After reporting a very sudden CEO switch which saw Executive Chairman George Salamis re-taking the reins from former CEO Jason Kosec after only 18 months, Integra Resources (ITR.V, ITRG) has now released the production update on its fully owned Florida Canyon gold mine in Nevada while it also provided an update on its hedging program for this year.

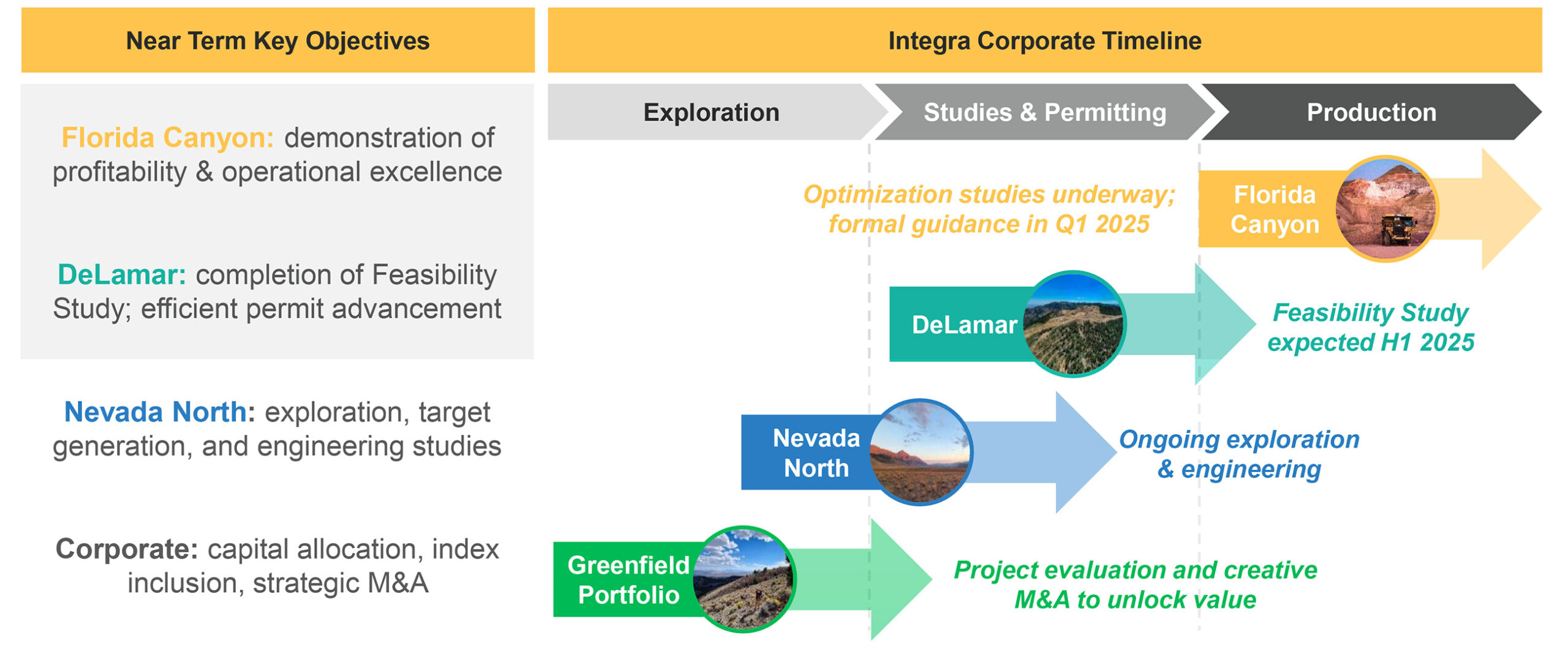

This is the first stepping stone towards a few additional milestones including the Q4 financial results (which still won’t contain a full quarter of revenue and cash flow contribution from Florida Canyon) and the guidance for this year. Meanwhile, the permitting process at DeLamar in Idaho remains on track, and likely accelerate given a more pro-mining political administration now in office, and all Idaho activities should be funded by the cash flow generated by Florida Canyon.

