In July, we flew to Kamloops, British Columbia to visit GSP Resource Corp (GSPR.V) which has an option to acquire 100% of the Alwin copper mine project. A maiden resource calculation on the property is currently in the works and should be published in September, but we already wanted to get a better understanding of the property and the strategic land position.

Strategic, indeed, as the Alwin mine property is directly adjacent to Teck Mining’s (TECK.TO, TECK) Highland Valley copper mine, which is Canada’s largest copper producer. And as Teck’s open pit mine continues to expand, including towards the west where GSP’s Alwin project is located, it is now becoming a question as to when the Alwin property will become a ‘nuisance’ for Teck Resources as the mining giant will either have to take the third party ownership of Alwin into consideration when it updates its operational plan for the 2030s, or it will have to find a way to purchase the Alwin asset.

And that’s our main consideration for being a shareholder of GSP Resource Corp. With just under 29.5 million shares outstanding, the current C$0.075 share price indicates the C$2.2M market capitalization represents tiny valuation and the market isn’t giving GSP enough credit for its Alwin mine project.

The history of Alwin

Before discussing our findings from the site visit, it’s perhaps a good idea to briefly discuss the history of the Alwin copper mine, and why GSP Resource Corp was interested in picking up this asset in 2020.

Copper mineralization was detected at Alwin in the late 19th century where after small-scale and basic mining activities commenced at the beginning of the 20th century. The project was a bit dormant after the initial copper production but saw two specific eras of renewed (exploration and mining) interest with known activities between 1967 and 1982 and 2005 to 2008. It’s during those years that plenty of drilling occurred. Between 1967 and 1970, the previous owner-operated completed in excess of 12,000 meters of drilling, including 6940 meters of surface drilling in 81 holes and almost 5,900 meters of underground drilling in 119 holes. On top of that, about 1,400 meters of underground development workings were completed as well, marking a very busy few years in the project’s history.

Subsequent to those exploration activities, a 500-ton-per-day mill was built, and about 76,000 tonnes of rock were mined and processed. The average grade of the rock processed in the mill was just over 1.5%. After a brief hiatus, the capacity of the mill was increased by 40% in the eighties, and a new owner mined 155,000 tonnes of rock, at 1.54% copper. As you notice, the grade of the copper remained pretty consistently around the 1.5% throughout the brief periods of production.

The mining activities were supported by an additional 15,000 meters of drilling in the late Seventies and early Eighties. This ultimately also resulted in a historical resource calculation of just under 400,000 tonnes of rock with an average grade of 2.5% copper. It goes without saying that the calculation is 1) non-NI43-101 compliant and 2) will be irrelevant once GSP’s own resource calculation is published later this quarter.

GSP Resource Corp was able to acquire the property on the cheap in 2020. The copper price started to get weaker again as the world was preparing for a pandemic. In total, GSP will be required to pay C$250,000 in cash (C$125,000 has already been paid) and issue 4.5 million shares, including 2 million shares to be issued upon the delivery of a bankable feasibility study and the 8th anniversary of the approval date of the agreement in 2028. 1.6 million shares have already been issued.

And finally, the sellers were awarded a 1.8% Gross Smelter Royalty, of which GSP Resource Corp can repurchase 0.8% for C$1.5M in cash. This results in a 1% GSR on the asset, payable to the vendors.

The access to existing infrastructure is excellent

We flew into the regional airport of Kamloops where multiple flights per day connect the city with Calgary and Vancouver, both are major international airports. From Kamloops, it’s an easy 1.5-hour drive to the project site on paved roads and highways. On the drive from Kamloops, you bump into several open pit mines with New Gold’s (NGD, NGD.TO) New Afton mine just outside Kamloops. The main landmark of course is the Highland Valley Copper mine, owned and operated by copper giant Teck Resources (TECK, TECK.TO). The mine has been operational for decades, and the company has just filed an application to approve its plans to keep the mine open until at least 2040. Those plans are backed by the current measured and indicated resource which contain in excess of 1.1 billion tonnes of rock.

