We like European stories, but unfortunately most of the projects are pretty early stage as mining has not been encouraged in the European Union. The mindset is definitely shifting though, as the EU seems to be aware it could make sense to become less reliable on imports from foreign countries to reduce the supply chain risk.

There are only a handful of ‘real’ and reliable mining jurisdictions in Europe, and Finland is one of them. Finland does have a mining history and recent exploration successes in Lapland have highlighted Finland as an attractive destination, both from a prospectivity point of view as well as from a legal framework perspective as the country has an established regulatory path towards permitting mines.

Mawson Finland (MFL.V) was recently spun off from Mawson Gold (MAW.V), with the advanced-stage Rajapalot gold-cobalt project as its main asset. That cobalt angle could be quite interesting further down the road as we can imagine mining projects with a strategic metal credit have a leg up in the greater scheme of things.

Rajapalot isn’t a grassroots exploration project as a Preliminary Economic Assessment was completed before the IPO of the company using the drill data up to 2021. And although that PEA may have been compiled ‘too early’ on a resource smaller than 1 million ounces of gold and is currently already outdated given the additional drilling that has taken place, it does provide an excellent stepping stone to expand the resource, update the mine plan and update the economics of the project. But as we will explain in the report, the project would also work in its current form as mining in Finland is cheaper than you’d think.

The company has actively promoted not only the exploration permitting but also the mine permitting processes. After preparing the PEA, Mawson Finland started the environmental impact assessment procedure and has already submitted the EIA program to the authorities. The authority has issued a statement on the EIA program, based on which the company can now move on to the next stage, i.e. the preparation of the actual EIA. The Regional Council and both municipalities in whose areas the Rajapalot project is located have also started the zoning processes which will be advantageous to the mining project as it paves the way to apply for the actual mining permit further down the road.

In the future, changes to national legislation based on the EU´s Critical Raw Materials Act will, among other things, promote the permitting of projects producing critical and strategic raw materials such as cobalt.

The PEA at Rajapalot already paints a positive picture

It goes without saying the Rajapalot gold-cobalt project is Mawson Finland’s flagship asset. The project is located in Northern Finland Lapland region and consists of a total of just over 41,000 hectares of land (including the reservation notification areas). The existing resource is hosted on two of the already granted tenements.

One element we would like to get out of the way immediately: although some parts of the land package are Natura 2000 designated areas, Mawson Finland does not expect to run into any major issues here. The project is per definition an underground mine and all required infrastructure can rather easily be built outside of the designated Natura 2000 areas. As per the PEA, the image below shows the infrastructure would be located outside of the Natura 2000 area (the green line).

So, yes, the company will have to be mindful and respectful of the Natura 2000 areas (which represent 17% of the total surface area), but there is no need to do any meaningful surface construction in those areas and it could be possible to have àll surface infrastructure outside of the Natura 2000 zones. There are no Sami or any other first nation community issues on the project.

The history of the project is quite interesting. Exploration kicked off in the 1950s as the Rompas-Rajapalot area was explored for molybdenum and uranium. In fact, it was Areva (now Orano), the large French nuclear conglomerate that first discovered gold (the discovery was made at the Rompas zone, located approximately 8 kilometers west of the main Rajapalot zone) but not until 2007, more than 50 years after initial exploration started in the area. In 2010, Areva decided to exit the area and sold the assets to Mawson which discovered the mineralisation at Rajapalot in 2012 (8 kilometers east of the initial gold discovery at Rompas).

Between 2013 and 2022, Mawson completed almost 90,000 meters of drilling in 567 holes, and of course every single one of those holes is well-documented with all data easily accessible.

Drilling was mainly focusing on the Palokas zone (as shown below) but the drilling density and location of the holes on the other zones was sufficient to compile a maiden resource calculation in the summer of 2021 and the underground block model was ultimately used to complete the Preliminary Economic Assessment.

As mining costs are low in Finland (Agnico Eagle reports a mining cost of less than 35 EUR/t at its underground Kittila mine, and the independent consultants used a similar cost for the Rajapalot PEA), the independent third party that completed the resource calculation was able to use a cutoff grade of just 1.1 g/t gold-equivalent. That sounds low for an underground mine, but it is definitely justifiable.