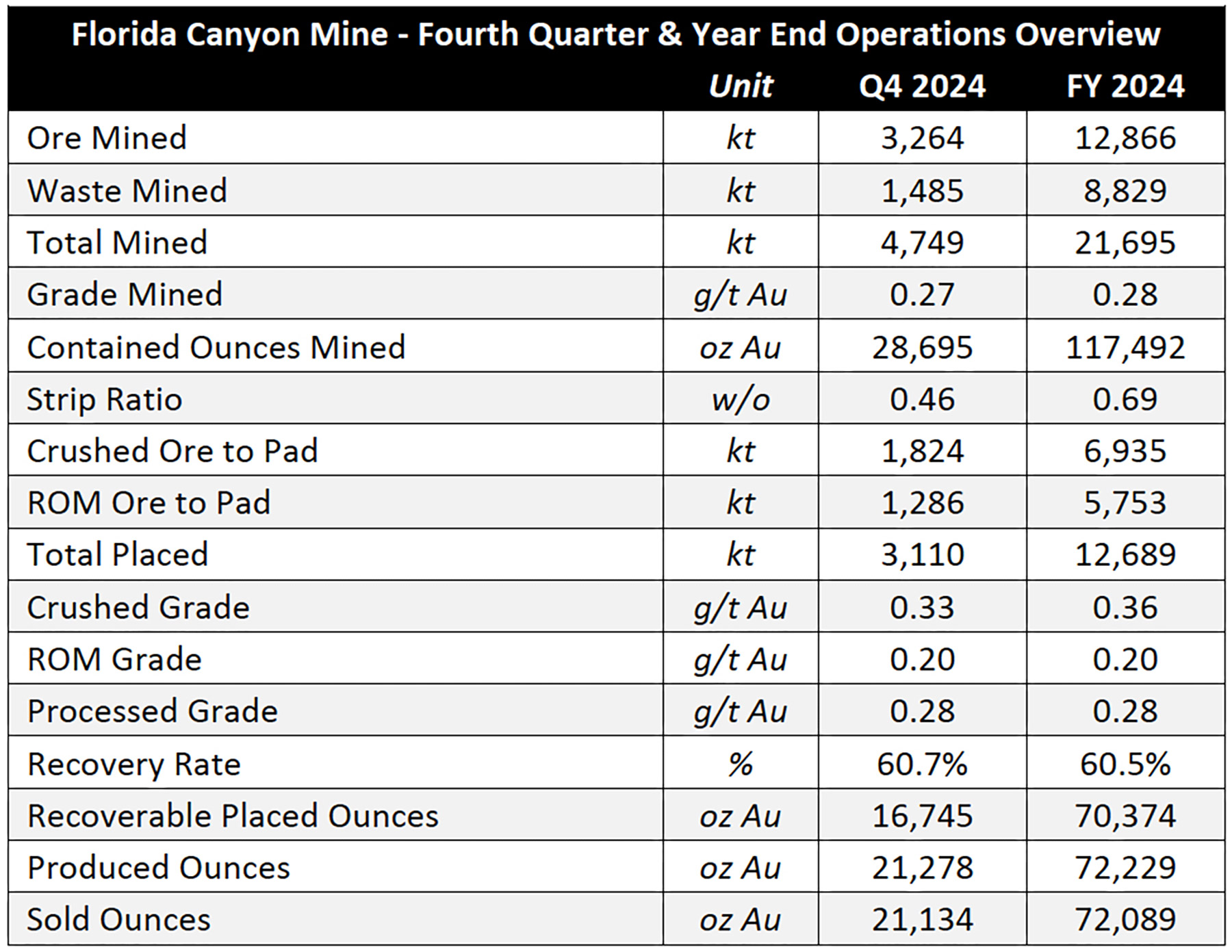

The FY 2024 production at Florida Canyon

Florida Canyon actually had a pretty good year from an operations perspective. The mine produced a total of 72,229 ounces of gold and as the table below shows, the fourth quarter was pretty strong with a total production of just under 21,300 ounces of gold.

Interestingly, the mine performed much better than what was outlined in the mine plan and what was guided for by Argonaut Gold. The contained gold ounces mined came in 17% above target while the recoverable placed gold ounces beat the top end of the guidance by approximately 14%.