The nearby Highland Valley copper mine is slated to produce 112,000-125,000 tonnes of copper and 1,300-1,600 tonnes of molybdenum this year, increasing to 150,000 tonnes of copper and 2,000 tonnes of molybdenum in 2025. At 330 million pounds of copper and 4.5 million pounds of molybdenum in 2025, the mine will generate a total revenue of in excess of $1.5B and protect the hundreds of jobs (it budgets US$350M to be spent on labour this year so the impact on the local economy on a direct and indirect basis is pretty massive). Teck Resources has guided for a total capex spend of US$250-285M this year and continues to work towards extending the mine life to 2040.

Access to the Alwin project is relatively easy, as one has to turn on a well-maintained dirt road at the end of the tailings facility. Once you leave the Teck-operated tailings dam, the road gets a bit bumpier but we have seen worse potholes in Vancouver, Calgary and Europe, and the main areas are still easily accessible by car. The foundations of the old mill site are still present, while a power line is still accessing the property.

As the pictures show, we were taken on an extensive tour by CEO Simon Dyakowski to get a good understanding of the asset.

What is GSP trying to do at Alwin?

GSP is lucky it has recently gained access to historical data which is a game changer for the project. Previous operators did not have a modern compilation of the old drill holes, workings and geology maps. The assay results from the historical drill programs are a big help during its own drill program, and the company will be able to use the data for the first time in its upcoming resource calculation.

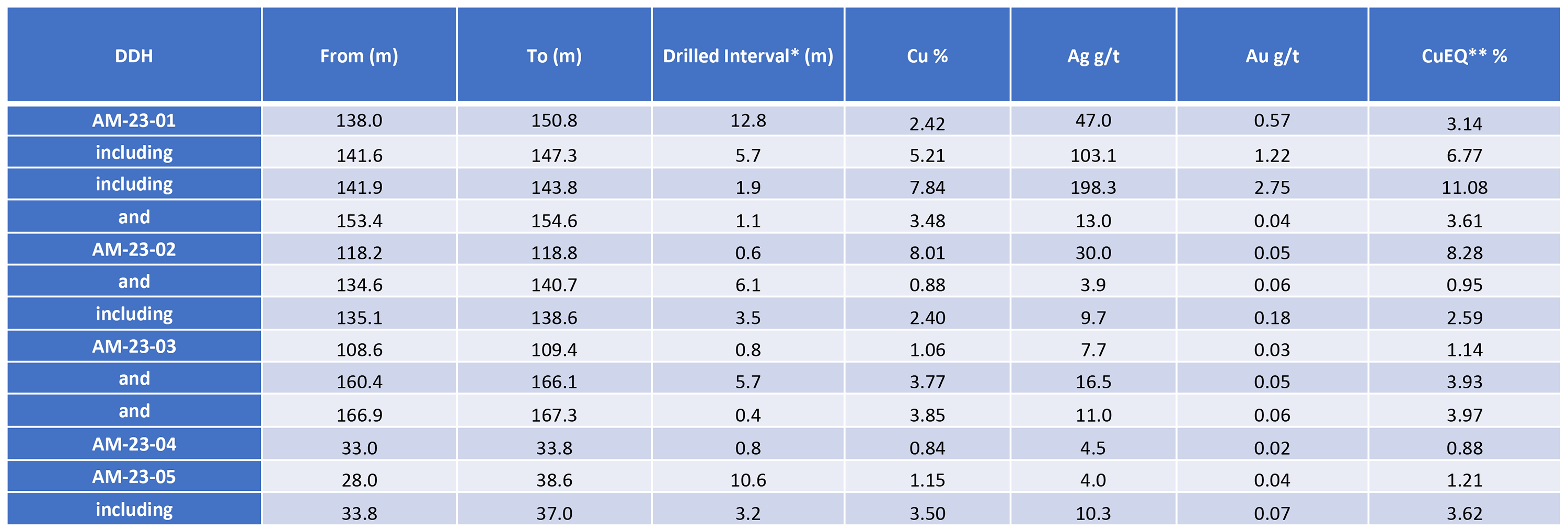

We think there are plenty of opportunities to build on the expertise of the previous owners and operators. The historical resource estimate we mentioned before was 1) using a higher cutoff grade than what would be applicable today and 2) only focused on the copper. GSP’s previous drill programs at Alwin have clearly shown the presence of gold and silver as well, and those precious metals were not really taken into consideration in the past. One of GSP’s most successful holes was AM23-01 which encountered 12.8 meters of 2.42% copper, 0.57 g/t gold and 47 g/t silver. This means the copper-equivalent grade of the precious metals was approximately 0.7% CuEq. At today’s metal prices and before taking recovery rates and payability into consideration, the higher gold and silver price would result in a 1% CuEq grade, higher than the 0.7% that was applicable upon the original calculation.