As you can see below, the maiden resource contains a total of 9.8 million tonnes at an average grade of 2.8 g/t gold and 441 ppm Cobalt for a total of 867,000 ounces of gold and 9.5 million pounds of cobalt on a contained basis.

The Palokas zone contributes approximately 60% of the mineralization and is for sure the main zone but the other, smaller, zones could and should be seen as interesting satellite deposits to feed one central processing plant.

This resource was used to work on a PEA, and in hindsight, this likely has been a contributing factor why Mawson Gold was held back, and why even Mawson Finland is currently trading at a valuation of just C$36M. Markets tend to be backward-looking, and the moment a company publishes an economic study, the market sometimes thinks that’s ‘it’ and there is no real additional upside potential anymore. But that’s not always the case, and it is definitely not the case at Rajapalot as the recent exploration activities unveiled additional exploration potential at depth and highlighted the prospectivity of some of the satellite zones.

And in hindsight, completing a PEA on a resource with less than 900,000 ounces gold perhaps wasn’t the best idea with a backward-looking investor base, but we also believe that’s where the opportunity is for Mawson Finland now. Because even though the asset base was pretty small, the outcome of the PEA was actually very robust.

The main contributor to the strong economics was the surprisingly low upfront capex. The initial capex was budgeted at just US$191M and already included a 20% contingency. And although the average gold grade of 2.8 g/t isn’t very high for an underground gold mine, the cost of doing business in Finland is pretty low as well. According to the data the independent party used to compile the economics, the underground mining cost is estimated at just under US$35 per tonne of mill feed (including the backfill costs as the mine plan uses a cut and fill mining method), followed by just $16.9/t in processing costs. This means the total cost per tonne of mill feed was estimated at just under $56.

That’s a remarkably low operating cost, and this indicates the grade of 2.8 g/t gold (in combination with the cobalt credit) works. In fact, the cobalt by-product credit would cover about 15% of the total cost per tonne (using the current cobalt price of around $24,000/t, an 87% recovery rate and a 90% payability percentage).

When the study was put together, the cobalt price was substantially higher and the independent consultants used a cobalt price of $60,000/t in their base case scenario. That’s more than 100% higher than the current cobalt price and that cobalt price should be taken with a grain of salt (and we’ll explain the impact of the lower cobalt price in a sensitivity analysis).

Looking at the base case scenario, which uses a gold price of $1700/oz and the aforementioned $60,000/t cobalt price, the after-tax IRR came in at 27% while the after-tax NPV5% was US$211M. This already yields a NPV to capex ratio of 1.1, but there’s more. The sensitivity analysis below shows that using a gold price of $2000/oz, the after-tax NPV5% immediately jumps by in excess of 50% to US$333M. Also important, the mine would be yielding US$442M in cumulative cash flow in the first five years of the mine life, reducing the payback period and increasing the IRR to 37%.

As the image above shows, for every $150 increase in the gold price, the after-tax NPV5% increases by approximately US$60M. While you cannot extrapolate this indefinitely (the higher average tax rate will result in slightly lower diminishing returns due to the different depreciation schedules), we anticipate the after-tax NPV5% at $2300 gold to be around US$425-440M.

While that is still based on a cobalt price of $60,000/t, the lower cobalt price will have a noticeable impact, but not a fatal impact on the economics of the mine. In years 1-3, the cumulative cobalt production is approximately 532 tonnes (not thousands of tonnes, but just 532 tonnes). Assuming a payability of 90%, that’s approximately 480 payable tonnes of cobalt. At $60,000/t, the cobalt would generate approximately US$30M in payable revenue, at $24,000 tonnes this would yield US$11.5M in net revenue. That’s a difference of $18.5M in the first three years of the mine life. Again, that will be a noticeable difference, but it wouldn’t be a deal breaker as Mawson Finland would only see the contribution from the by-product credit decrease from $116/oz to $45 per ounce. And the $71/oz it ‘loses’ on the cobalt credit side, it is gaining on the revenue per ounce of gold sold.

