It took Integra Resources (ITR.V) almost three months to follow up on its excellent assay results that were published in June, but the recently released results were well worth the wait. The new drill results confirm Integra’s exploration theory, confirms the resource expansion to the southeast of the Sullivan Gulch zone and validates the use of an IP survey to detect new gold targets.

It took Integra Resources (ITR.V) almost three months to follow up on its excellent assay results that were published in June, but the recently released results were well worth the wait. The new drill results confirm Integra’s exploration theory, confirms the resource expansion to the southeast of the Sullivan Gulch zone and validates the use of an IP survey to detect new gold targets.

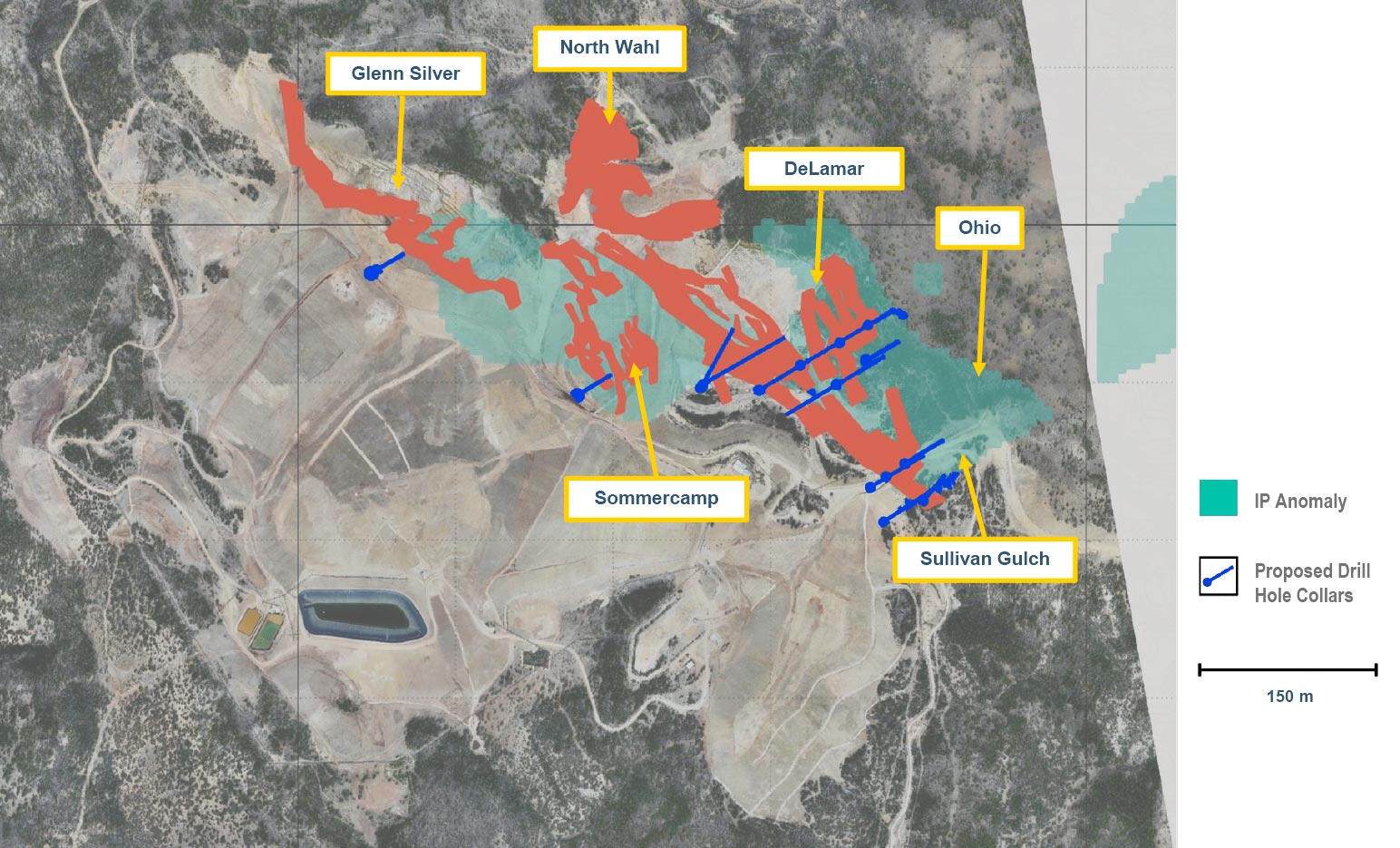

Sullivan Gulch

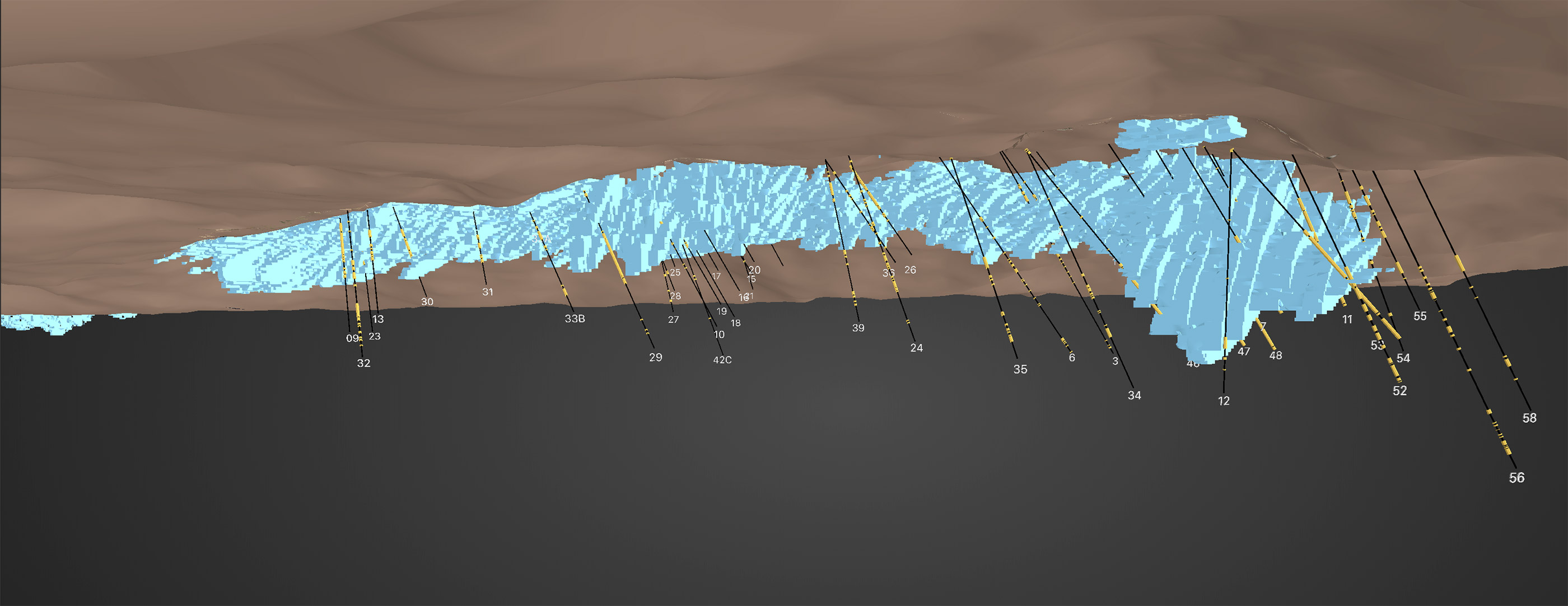

Holes 46, 47 and 48 were drilled on the southeast side just outside of the historic pit that has been backfilled, and the assay results of these three holes were the best results of the entire release. Drilling almost 328 meters of 0.51 g/t gold and 19.36 g/t silver is an excellent long interval confirming the thickness of the mineralized zone. And don’t let the depth of holes 46 and 47 (with mineralization starting at a depth of respectively 261 meters and 264 meters) fool you. The cross section shows why the depth of holes 46 and 47 is relatively irrelevant:

Any potential open pit operation at Sullivan Gulch would have to dig through the mineralized zone encountered in hole 48 anyway, so it’s not like Integra Resources would have to excavate 200 meters of overburden. It would be really interesting to see what Integra’s drill bit would encounter further to the left of hole 46 in the cross section image. The thick intervals in holes 46, 47 and 48 are outlining a zone which appears to be 10-15 million tonnes and this could result in a meaningful upgrade of the existing resources. As a reminder, the current inferred resource estimate has an average grade of 0.41 g/t gold and 24.3 g/t silver for a gold-equivalent grade of 0.70 g/t.

This tells us two things.

