When we learned about Integra Resources’ (ITR.V, ITRG) plan to acquire Florida Canyon Gold (FCGV.V), we were not exactly very enthused. It sounded a bit like ‘buying production for the sake of buying production’ and the eyed re-rating basically happened overnight when the company used stock at a 0.1x NAV multiple to acquire an asset at 0.5x NAV. The share count almost doubled overnight, resulting in a higher average NAV multiple.

Additionally, the Florida Canyon gold mine had a negative connotation, mainly due to Argonaut Gold siphoning the cash away from Nevada to fund the massive cost overruns at its Magino project in Canada. Alamos Gold (AGI, AGI.TO) put Argonaut Gold out of its misery and the assets it didn’t want have now been sold. The Mexican assets went to Heliostar Metals (HSTR.V) and Integra Resources is now absorbing Florida Canyon in its portfolio of Nevada & Idaho assets.

While we initially considered the acquisition to be a head-scratcher, subsequent discussions with Integra’s management team have subdued our initial negative approach. It still very much is a deal that needs an average realized gold price of $2250 gold for the next two years to make the acquisition worthwhile but every day the gold price continues to trade at $2400/oz is a day that further derisks the acquisition. Additionally, we are glad to see Integra’s management team plans to hedge a portion of the anticipated production, which should reduce any gold price-related concerns.

Additionally, the increased market cap could help Integra meet the requirements for inclusion in the GDXJ ETF, which generally focuses on companies with a market cap in excess of US$150M and favors producing mining companies with cash flow. At the current share price and assuming the acquisition and sub-receipt financing go ahead, Integra would get very close to meeting that threshold.

The proposed deal

Florida Canyon Gold started trading just over two weeks ago, and the sole reason for the company to be spun off from Argonaut Gold as part of the sale to Alamos Gold likely was that the latter was focused on acquiring Argonaut solely for Magino, for the efficiency benefits and economies of scale with its nearby Island gold mine. Alamos does not currently have any operations in the USA.

All non-core assets were folded into Florida Canyon Gold, and then Florida Canyon basically liquidated itself. The Mexican assets were sold to Heliostar Metals and now Integra Resources is acquiring the Nevada asset. Integra didn’t rush into this, as the first rumors of Integra being in the data room to kick Florida Canyon’s tires emerged in June, when we heard rumblings while we were in Nevada for a site visit hosted by another company. Two months ago, several companies were rumored to be in the data room and Integra emerged as the best bidder. We don’t know if Integra was the highest bidder, but let’s not forget Alamos Gold controls a large block of Florida Canyon stock, so it for sure had a preference and say whose shares it wanted to own. And for what it’s worth, we understand that Alamos is supportive of the transaction and is expected to enter into a voting support agreement in favour of the transaction.

Integra resources is offering an all-share deal whereby every share of Florida Canyon Gold will be swapped for 0.467 shares of Integra Resources.

Of course, it is always possible a third party emerges with a superior offer (Integra wasn’t the sole company in the data room), in which case a US$2.25M (roughly C$3M) break fee would be payable to Integra. But for now, we are assuming the merger goes ahead and hope to see an update on Integra gaining support from Florida Canyon’s largest shareholders.

The advantages and disadvantages

Every deal has advantages and disadvantages. And although Integra Resources is a sponsor of the website, we don’t want to sweep the elements that we perceive to be negative under the rug.

The positives

- First of all, the acquisition provides Integra Resources with incoming cash flow. While that incoming cash flow will be relatively low in the first few years of the remaining mine life, a lower strip ratio and a lower sustaining capex will accelerate the cash flows from 2026-2027 on.

- If the gold price holds up and at least remains steady, the incoming cash flow from Florida Canyon should be sufficient to cover all corporate expenses, including completing the permitting process on the DeLamar project in Idaho plus some exploration at Florida Canyon.