Also important: there only is a 0.15% NSR payable to the Finnish government while a new mineral concentrate tax of 0.6% has recently been introduced as well. As the property is virtually unencumbered by a royalty, selling a NSR could provide a meaningful contribution to the equity component of a construction financing package. Just to give you an idea, a 1% NSR on the current mine plan using $2000 gold and $24,000 cobalt would generate US$14.5M in net revenue to the buyer and would likely fetch a price of US$5-10M. But of course, Mawson Finland’s management would be crazy to sell an uncapped NSR this early in the game and we would expect a potential royalty sale in conjunction with a financing package in a few years.

The upside potential using a higher gold price and adding more ounces to the mine life

As mentioned above, the gold price has a major impact on the NPV of the project and for every $150 fluctuation in the gold price, the after-tax NPV5% moves by approximately US$60M. We also argued that publishing a PEA on a resource with less than a million ounces of gold perhaps wasn’t the best idea as the market appears to be too backward-looking, but that issue can easily be rectified.

While Mawson Finland can easily use a higher gold price for its next economic study, let’s also not forget the company has just completed an additional 11,400 meter drill program and will be gearing up for another winter drill program. It’s not a secret Mawson Finland would like to increase its existing resource by approximately 50% and this would bring in an additional 350,000 ounces of recoverable gold into the mine plan.

Assuming an AISC of around $1000/oz (we are taking cost escalations towards the end of the mine life into account as well as the lower cobalt price which reduces the by-product credit) and using a gold price of $2,250/oz, the additional 350,000 ounces would result in approximately US$525M in additional pre-tax and undiscounted cash flow. Applying the 20% corporate tax rate and assuming the additional ounces are added towards the end of the mine life, a 50% resource increase would likely add somewhere between $200M and $250M to the after-tax NPV5%. So even if the initial capex would increase by 50% compared to the PEA, the company still has a very clear path forward towards a US$500M NPV5% at US$2300 gold.

Of course these are just assumptions and readers are cautioned to rely on the official publications by the company. But we just wanted to paint the picture the combination of higher metal prices and a larger resource estimate could have a very positive impact on the economics of the Rajapalot gold-cobalt project.