First of all, the gold is hosted by the latite and porphyritic rhyolite zone, while the banded rhyolite zone appears to be pretty barren (which is consistent with the exploration theory). This could indicate the gold mineralization is just continuing towards the northeast of hole 48 (which is towards the right on the previous image), and we would like to see Integra completing a few holes in that direction to figure out how widespread the gold mineralization is.

Secondly, any open pit operation would obviously start on the right hand side of the image, and will go after the low-hanging fruit first. Sure, the grade in hole 48 is much lower than the grade in holes 47 and 46, but because the gold mineralization starts much closer at surface at hole 48, it would only make sense to start mining there. This will allow Integra to immediately put pay dirt on the leach pad (or in the mill, depending on Integra’s preferred production scenario) and defers the stripping of the overburden on the left hand side to the sustaining capex. This should have a positive impact on the economics as ITR could avoid a pre-strip capex before it puts the first tonne on the leach pad.

If you just look at the table with the assay results, you might indeed be underwhelmed by the depth of holes 46 and 47. But there’s more to the story than just numbers…

Integra also completed a few holes further towards the east-southeast of the 46-47-48 series, and confirmed the existence of near-surface mineralization.

The grades are a bit lower than the aforementioned holes, but the mineralized zone appears to be reasonably thick, and more importantly, consistent. These five holes were drilled approximately 200 meters away from holes 46-47-48, and with this series of step-out holes, Integra is really building tonnage. A mineralized envelope of 200 by 200 by 150 meters at a density of 2.65 gets you a total tonnage of approximately 16 million tonnes.

Other mineralized zones at DeLamar

Extending the gold and silver mineralization at Sullivan Gulch is an important step for the company, as it’s zeroing in on expanding the resource estimate to 5 million gold-equivalent ounces.

But there’s more than just the old DeLamar open pit and the Sullivan Gulch zone. Integra Resources has also drilled a few holes at the Sommercamp and Glenn Silver zones (erroneously spelled as ‘Glen’ in the technical report).

The drill program on these zones is predominantly meant to confirm the existing inferred resource estimate, but will also test the surrounding land for potential extensions of the mineralization. Kinross Gold, the previous owner of the DeLamar mine, did explore for gold on these zones, but it looks like the senior producer just didn’t drill deep enough. Whereas Integra has been drilling holes up to a depth of 250 meters, Kinross’ drilling was limited to just 100-120 meters from surface.

Florida Mountain: There’s the high-grade!

Keep in mind the DeLamar deposit is just one part of Integra Gold’s Idaho operations. Just five kilometers from DeLamar (as the crow flies), Integra also acquired the Florida Mountain gold-silver project, which currently hosts an inferred resource estimate of 871,000 ounces gold-equivalent at an average grade of 0.74 g/t AuEq. The gold-equivalent resource consists of 675,000 ounces of gold and almost 17 million ounces of silver, and we are definitely anticipating a resource boost. Perhaps not immediately (or at least not a substantial resource boost) after the current nine drill holes, but further down the road there’s a very good chance of Florida Mountain to become a multi-million ounce gold deposit.

The mineralized zones encountered in the first nine holes at Florida Mountain appear to have been successful in hitting near-surface mineralization. Drilling 20 meters at 1.16 g/t AuEq starting from surface is an excellent result, and as you can see on the previous table, most of the economic grade ore was intersected within the first 100 meters from surface.

Integra Resources also immediately (re-)discovered the high grade veins but much to our surprise, these veins were encountered much closer to the surface than we expected. 3 meters at 14 g/t AuEq starting at less than 24 meters down-hole and 2.74 meters containing 10.57 g/t AuEq at a depth of just 19 meters down hole are excellent grades for near-surface mineralization.

Integra Resources has completed 9 drill holes for a total of 2,400 meters, and the first drill results are very encouraging as the drill bit intersected both the thick low-grade mineralization as well as the high-grade veins the company has been chasing. This makes the Florida Mountain project quite unique as records indicate the average grade in the late 1800’s was almost 1 ounce of gold-equivalent per tonne of rock, followed by a period of low-grade production by Kinross Gold, which trucked the ore from Florida Mountain to DeLamar’s mill, where the recovery rates were an excellent 95% for the gold and 75% for the silver. On top of that, column leach tests have indicated recovery rates of 85% for the gold and 54% for the silver, which further emphasizes Integra’s expectations to consider DeLamar and Florida Mountain as heap leach operations.