- CEO Jason Kosec mentioned he plans to hedge about half of the gold production for the next few years using costless collars with a bottom price of $2300/oz and a ceiling of $2600/oz. While this will take away some of the upside in case the gold price does break out, we consider hedging a portion of the anticipated gold production to be a positive as it reduces the downside risk of acquiring a high-cost asset.

- It’s easier to buy production with 65 million shares than trying to sell 65 million shares in the market in financings, as that would result in an almost-eternal ceiling on the share price without any guarantee the required cash could ultimately be raised. The permitting process in Idaho is expected to cost around C$15M per year, so Integra would have had to continue to raise money while there was no guarantee on share prices and required warrant kickers. If the Florida Canyon mine (purchased at a deemed issue price of C$1.35 per share of Integra) performs as expected, Integra won’t need any external financing anymore. So while the ‘immediate’ dilution is high, it removes uncertainty, while the company may have had to issue the same amount of shares anyway, spread out over the next few years, to fund the permitting process. Integra’s management team looked at the big picture and the NAVPS accretion was likely higher with this deal than with annual capital raises over the next three years.

- The capex for this year has already been almost fully spent. When Integra takes possession of the mine, there is very little capex to be spent this year and the incoming cash flow can already be used to start getting the ball rolling for next year’s capex commitments.

- The project is highly levered to the gold price. At a gold price of $1800/oz, the pre-tax NPV5% is US$50M. This increases to US$141M at $2000 gold and US$259M at US$2340 gold. This means that at the current gold price of around $2400/oz, the after-tax NPV5% is likely close to US$225-250M which makes the acquisition price tag of around US$65-70M more palatable and actually a good deal. Also keep in mind all capex for this year (estimated at north of US$40M) will have been spent before Integra Resources takes possession of the mine.