As a reminder, the measured and indicated resources at neighboring Highland Valley Copper contain 1.1 billion tonnes at an average grade of 0.28% copper and 0.01% molybdenum. Teck did not disclose any gold or silver values in its 2023 annual report.

As far as we are concerned, we see two possible ways for GSP Resource Corp to monetize the asset. Either the strategic land position of Alwin will become a nuisance to Teck Resources, or the copper resource could become an area of interest to Teck. GSP’s upcoming resource may have an open pit resource component to the model – which would be a first for the Alwin project as historically it was only known to be an underground type mine.

GSP also has several targets to expand on the mineralization around the Alwin Mine, particularly along strike to both the NW and directly east. GSP has true “porphyry” style exploration targets at the Al showing at the northeast of the Alwin claim block and in the recently acquired 100% owned Mer property.

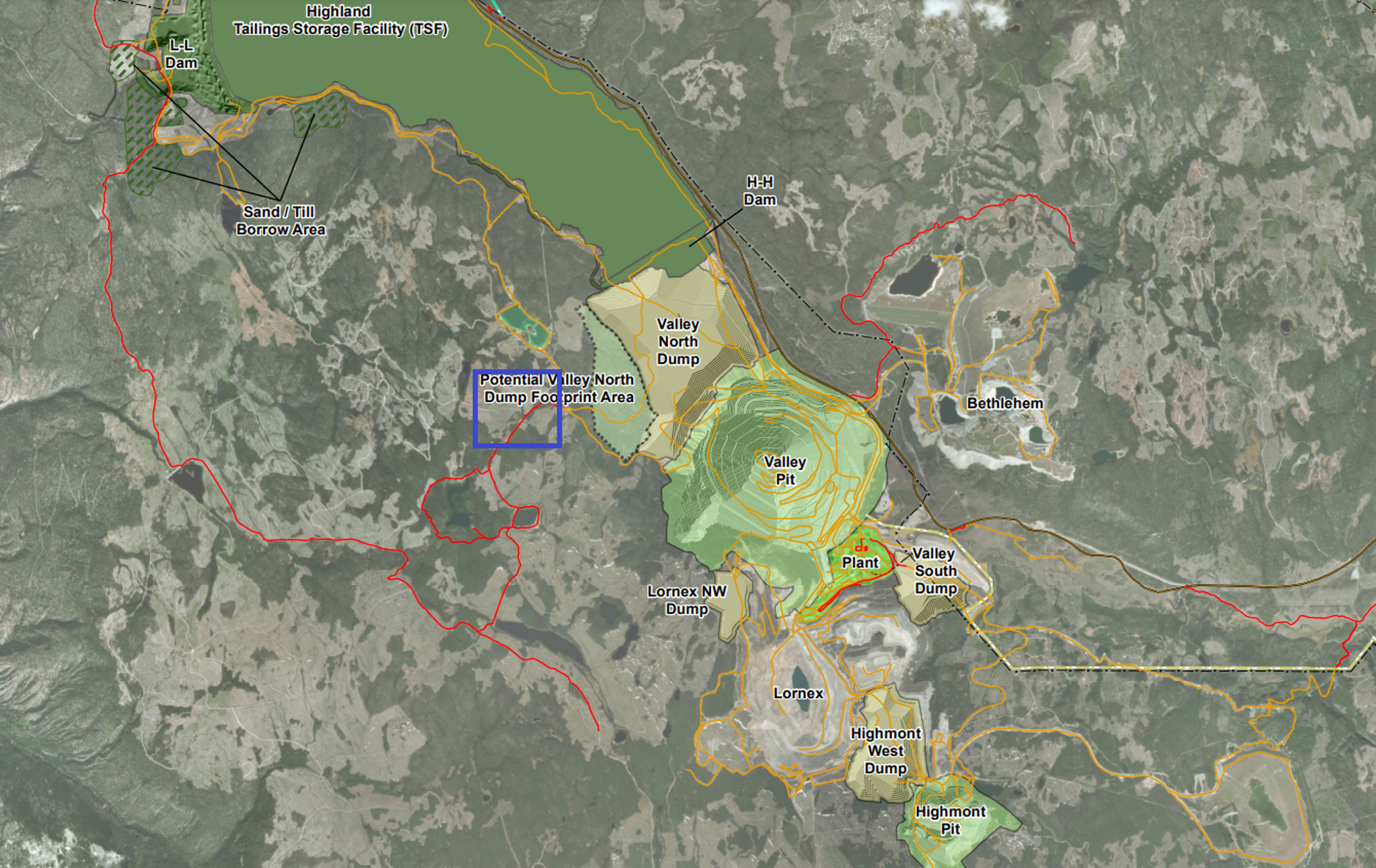

In our view, Teck likely won’t be bothered too much by a small resource, and it is more likely that the large copper company will want to have free reign at and around its existing open pit. As you can see below, as per the 2040 development plan, Teck Resources wants to extend the Valley North Dump towards Alwin (the approximate location of Alwin is highlighted in blue). This indeed means Teck plans to go all the way up to the property boundary in its 2040 mine plan. This also means that once it reaches the property boundary, the Valley North Dump cannot easily be expanded further west, unless Teck Resources acquires the land.

But Teck could also kill two birds with one stone. Let’s say there’s 1.5 million tonnes at 1% copper. Note, this is purely an arbitrary number and should not be interpreted as a resource guidance by us nor the company. We did find an old report on the government website outlining a historical resource of 1.05 million tonnes at an average grade of 2.5% copper, with the potential to add 250,000 tonnes.

Given the additional drill programs and using a lower cutoff grade, we don’t think 1.5 million tonnes is a stretch, but we would obviously refer to the official resource calculation later this quarter. It would be pretty easy to run those tonnes through the Highland Valley mill. The topography would also allow for relatively shipping costs as the plant is located a few kilometer from Alwin, and rock could easily be