) and what kind of drill density would you need to get there?

Rule of thumb in Ireland is at least 10 million tonnes of 10% Zn+Pb to start contemplating economics and engineering. Its too early to say how much drilling will be needed at Ballywire to get to that stage because we still don’t know the outline of the mineralized zone or where the hot spots are. However, I think it is fair to say that in Ireland, it is typical to need 100m or less in drill spacings for inferred resources.

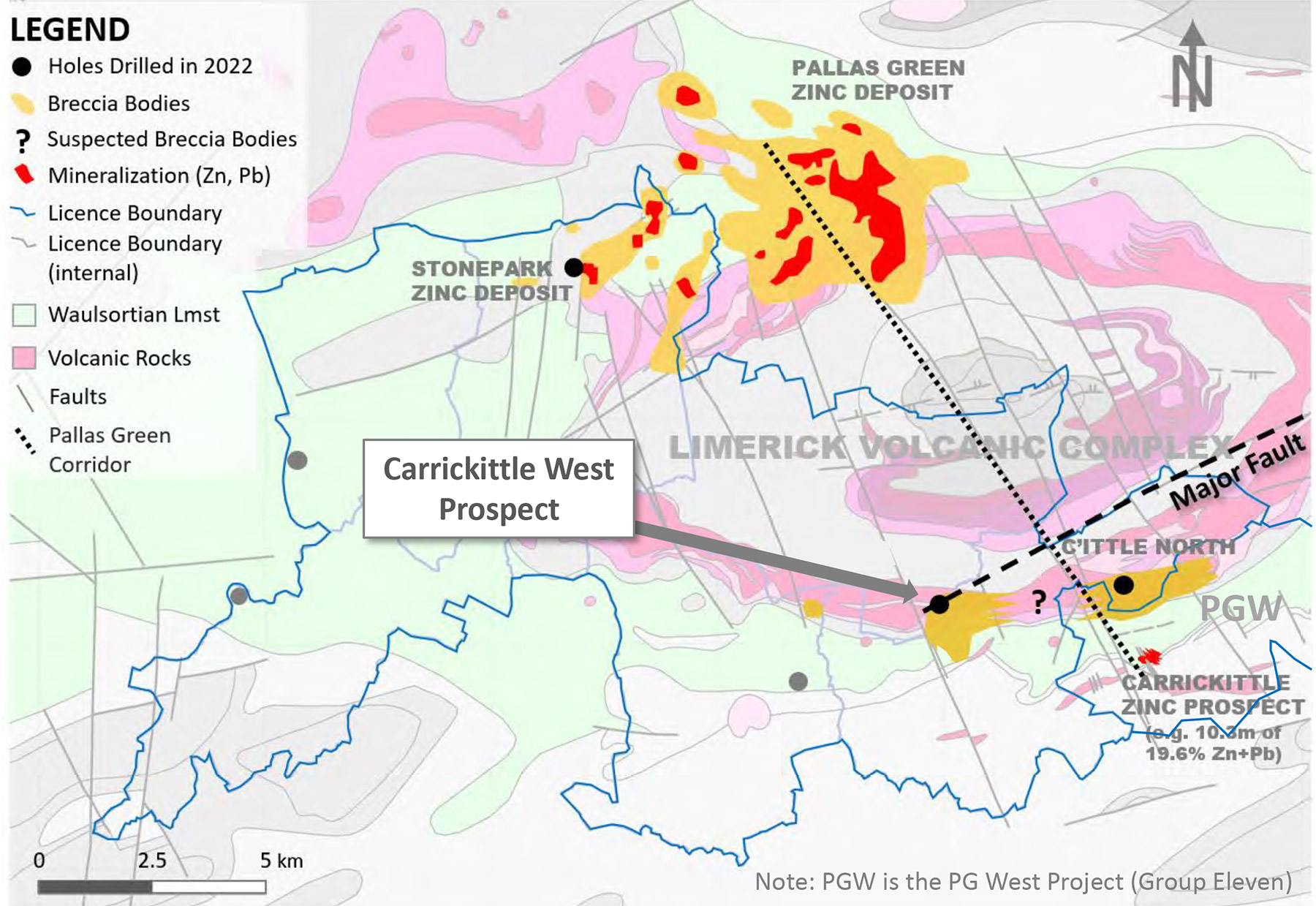

In your update released two weeks ago, you outlined your plans to drill 1,700 meters at Carrickittle West, in just 4-5 holes. What specific zone are you targeting there?

Carrickittle West is a mirror-image, lookalike target to Glencore’s (GLEN.L) Pallas Green deposit (45 million tonnes of 8.4% Zn+Pb, Inferred; one of the largest undeveloped zinc deposits in the world). Whereas Pallas Green is situated on the north side a large (20km wide) oval volcanic complex, Carrickittle West is on the south. Both the north and south share strong geological similarities, including volcanic centres (ancient volcanoes) which may have provided the plumbing and fluid flow required to form zinc mineralization during the mineralizing event. The south is even more interesting in some ways, given we proved (via drilling in 2022) the presence of a large fault with at least 150m of displacement. This may be a major feeder. We’ll be drilling 1,700m in 2H 2024, specially testing the volcanic centres and this major fault structure.