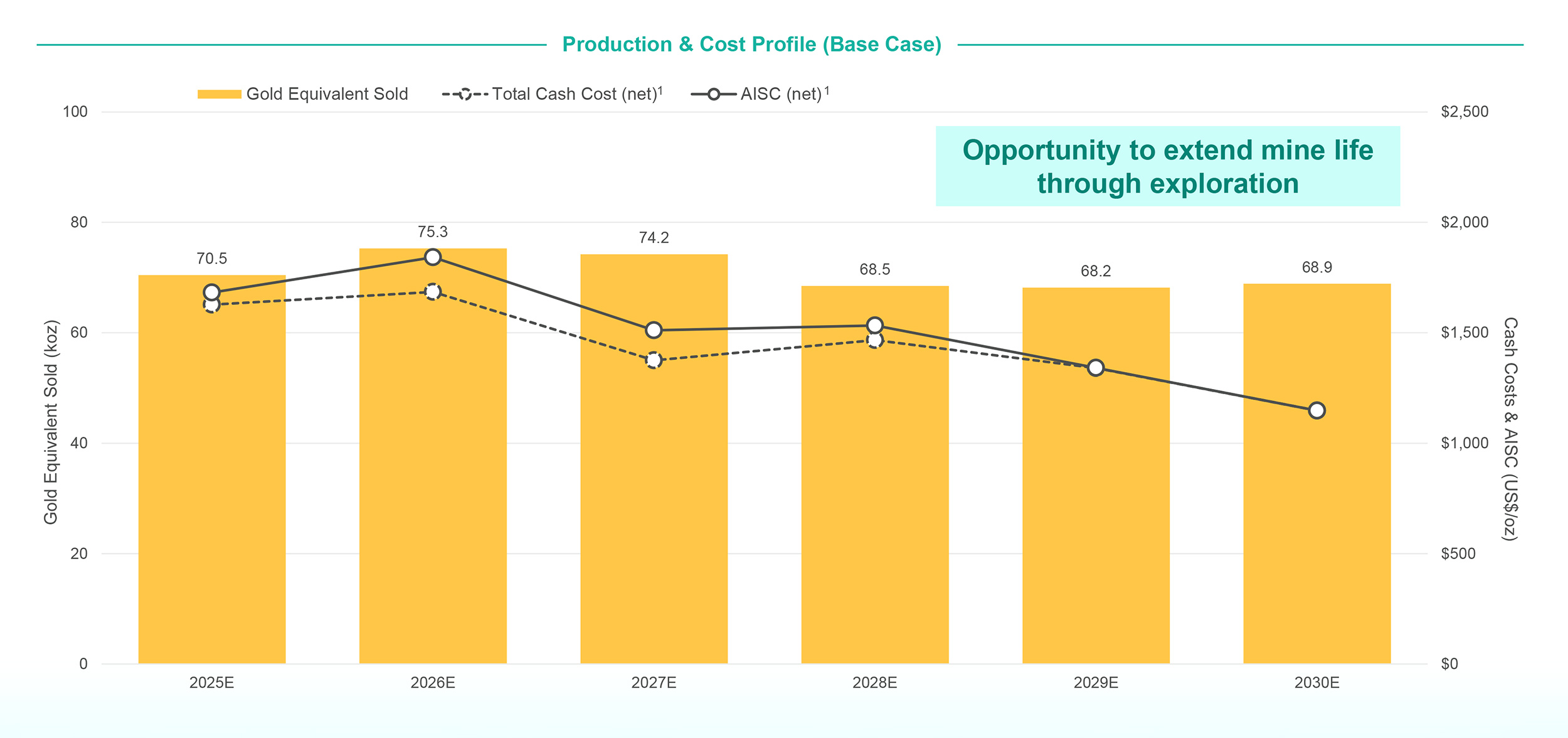

- As the strip ratio will decrease from 2027 on while the sustaining capex will also nosedive, the company anticipates the LOM all-in sustaining cost will be just US$1525 per ounce (as per the recent NI43-101 feasibility study on the asset). The first two years will be the most difficult years with an anticipated average AISC of around $1800/oz, before it drops to less than $1500/oz.