Recent exploration results

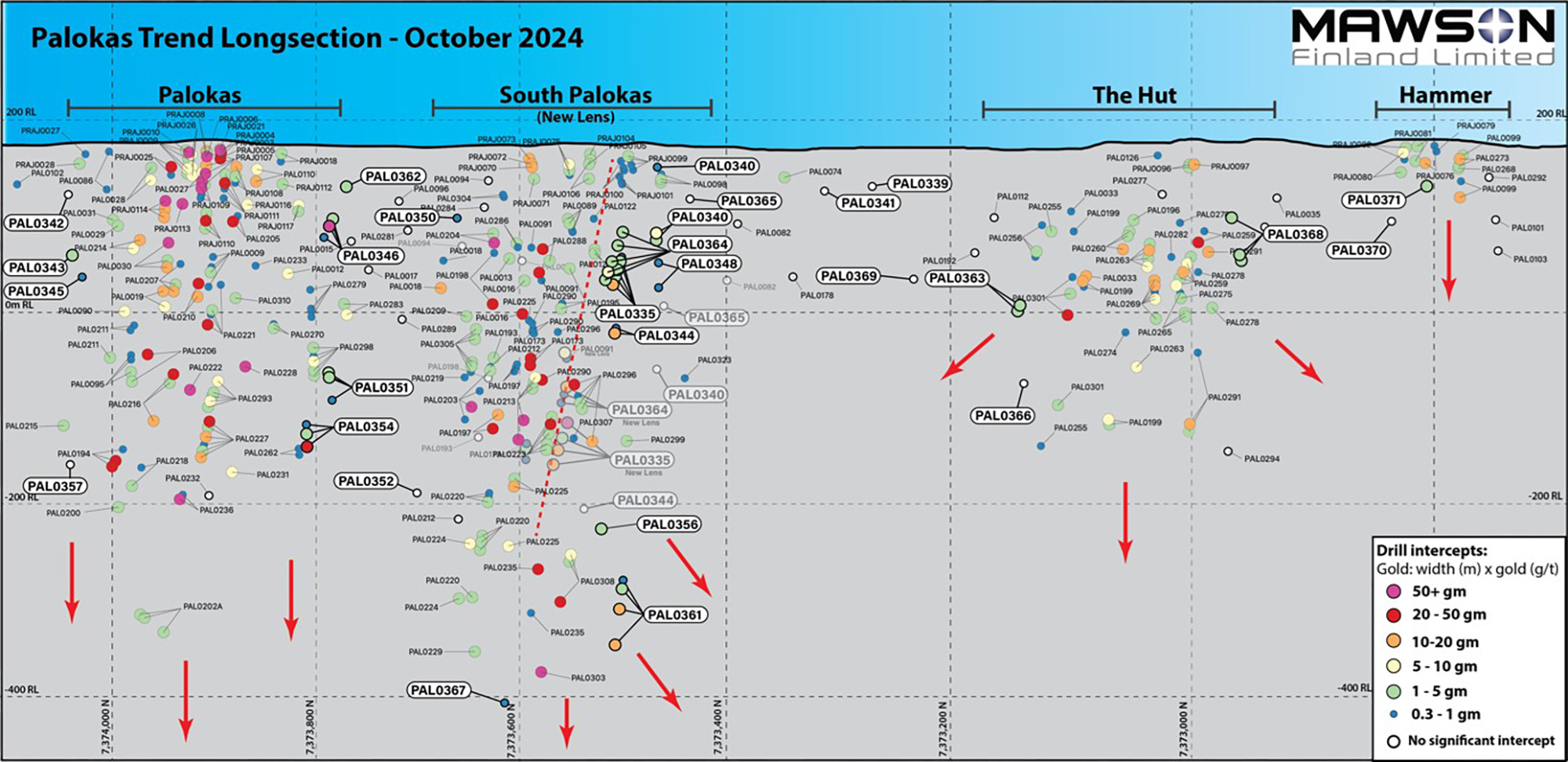

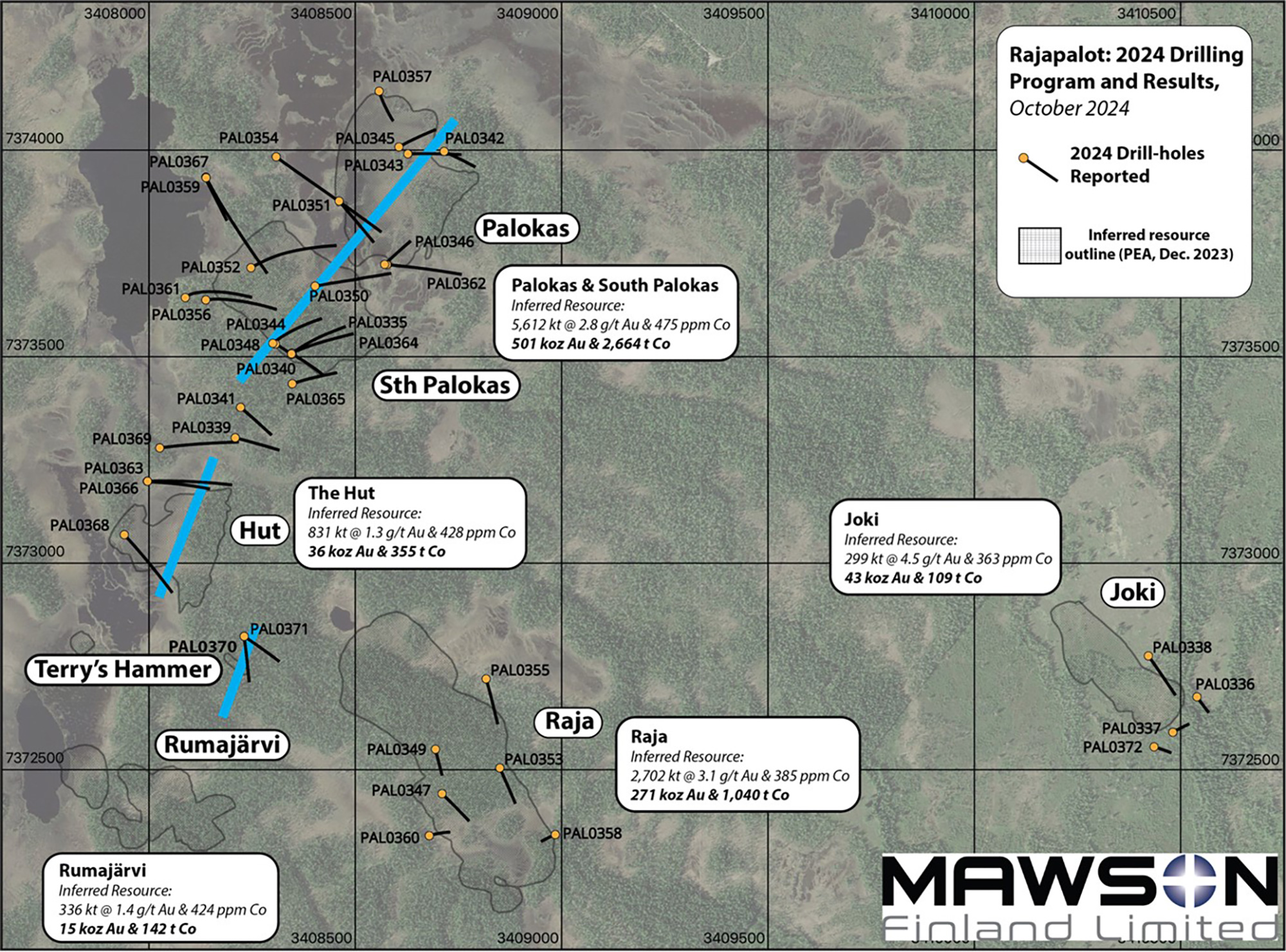

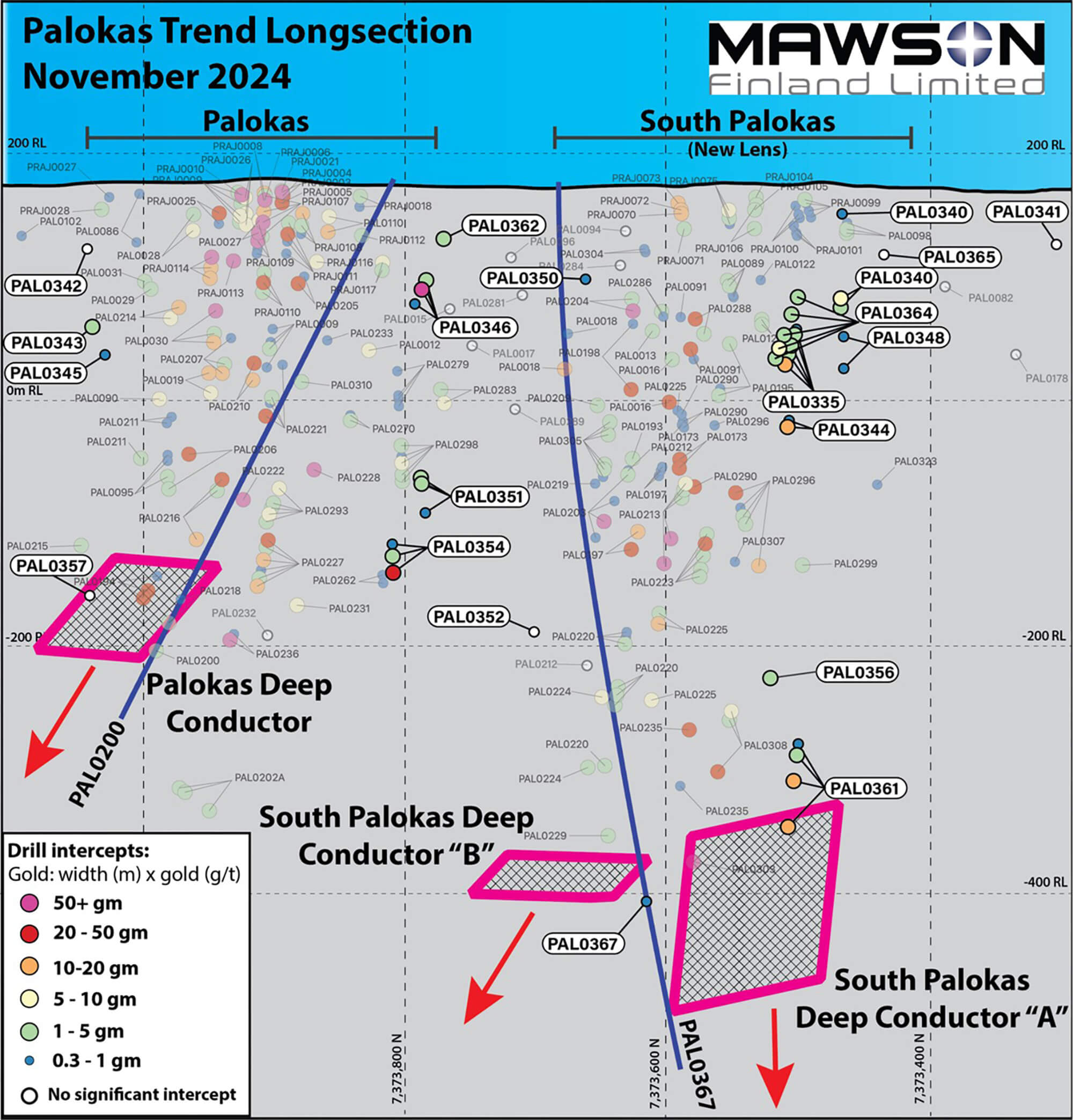

Mawson has now released all assay results from its 2024 drill program on its flagship Rajapalot gold-cobalt project in inland. The drill program consisted of almost 11,400 meters of drilling in 38 holes and was designed to further improve the knowledge of the mineralization on the property while also expanding the known gold mineralization. This drill program was conducted with three drill rigs between January and April, and the results were held back at the lab during the IPO process of the company. Twenty of the holes were drilled at and around the Palokas and South Palokas zones, with additional targets being drilled by a handful of holes as well.

At the Palokas zone, the company was successful in demonstrating the mineralization in the southern end of the gold-cobalt system appears to continue, with a very intriguing interval of 7 meters containing 9.1 g/t gold and 706 ppm cobalt. Additionally, at Palokas and South Palokas, the drill bit intersected gold and cobalt in several step-out holes, which indicates the total size of the mineralized body may very well be expanded at depth as both zones remain open at depth.

On top of that, the footwall below the South Palokas zone contained a pretty thick interval of 21.75 meters containing 5.25 g/t gold and 515 ppm cobalt (including an even higher grade interval of 3.2 meters containing 21.61 g/t gold and 373 ppm cobalt). The assay results of the 2024 drill program will be very helpful for Mawson Finland to further expand the resource beyond the current 9.8 million tonnes of 2.8 g/t gold and 441 ppm cobalt for a total of 867,000 ounces of gold and 4,300 tonnes of contained cobalt.

