When Oroco Resource Corp (OCO.V) released the outcome of its Preliminary Economic Assessment on its flagship Santo Tomas project in October of last year, there wasn’t anything to be really excited about. Yes, that first PEA confirmed the economic viability of the flagship Santo Tomas project but with an after-tax IRR of 17.3% using 3.85 copper, there wasn’t a whole lot of wiggle room for a potential acquiror to generate a double digit IRR on Santo Tomas after factoring in the purchase price. Note: there are – as far as we know – no negotiations to sell the company at this point, but Oroco isn’t exactly keeping it a secret they would like to sell the asset and doesn’t consider themselves to be mine builders. Considering that CEO Lock’s employment contract contains a bonus expressed as a percentage of a potential sale price of the company, it is clear what Oroco’s intentions are.

But in order to find a potential buyer, the asset needs to work. Fortunately, the company and its independent consultants were able to identify several possibilities to optimize the results of the study. Now, ten months after the initial study was published, Oroco has released the results of a second, optimized and updated PEA. And the economics (both the NPV and IRR) are substantially better than in the first version (even if you’d leave the $0.15 higher copper price out of the equation).

| Commodity | Unit | Price |

|---|---|---|

| Cu | US $ / lb | 4.00 |

| Mo | US $ / lb | 15.00 |

| Au | US $ / t.oz | 1,900 |

| Ag | US $ / t.oz | 24.00 |

Now the after-tax IRR comes in above 22% while the NPV to capex ratio increased to 1.34, Santo Tomas is likely gaining a few spots in the ranking of multi-billion-pound copper assets in the world.