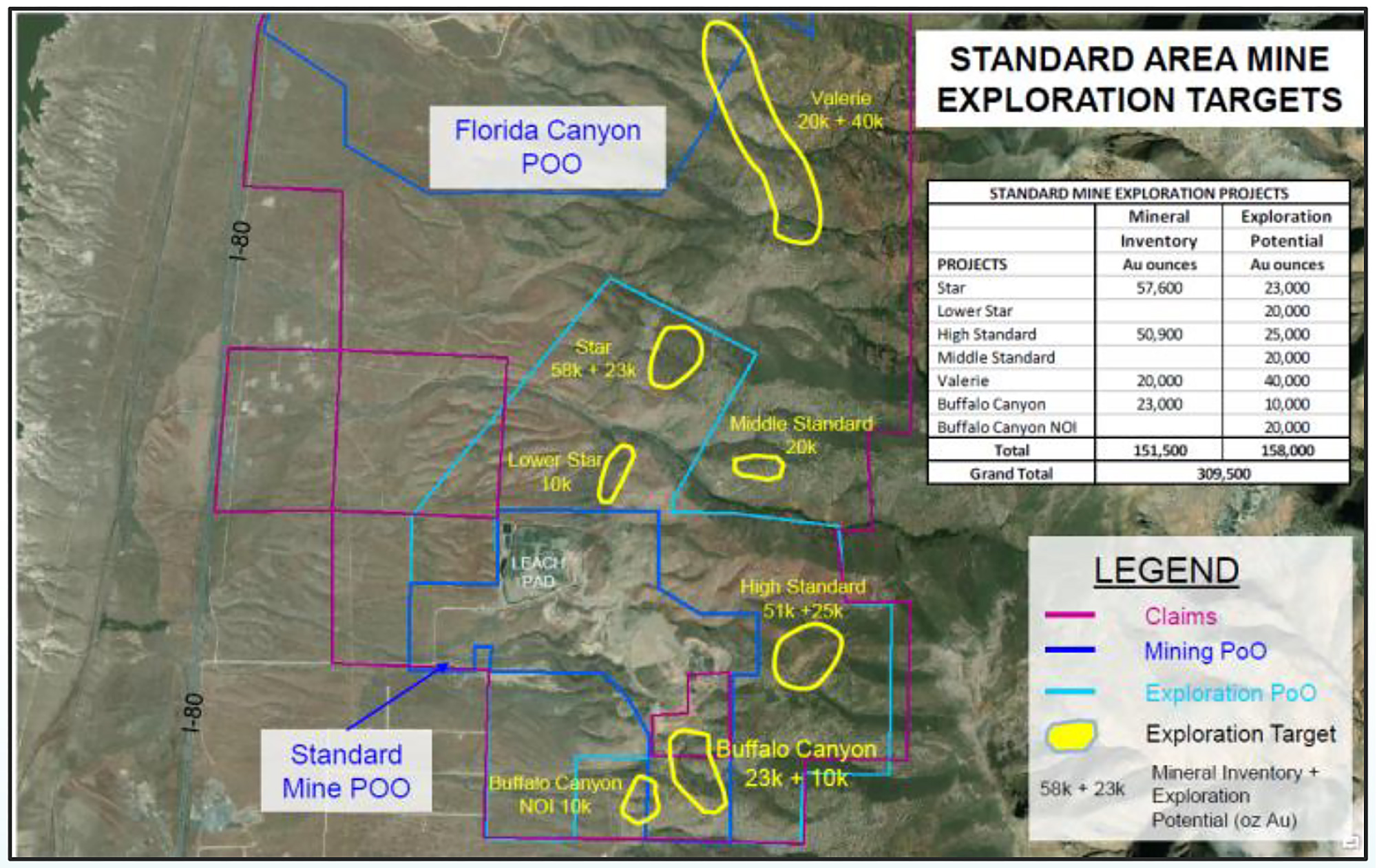

- The asset hasn’t been thoroughly explored in the past two decades and perhaps Integra will now include exploration in its annual operating budget at Florida Canyon. The company’s management team sounded upbeat to be able to convert some of the inferred resource into a higher category so it could ultimately end up in the mine plan. That would add more ounces and add to the mine life at Florida Canyon. The immediate surroundings of the mine are permitted for field studies and drilling.

- Argonaut Gold hired a new general manager for the Florida Canyon mine. Looking at his resume, Greg Robinson combines a multi-decade engineering background with the completion of an MBA. We like the combination of having practical experience while having an understanding of economics. It’s a good combination, and Robinson could use the experience and knowledge on the other projects in Integra’s asset portfolio when a development decision will be made.