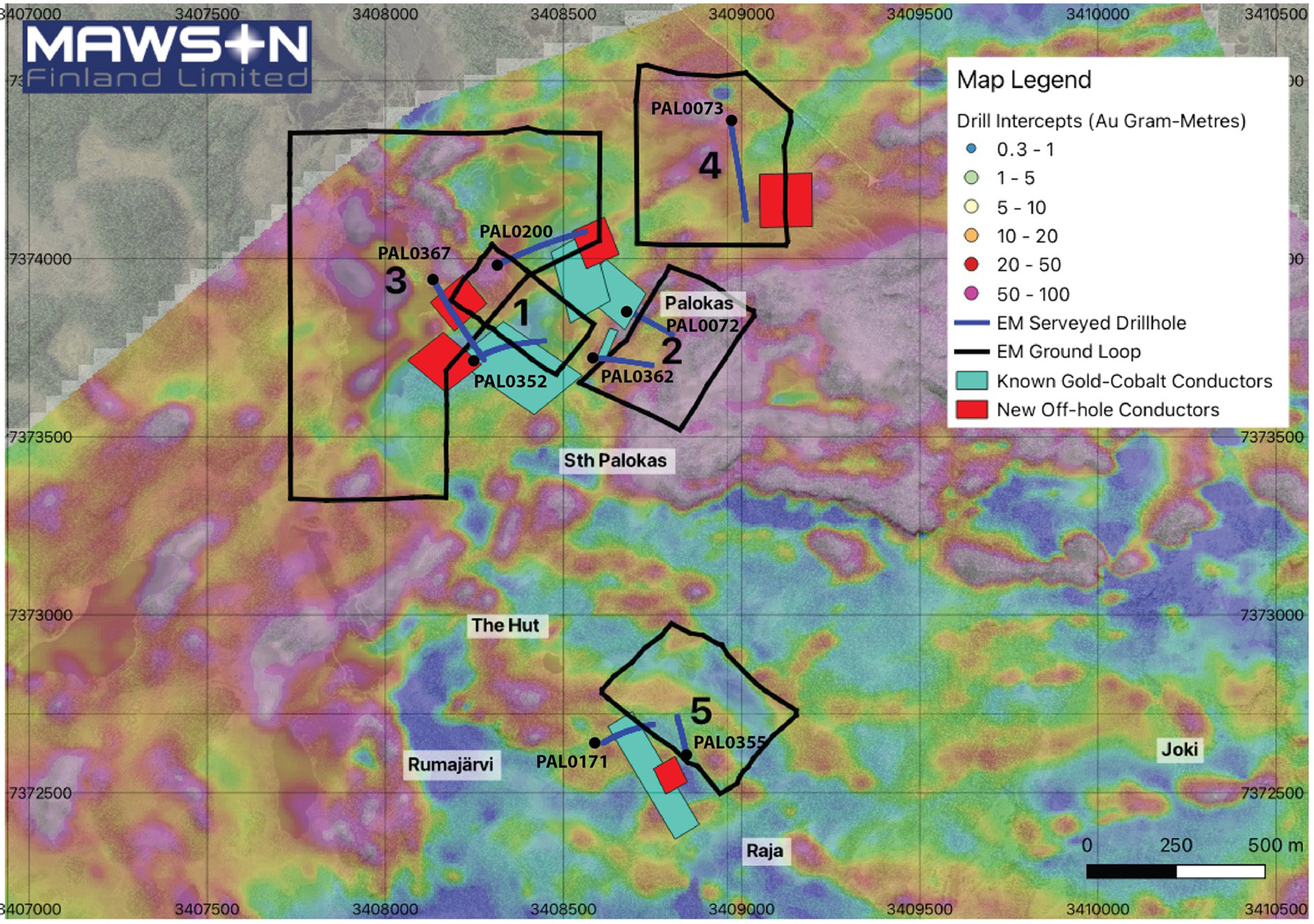

On top of that, Mawson Finland also released the results from its downhole electromagnetic exploration program, which found multiple deep conductors at Rajapalot, including in the area down dip and down plunge of the Palokas and South Palokas zones. These conductors could indicate the gold-cobalt mineralization continues at depth, and that bodes well for the exploration potential below the currently known resource. Other conductors highlighted the potential of some other zones, including a deep conductor located along strike from the Palokas zone, but approximately 500 meters to the north east.

The downhole EM survey encountered no fewer than five conductive targets within or nearby the current inferred resource category, and we expect Mawson to drill-test some of those areas in the upcoming winter drill program. Meanwhile, Mawson Finland will conduct additional EM geophysical studies, in addition to a sub-audio magnetic ground survey program which is currently underway at the Rompas area and its surroundings, which is located approximately 6 to 8 kilometers east of Rajapalot.