Key Financial Results and Costs

| Economics | Unit | LOM |

|---|---|---|

| NPV at 8% (pre-tax // post-tax) | US$M | 2,640.5 // 1,475.4 |

| IRR (pre-tax // post-tax) | % | 30.3 // 22.2 |

| Payback (pre-tax // post-tax) | Years | 2.9 // 3.8 |

| Revenue over LOM | US$M | 21,517 |

| Initial Capital | ||

| Mining Pre-Stripping (Capitalized OPEX) | US$M | 75.5 |

| Mining Capital Equipment (1) | US$M | 89.4 |

| Total Mining (1) | US$M | 164.9 |

| Processing | US$M | 938.7 |

| Total Initial Capital (1) | US$M | 1,103.6 |

| Sustaining Capital | ||

| Mining Equipment | US$M | 952.4 |

| Processing | US$M | 94.6 |

| Total Sustaining Capital | US$M | 1,047.0 |

| Expansion Capital – Processing (year 7) | US$M | 687.2 |

| Average LOM Operating Costs | ||

| Mining Cost per tonne mined (2) | US$ / t | 2.04 |

| Mining Cost per tonne milled (2) | US$ / t | 4.78 |

| Mining Equipment Leasing Cost per tonne milled | US$ / t | 0.06 |

| Processing Cost per tonne milled | US$ / t | 4.04 |

| G&A Cost per tonne milled | US$ / t | 0.65 |

| Total Operating Cost per tonne milled (2) | US$ / t | 9.53 |

The outcome of the updated PEA

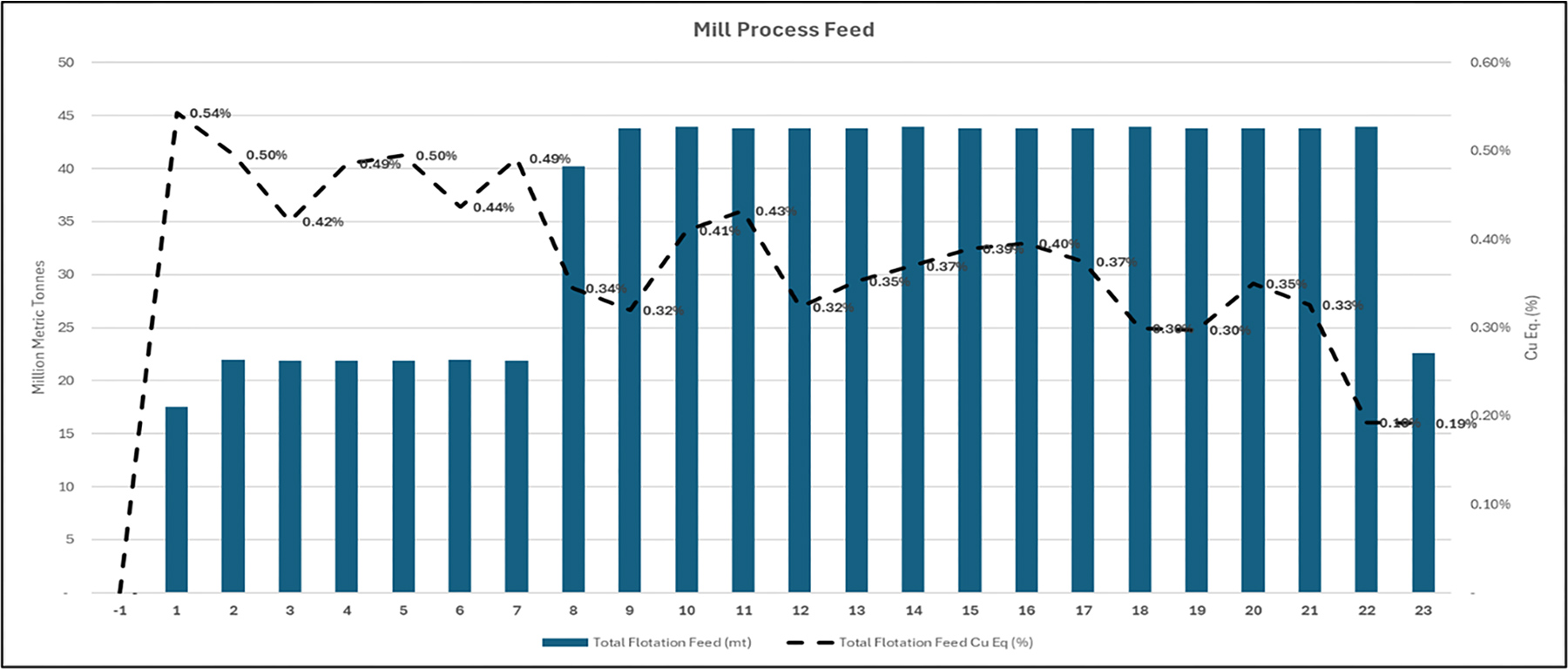

The updated PEA on the 85.5% owned Santo Tomas project is based on a mine life of almost 23 years, wherein a total of 825 million tonnes of rock will be mined and processed, at an average strip ratio of 1.38 tonnes of waste per tonne of rock.

This should result in an average output of just under 238 million pounds of copper-equivalent (208 million pounds of copper plus Mo, Au, Ag) per year, while the production will remain relatively limited in the first few years of the mine life with an average output of around 168 million pounds. In order to keep the initial capex relatively ‘low’ at $1.1B to make the project ‘financeable’, Oroco is deferring the expansion plan to year 7 (from Y8 on, the daily throughput will double from 60,000 tonnes per day to 120,000 tpd).

As per the capex breakdown, that expansion will cost just under US$700M and comes on top of the $1.05B in sustaining capex. While some investors may be worried about the $1.75B in sustaining capex and expansion capex, let’s not forget the mine is slated to produce approximately 4.75 billion pounds of copper (as well as and molybdenum gold and silver as by-products), generating almost $23B in gross revenue at current metal prices, and the sustaining + expansion capex represents approximately $0.37 per pound and that is a very reasonable number. So, while some people may interpret this as ‘cheating’, it simply is the best solution to avoid a $2B initial capex price tag and use the cash flows that will be generated in the first few years of the mine life to fund the expansion.

The total all-in sustaining cost per produced pound of copper is estimated to be $2.00, and this includes the expansion capex, so technically the ‘pure’ AISC excluding an expansion (and closure costs, for that matter) would be even lower).

Another interesting element here is the anticipated AISC in the first five years of the mine life. Although the daily throughput will be ‘just’ 60,000 tonnes per day which means the plant wouldn’t have the same operational efficiencies as it would have at 120,000 tpd later in the mine life, the higher grade in the first few years of the mine life definitely provides a nice boost. And that also explains why the payback period is less than 4 years while the IRR is just over 22%.