moved downhill. If rock with a grade of 1% could be blended in with 0.28% bearing rock at a 20:1 ratio, the average grade would increase by 10% to 0.31% of copper. At a more likely 40 or 60:1 ratio (which makes more sense given the nominal mill capacity of 133,000 tonnes per day at Highland Valley, it is unlikely a 20:1 ratio, which would imply mining in excess of 6,000 tpd at Alwin is feasible), the impact would still be noticeable although it would be less pronounced.

The scenario outlined above is a purely theoretic thinking exercise how the Alwin rock could potentially spike the average grade milled at Highland Valley. Just to be clear: there is currently no joint venture or plan in place that would see that scenario happen. But it would make sense for anyone to try to lever existing infrastructure.

While it would definitely be worthwhile for Teck Resources to explore this option, there obviously is no guarantee the large copper miner will care at all, with its 1.1 billion tonne resource in the measured and indicated resource categories it has bigger frish to fry. But the larger the Alwin resource (and the higher the grade), the more likely it is for Teck to take the Alwin project serious.

Conclusion

GSP Resource Corp. is an exploration company trading at a tiny valuation. It will be interesting to see what the independent consultants come up with in the maiden compliant resource calculation, which will be published in September. At the very least, the upcoming resource estimate will underpin the current valuation of the company, and have recommendations to expand from there with further drilling, but we are particularly interested in seeing the gold and silver values at Alwin, and what the recommendations of the consultants are to further improve the understanding and increase the value of Alwin.

At the current valuation of C$2.2M, GSP Resource Corp appears to be an interesting speculative bet on the company becoming too much of a nuisance to neighbour Teck Resources. There are no guarantees in life, and Teck may easily snub the Alwin mine project, but the company believes they can grow the upcoming resource with further drilling and even attract other partners than Teck. That is also why you are paying a shell-like valuation for GSP. It’s a low-cost lottery ticket.

Disclosure: The author has a small long position in GSP Resource Corp. GSP is not a sponsor of the website. GSP covered the vast majority of our travel expenses. Please read the disclaimer.