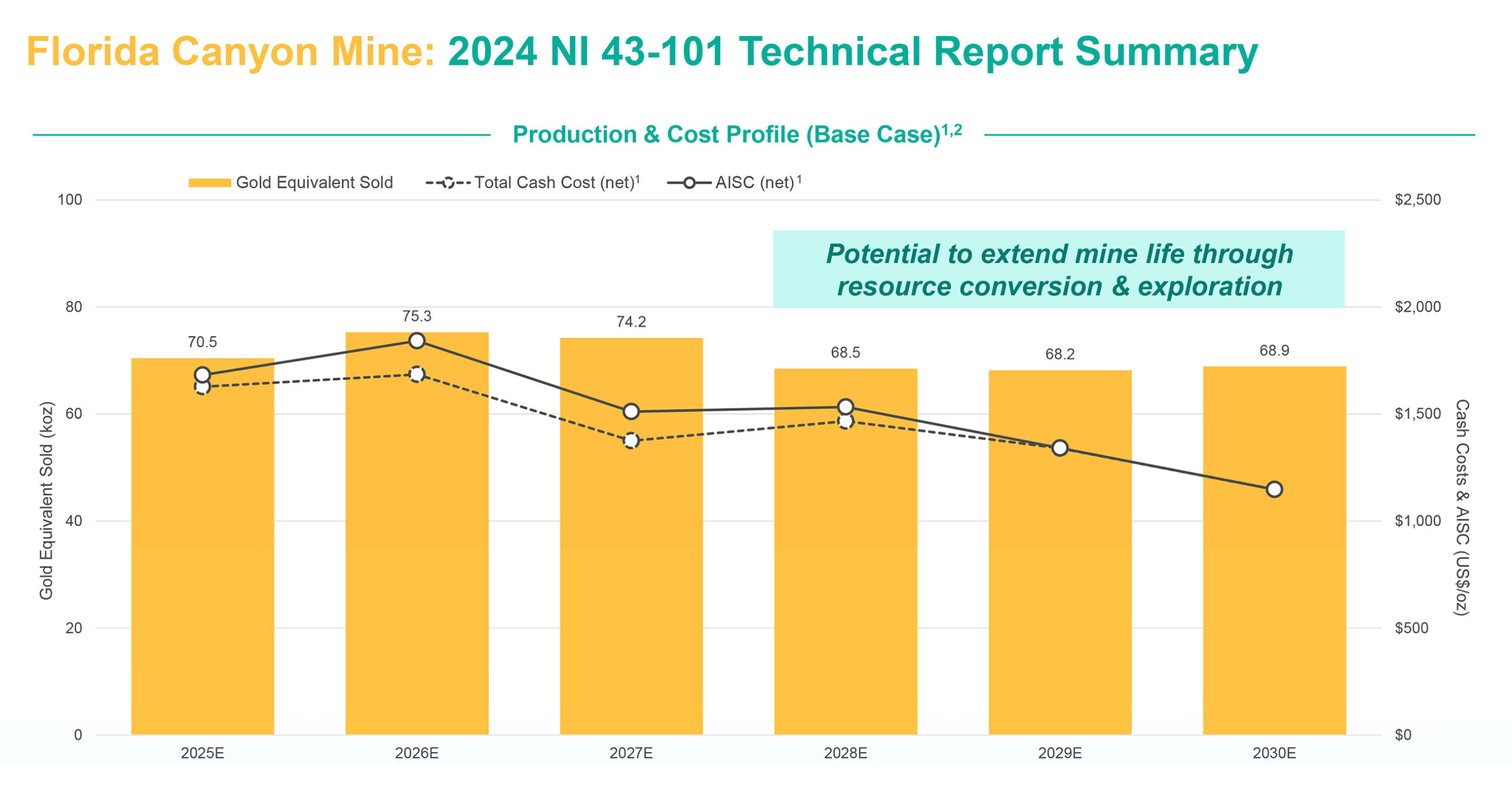

This bodes well for 2025, and Integra should release its guidance for this year in the coming month or so. As a reminder, the mine plan as per the official NI43-101 technical report anticipates a saleable production of 70,100 ounces of gold and just under 40,000 ounces of silver and we expect Integra’s 2025 guidance to be pretty close to these numbers.

Discussing the hedge program

Integra Resources also provided an update on its ‘gold price protection program’ as it has engaged in a strategy to actively hedge a portion of its gold production.

The company confirmed it has purchased put options that cover about 37,800 ounces of gold with an average strike price of $2,400 per ounce with expiration dates between January 2025 and December 2025. This represents approximately 54% of the anticipated production for this year and will be a big help to protect the potential downside, which we view as a prudent strategy in its first year of growth as a new gold producer in the industry. According to the mine plan (shown below), the 2025 production is anticipated to be around 70,000 ounces of gold. The anticipated AISC as per the technical report is approximately $1700/oz but Integra may have its own priorities and may bring forward some of the investments and this could weigh on the AISC number. It is not unlikely the AISC will be higher than this number as Integra works towards implementing some of its own ideas to improve Florida Canyon further down the road.By locking in a floor price of $2400/oz, Integra will make about $400/oz on those 37,800 hedged ounces (we are being conservative here and apply a $2000/oz AISC in the first full year of Integra operating and owning the mine, we will narrow this down once Integra releases its official guidance), resulting in about US$15M in cash flow (after capex but before taxes). The remainder of the anticipated production (about 32,000-34,000 ounces of gold) remains unhedged, however in discussion with the company, they might be considering more hedging at some stage. At the current spot price of $2750/oz, all gold will be sold at $2750 as the put options will expire out of the money, and Integra will generate about US$50M in cash flow.

Right now, Integra is buying put options. In an ideal world it would engage in costless collars but as there is some debt on the balance sheet, the debt covenants may have to be reworked before all parties can sign off on a more detailed hedging strategy whereby the company also sells call options.