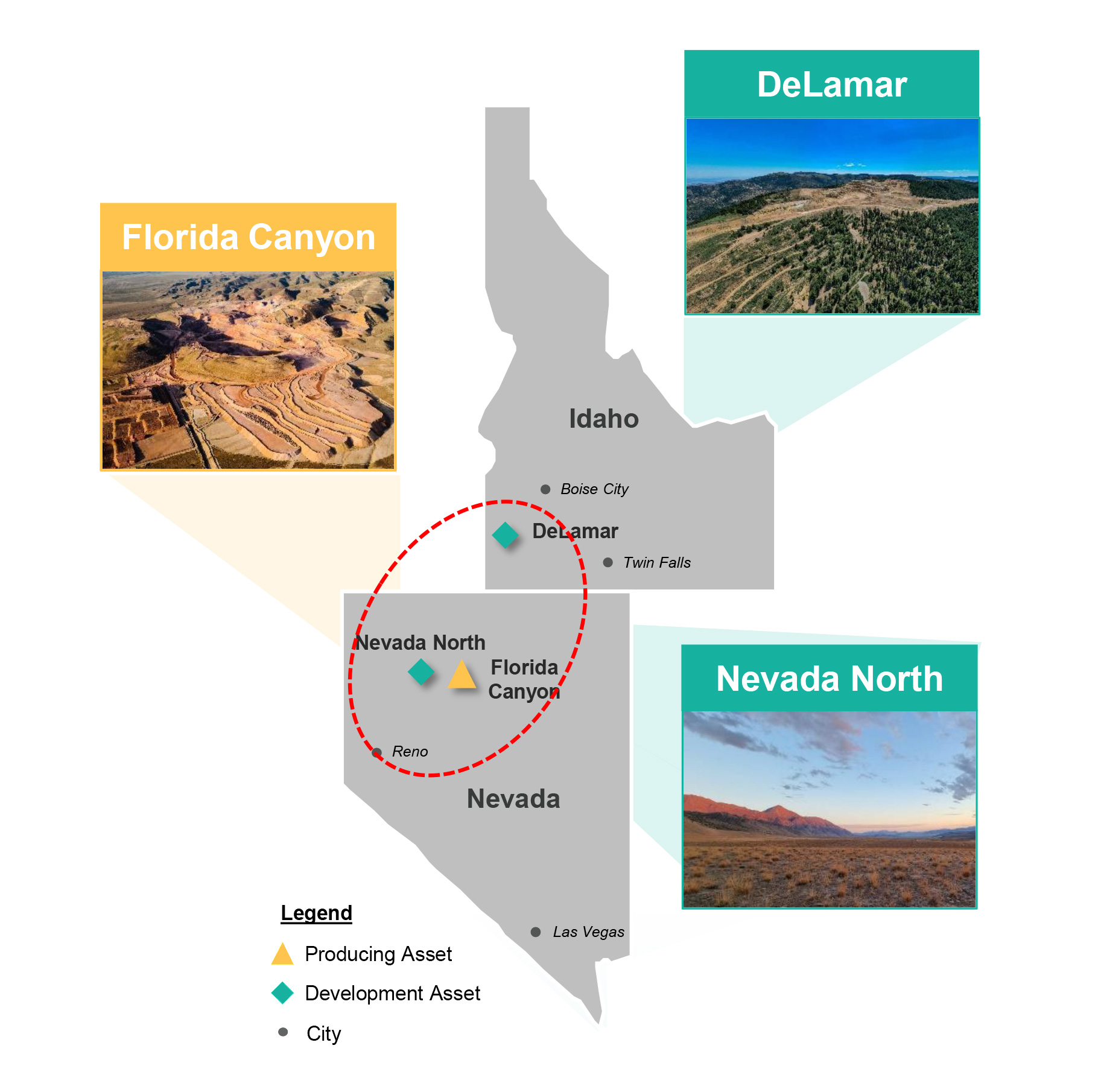

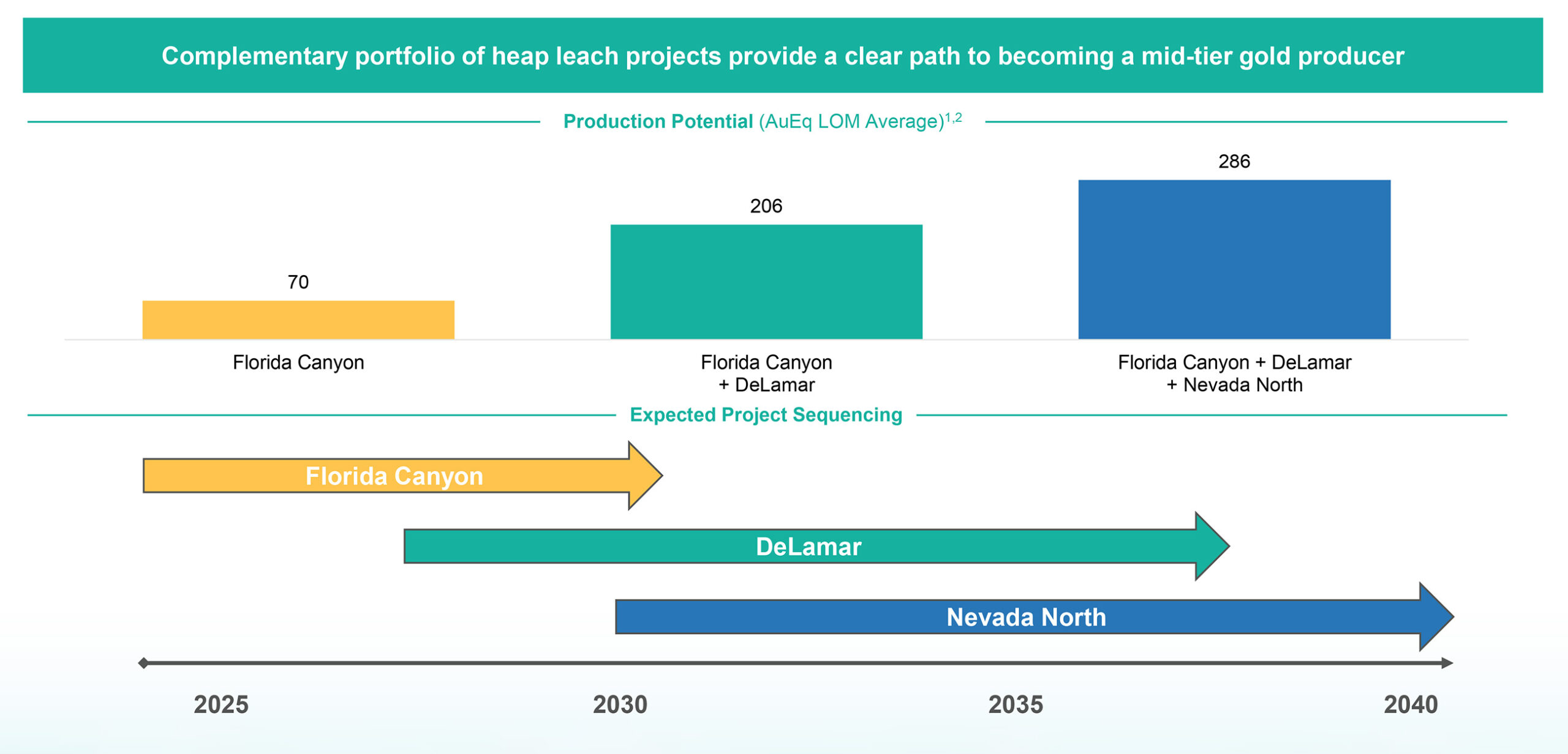

- Given the proximity of Florida Canyon to the Nevada North cluster (the combination of Wildcat and Mountain View), there could be capex savings further down the road as some of the equipment used at Florida Canyon could be used at Nevada North. And it goes without saying having an experienced labor force ready to hit the ground running at other heap leach assets is an important and valuable intangible. Nevada North and Florida Canyon also share the same BLM permitting office which is expected to beneficial from a permitting perspective.

DeLamar is located approximately a three-hour drive north from Florida Canyon in neighbouring Idaho. The operations team and Florida Canyon will be hugely beneficial to Integra as it looks to build and ramp up productions at DeLamar in the coming years. Mining labor is extremely competitive in the Great Basin, and having access to an existing workforce of open pit heap leach experts is a major advantage. Additionally, having an experienced heap leach mining team could help ease concerns to future DeLamar project financing lenders; and that’s an important intangible.

The negatives

- The pre-deal NAV using $2000 gold as a base case scenario and using Integra’s after-tax NPV5% of around US$450M for DeLamar and US$500M for Northern Nevada implied the global after-tax NPV5% was US$960M or C$1.3B (this was confirmed in the press release announcing the acquisition of Florida Canyon).