Forgive our ignorance, but given the exploration success at Ballywire, what is the main reason to drill Carrickittle West?

You are correct, Ballywire is our focus, however, Carrickittle West is also an amazing target – and we want to keep progressing it and keep it in good standing.

Doing Business in Ireland

As Ireland had to deal with some mine closures in the past few years, has the stance towards mining changed at all, or are the locals (and lawmakers) keen on getting new projects on line?

Yes indeed, the Galmoy and Lisheen mines were exhausted in 2012 and 2015, respectively, and the last remaining zinc mine in Ireland, Boliden’s Tara operation, is now ramping up after a flooding event and high-energy costs forced it to temporarily close in mid-2023. News of Tara’s temporary closing certainly made the headlines here in Ireland and the topic was hotly debated on the heels of the news by the then Prime Minister (Taoiseach) and the leader of the opposition, in parliament (Dáil Éireann). It made the headlines because it affected thousands of direct and indirect jobs at the mine site, the local town of Navan and nationally. This, I believe, made the public more aware of the importance of keeping this industry alive in Ireland – after approximately 60 years of continuous zinc mining in Ireland. Separately, ISIF (Irish Strategic Investment Fund) publicly stated they have contracted South Africa’s Lionshead Capital Partners (a mining specialist fund) to help deploy €30 million in funding for Irish mining projects. This is a welcome move – and certainly in step with the European Union which recently enacted the CRMA (Critical Raw Materials Act), trying to fast-track critical metals projects in Europe to decrease reliance on China.

What is the current drill cost in Ireland?

Relatively inexpensive compared on global peers – we’re approximately C$150 per metre, all in (including assays). This reflects the fact we don’t need helicopters, road building or any cribbing on the side of a mountain – like you do in some jurisdictions.

Although your asset is located in Ireland, the Canadian government is increasing the pressure on Canada-domiciled companies and making it harder to have foreign investment on the corporate level if the focus is on one of the 31 critical minerals. Zinc is on that list so in theory Group Eleven would be under additional scrutiny on the level of the federal government if anyone (Glencore?) would ever want to take a run at you. Have you discussed the potential re-domiciliation of the company to a jurisdiction with less government meddling with your board of directors? You are living in Ireland anyway, so it would be relatively easy to cut the ties with Canada?

I suspect we are currently below the market value thresholds which would put us at odds with these types of restrictions. For now, its not an issue that we have focussed on significantly within the Company. We are content being domiciled in Canada. However, if in future major restrictions were imposed on our M&A flexibility, then we would more strongly consider our options at that point.

Corporate

Although the zinc price has been moving up in stealth mode and it is currently trading at $1.35 per pound, it looks like the market remains pretty indifferent to the base metal. How is the perception of zinc on the more ‘corporate’ level? You are operating in ‘zinc-land’, so you must hear a different opinion on zinc and the anticipated supply/demand dynamics from the larger players in the sector?

The outlook for zinc has drastically improved over the last six months or so on the back of supply constraints. A lot of zinc mines globally have recently been shuttered, either temporarily or permanently reflecting high energy, input and labour costs as well as, in some cases, diminishing grades. Meanwhile, demand side is holding steady and expected to grow by about 2% per annum over the next decade, according to South32’s (S32.AX, S32.L) news release from February 15th, 2024. Global mined zinc grades are about half of what they use to be some 20 years ago and that, plus increasingly stringent environmental regulations in China and other parts of the world are making it difficult to flex upwards on supply. The most tangible metric to look at when gauging zinc prices over the next year are the TCs – or treatment charges. The lower the TC, the more bullish the outlook for zinc prices because it means the smelters are dropping the fees they are charging the miners in order to attract increasingly scarce supply of zinc concentrate (the product which comes out of mines). In 2023, TCs were about $270 per tonne of concentrate, whereas this year the benchmark set (between Korea Zinc and Teck) was $164/t. We are hearing spot TCs in Asia, however, are near zero and/or negative – which is a very bullish situation.

At the end of March, you had about C$2.1M in working capital. How far will that get you?

This working capital should be more than sufficient to carry us through all the planned exploration for the rest of the year, including Ballywire and Carrickittle West.

There are 12.5M warrants with a C$0.12 strike price expiring in 3 months from now. May we assume you see warrants being exercised on a daily basis?

A small number of those warrants have been exercised thus far and we do expect the rest of those to come in over the next 3 months or so as long as the share price stays above 12 cents. If exercised fully, that would bring in about C$1.5m, helping accelerate our exploration.

What percentage does Glencore currently own? Do you talk to them on a regular basis? What would they like to see you do?