Confirming IP surveys are effective

The exploration success also seems to confirm Integra’s approach to use Induced Polarisation surveys on its land package to define the gold zones. According to the company, there was a strong correlation between the high IP chargeability anomalies and the existing inferred resource estimate.

Integra wanted to follow up on this correlation and used IP surveys on other parts of the DeLamar project. A first success was the discovery of more gold mineralization at the Sullivan Gulch zone (confirmed by the drill results discussed earlier in this update report). It also looks like the Sullivan Gulch mineralization is extending further towards the southeast, and ITR will very likely prioritize drilling those zones to define a large in-pit resource.

Conclusion

Integra Resources kept the market waiting for more drill results, but we are definitely pleased with what we see. There’s a very clear path forward to a total resource estimate of 5 million gold-equivalent ounces at the DeLamar-Florida Mountain zones at a higher grade than the current inferred resource. Integra Resources has started a metallurgical test work program, and that will be an important box to tick, and it will enable us to start building an economic model to determine the viability of the project.

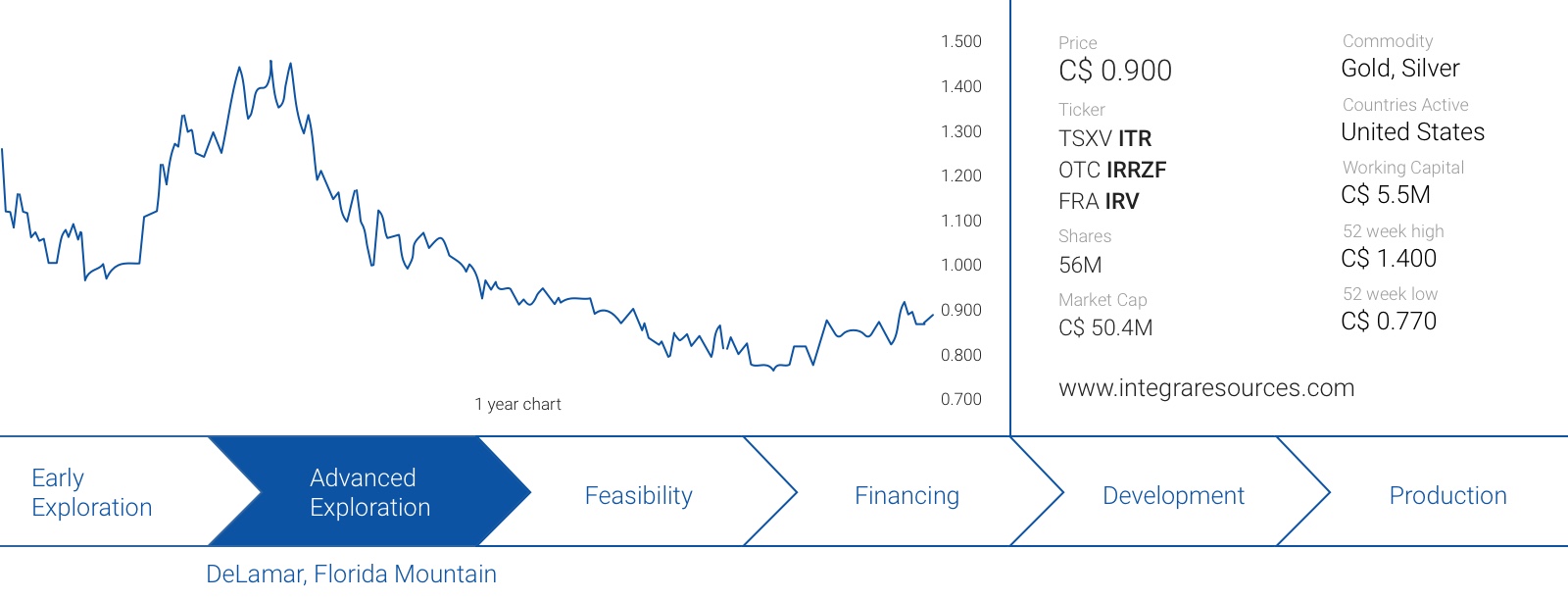

With a current market capitalization of just C$50M, we feel like Integra Resources is offering a very compelling value-for-money proposition.

The author has a long position in Integra Resources. Integra Resources is a sponsor of the website. Please read the disclaimer