At a copper price of $4/pound, a molybdenum price of $15/pound and a gold and silver price of respectively $1900/oz and $24/oz, the after-tax NPV8% of Santo Tomas is approximately US$1.48B on a post-tax basis ($2.64B pre-tax), and Oroco’s 85.5% stake in Santo Tomas indicates the attributable portion of the NPV is around C$1.75B, or just over C$7/share. The after-tax IRR has also increased to a much healthier 22.2%.

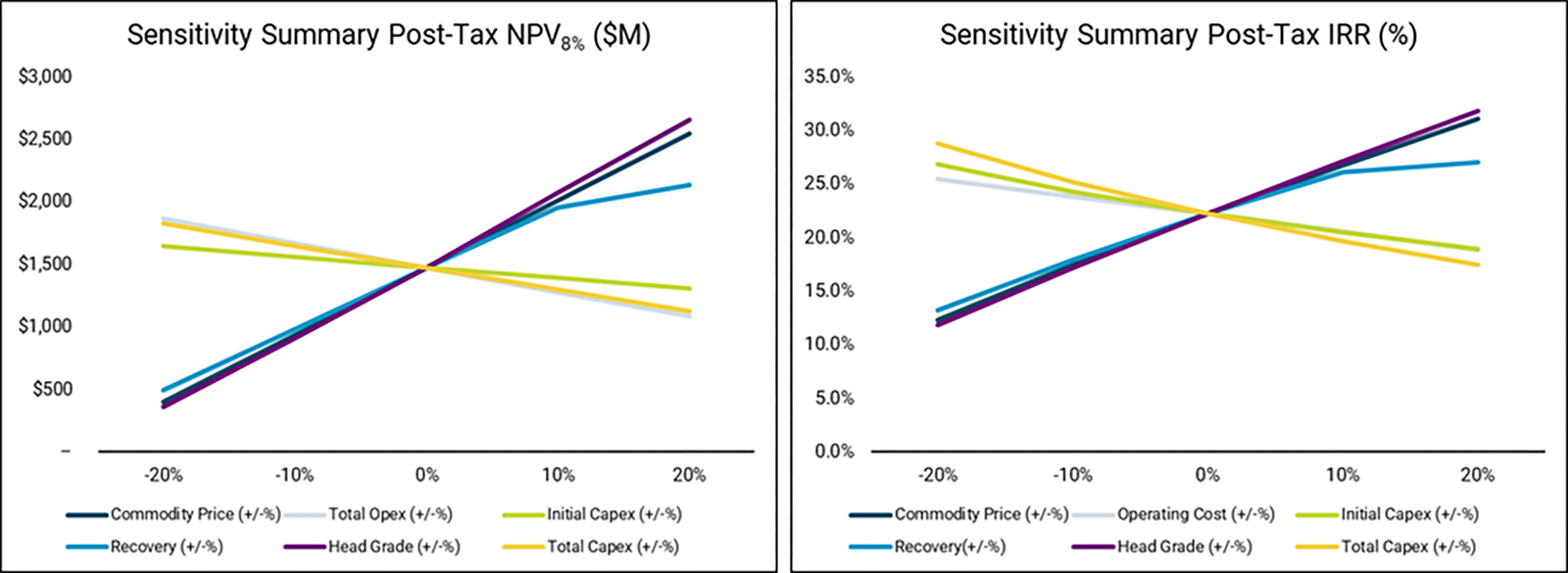

Looking at the sensitivity tables, a 10% increase in the copper price would boost the after-tax NPV8% to around $2B while the after-tax IRR should exceed 25%. At $4.50 copper, the NPV increases to US$2.15B on an after-tax basis while keeping the discount rate unchanged at 8%.

One of the wild cards at Santo Tomas is the precious metals credit. As per the updated PEA, the mine will produce almost 27 million ounces of silver and 300,000 ounces of gold. Not only does this mean a precious metals stream could provide a viable cash and equity infusion as part of a capex financing package, the base case prices in the PEA are relatively low. While $24 for silver appears to be fine, the $1900 gold price appears to be a tad low. Using $2400 for instance, would increase the LOM net revenue by approximately $150M. Using $28 silver would add another $100M for a combined impact of around $250M.

Granted, given the total pre-tax NPV8% of $2.64B and a LOM revenue of $21.5B, applying higher base case prices for the precious metals by-product credits may not move the needle by too much. But we see it as an additional potential bonus to the project.