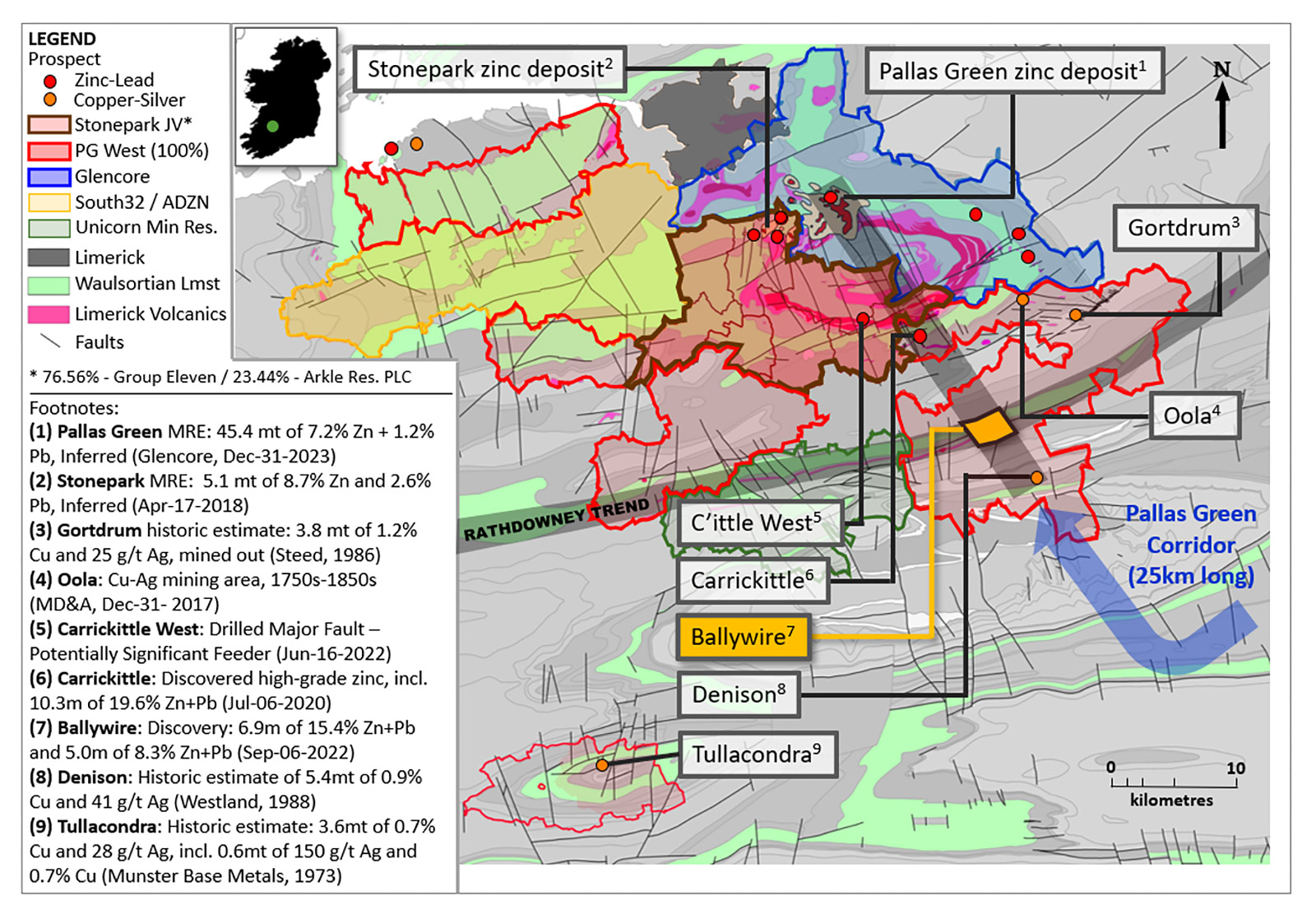

Glencore owns 18% of Group Eleven and yes indeed, we keep in regular contact with them. I believe Glencore wants us to succeed on the exploration front because that would enhance their Pallas Green project. In other words, our interests on the ground are very much aligned.

Conclusion

Group Eleven’s share price has tripled in the past year, and deservedly so. The company is fortunate to attract the markets attention thanks to the combination of new high-grade discovery holes and the strengthening zinc market.

The company is a direct neighbor of Glencore which owns the 45 million tonnes Pallas Green project and South32 and we are pretty certain the discoveries made by Group Eleven are closely followed by the larger players in the area. The endowment of mineralization in the Pallas Green area appears to be larger than originally thought, and Group Eleven is doing its part in working towards defining tonnage on its side of the district.

Drilling should start soon at Carrickittle West, and hopefully this means Group Eleven will have an action-packed and news-filled second half of the year.

Disclosure: The author has a small long position in Group Eleven Resources. Please read the disclaimer.