The management bonuses and incentive options are correlated with shareholders interests

The prospectus published in conjunction with the Initial Public Offering of Mawson Finland also contained very interesting details on how Mawson Finland deals with management options. Quite often we see how ‘incentive options’ rarely are incentive options as most companies price them at the market price at the time of issue.

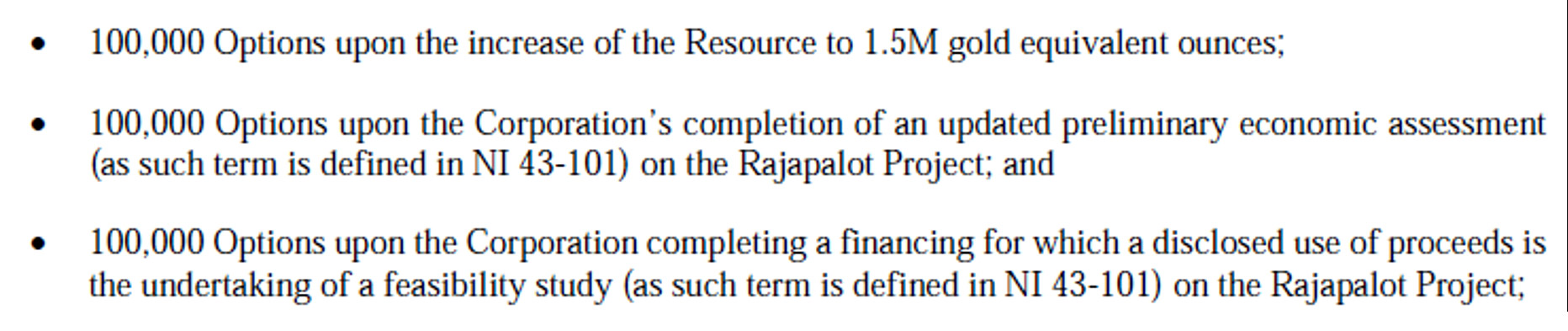

Mawson Finland does it different. It’s perhaps the easiest to explain when we pull up the option package awarded to Executive Chairman Neil MacRae.

As you can see above, he was awarded 300,000 options, but the vesting terms are intriguing as they truly align MacRae’s interests with the best interests of the shareholders. In case the resource update does not deliver the anticipated increase, the 100,000 options subject to reaching the 1.5Moz AuEq milestone simply will not vest.

Additionally, it’s in the shareholders’ best interest to have an updated PEA as well, while raising the funds to complete a feasibility study ensures the project continues to move forward. And in case Mawson Finland is unable to complete the three milestones above, not a single one of MacRae’s options will vest. And given their intrinsic value of a few hundred thousand dollars, we are quite confident MacRae will try to achieve the milestones.

There is only one way for management to ensure the options are vested even if not all milestones are met, and that is achieving a share price exceeding C$3 for a period of 120 consecutive days. C$3 is about 55-60% higher than the current share price, and even if the company doesn’t achieve the aforementioned milestones, investors should be fine with a substantial share price increase. And if the share price doesn’t reach the C$3 level while the milestones aren’t met either, the management options simply will not vest.

Conclusion

Mawson Finland has a pretty advanced project for a company that came out of the gate with a market capitalization of just C$36M. Although the market appears to be sceptical of the relatively ‘small’ resource, the existing PEA indicates the gold-cobalt resource indicates the project has a viable path forward, using $1700 gold and $60,000 cobalt. And of course, the lower cobalt price is compensated by the substantially higher gold price. On top of that, the current resource expansion drill program should also add more tonnes to the resource and the mine plan, creating additional value.

Mawson Finland came out of the gate pretty strong right after its IPO, but the share price isn’t immune to the recent weakness on the gold markets in general. At the current share price, the market cap is just while the company still has approximately C$3M on its bank account.

Disclosure: The author has a long position in Mawson Finland. Mawson Finland is a sponsor of the website. Please read our full disclosure.