This means the stock was trading at approximately 0.10x NAV before the Florida Canyon deal. According to the technical report of Florida Canyon, the after-tax NPV5% at an average gold price of around $2000 gold (it starts of with $2200 gold and assumes a decreasing gold price in the next few years) was about US$128M, meaning Integra Resources used stock trading at 0.1x NAV to buy an asset for 0.5x NAV.

Granted, there is a bit of difference in how development projects and producing assets are valued, and a multiple of 0.5x NAV is definitely justifiable. But when all is said and done, Integra’s share count will almost double to 170M shares. At C$1.25 per share (US$0.925), the company is now trading at 0.16 times NAV, so about 60% more expensive. Note: Integra’s presentation mentions the company is trading at 0.25x NAV, and that is based on the consensus gold price and NAV estimates across the board. At this point in time we feel $2000 is an acceptable long term price but perhaps Integra uses a lower base case price to calculate its own NAV. - While the current gold price is working in Integra’s favor, we should not forget the average production cost and AISC will remain high for the next 24 months.

- The pressure will now be on Integra’s management and operational team to ensure the operations continue to run smoothly in the first few years. Although Integra now is a producer, it still is a single asset producer, owning a high-cost mine so the risk profile is still pretty elevated.

From an optimistic point of view, the cash flow from Florida Canyon could be an important part of the jigsaw puzzle

Integra Resources has always struggled to find a good balance between raising capital and keeping the permitting process in Idaho going. While the company was always able to raise the money it needed, it came at a hefty price and the most recent capital raise that was completed in March happened at a discount of almost 95% from the 2020 high. The company always raised the money, but the associated cost was pretty high. And as mentioned in the bullet points, the ongoing permitting process in Idaho is expected to cost C$15M per year.

Going back to the basics, the company is now exchanging 65 million shares in return for cash flow. A cash flow that should reduce or even completely cancel the need for the company to go back to the market.

The concurrent bought deal of subscription receipts (C$20M priced at C$1.35, no warrants, convertible in common shares when the deal closes) will also help Integra to maintain a healthy cash balance notwithstanding the anticipated incoming cash flow.

And that incoming cash flow could be the missing piece to unlock the value of the development projects. As the company patiently navigates through the permitting process for DeLamar it won’t be sidetracked by continuous capital raise efforts as the Florida Canyon production should take care of that. And if/when DeLamar (and later on, Nevada North) gets permitted, the multiple to the NAV should improve as well. The company received just 0.1x NAV for DeLamar in the pre-feasibility stage, while a permitted project in the feasibility stage should command a multiple of 0.3-0.35 times NAV and should result in a general rerating of the entire company.

Conclusion

Admittedly, we were scratching our heads when we saw Integra was heading towards a 67% dilution in the share count to acquire Florida Canyon Gold. The Florida Canyon mine has never been a real cash cow, but the appointment of the new general manager has changed things, and the potential to further extend the mine life beyond the current seven or eight years appears to be real.

And although the total share count (including the impact of the subscription receipt financing) will almost double compared to a week ago, Integra deserves the benefit of the doubt. While Florida Canyon will remain a high cost gold mine in the first few years after Integra takes possession, the anticipated lower strip ratio and lower sustaining capex from 2027 on should expand the margins. And that incoming cash flow could be very useful to help funding the equity portion of the DeLamar capex, as we anticipate construction at DeLamar to be in full swing at that point as the current permitting process seems to indicate a Record of Decision to be obtained in 2026.

The main risk that could torpedo the deal’s merits is the gold price. But the fact that the gold price trades at $2400/oz every day is beneficial to Integra Resources and its long-term plans, as the acquisition gets derisked day after day.

Disclosure: The author has a long position in Integra Resources. Integra Resources is a sponsor of the website. Please read the disclaimer.