So for now, Integra buys put options. That doesn’t have to be expensive considering the futures market for gold points towards a sharply higher gold price later this year. Have a look at the gold price for delivery in December of this year (screenshot taken on January 27, 2025 after closing):

Indeed, based on the futures market, gold traded at in excess of $2850/oz in December. That’s not just our guess, that is the actual gold price for delivery in December. The advantage of the contango situation (futures prices are higher than the spot price) is of course that buying put options is pretty cheap.

Right now (using the data of January 23 – keep in mind option premiums and futures prices obviously continuously change), the cost to purchase a put option at $2400 for June 2025 is just under US$6/oz. A put option at the same exercise price for delivery in January 2026 is just $18/oz. So in essence: the current contango situation on the futures market makes the put buying program very affordable.

Let’s be clear: the numbers we just quoted are up-to-date on January 23, 2025. Integra Resources has been buying put options since December and the gold price (and futures prices) were lower back then which also means the put premiums were higher. That being said, we feel pretty comfortable using an anticipated hedging cost of $30-40 per ounce. This means that at the higher end of that range, hedging 37,800 ounces of gold comes at a cost of 37,800 * $40 = US$1.5M.

That sounds like a waste of money, but it actually isn’t. By protecting the downside on these ounces, Integra is basically protecting a minimum margin of $400/oz (based on our assumed 2025 AISC of $2000/oz at Florida Canyon) for a total net cash flow of $15M. Paying $1.5M to guarantee an assumed $15M in net pre-tax cash flow (with future additions to the hedge book likely having a materially lower cost than the $40 we assumed)? That’s a trade-off we would like to see a company (any single producing asset company, really) take every day of the year, especially in its 1st year of production as a gold producer.

In an ideal world, Integra would also start selling call options to end up with a collar, if their debt covenants allow. And considering the gold market is in a contango situation, those call options can bring in quite a bit of cash in the kitty. Just to give you an example, a call option with an exercise price of $3000/oz for delivery in June 2025 yields a premium of $48/oz. Integra could thus sell call options and use the proceeds to purchase put options.

And if it follows a 1:1 ratio, it would actually make money on that collar. It could sell calls for 5,000 ounces at $47/oz while buying puts with a strike price of $2400/oz at $5.5/oz. The difference of $41.5/oz could be pocketed and could provide a boost to the effectively realized price: if the gold price in June trades at for instance $2750/oz, both the calls and puts would expire out of the money (i.e. at zero dollars) but Integra would of course still retain the delta of $41.5/oz in which case the realized gold price wouldn’t be $2750/oz but $2791.5/oz after taking hedges into consideration.

The example above is 100% arbitrary and just serves as an example to show how those collars work). Right now, Integra is limited to buying put options but we hope a more inclusive strategy of selling calls will be activated soon as well. And of course there are plenty of possibilities as well. Integra could for instance sell 1 call option for every three put options it purchases to keep a higher portion of the ounces exposed to higher gold prices.

Bottom line: buying put options is a relatively cheap but secure way to protect the cash flows. And given the contango situation on the gold market selling calls further down the road could improve the returns on the hedge book.

Conclusion

Hedging isn’t a bad word nor a bad strategy, especially at these gold prices. While it’s understandable market participants and gold bugs prefer to see the gold production remain unhedged, the simple truth is that Integra still needs to protect its downside, especially in 2025 and 2026 before the anticipated production costs at Florida Canyon will decrease as the strip ratio will come down. Hedging got a bad reputation because most gold companies started to hedge during downturns or almost at the bottom of a downturn and were proud to be ‘hedge free’ when gold prices were strong. And that’s the wrong way to approach hedges, as it actually makes sense to protect the margins when the gold price is high.

We do hope Integra Resources can move on to collars sooner rather than later because even though the option premiums to buy put options are relatively low, it’s always better to keep a million dollars in the treasury rather than spending it on hedges. But for now, buying put options is a pretty cheap ‘insurance premium’ to protect the downside and there shouldn’t be any debate at all whether or not this is useful for Integra.

We are hoping to see Integra’s full-year production guidance soon to see how it stacks up against the mine plan in the NI43-101 technical report on the Florida Canyon mine, though we understand that the company might have its own view on [cost] guidance as compared to the 43-101. The technical report anticipated a production of around 70,000 ounces of gold which is a very respectable production number which means that at the current gold price Florida Canyon should generate approximately US$50M in pre-tax cash flow, after taking the cost of hedging into account and after applying a higher AISC of $2000/oz (which we will of course fine tune once the company releases its cost guidance).

And that’s not too shabby for a company with a market capitalization of just over US$150M.

Disclosure: The author has a long position in Integra Resources. Integra Resources is a sponsor of the website. Please read the disclaimer.