Additionally, the PEA uses a base case price of $15 per pound for molybdenum although the price of that commodity has been trading steadily around $20 per pound for the past few months. Although the moly price can be pretty volatile and caution is certainly warranted, applying the current spot price to the PEA would add another $400M in pre-tax revenue. This would have a positive impact on both the NPV and the IRR as there are no additional operating expenses associated with this.

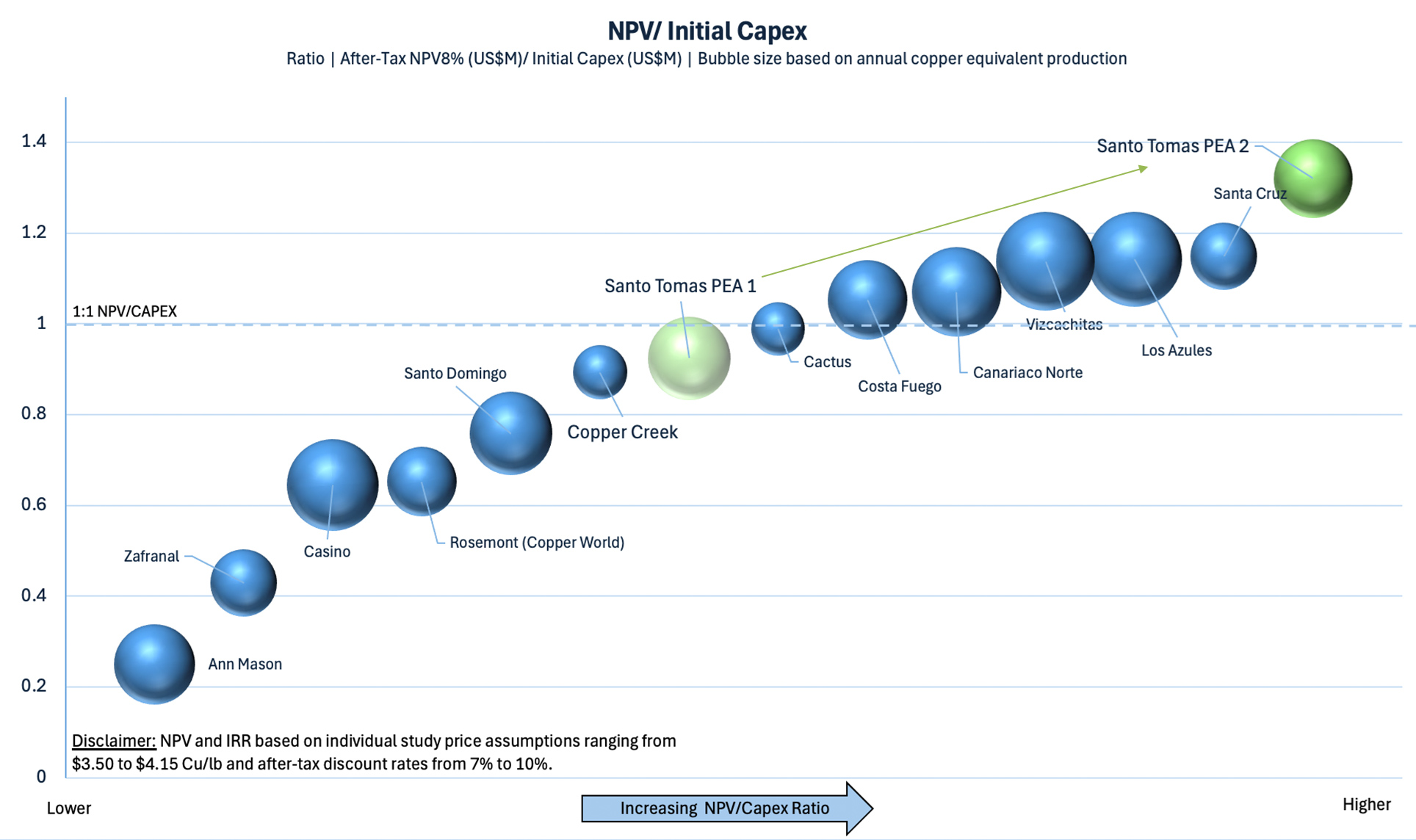

Another interesting metric is the after-tax NPV to capex ratio. Although it for sure isn’t the Holy Grail, it is a useful metric to determine ‘risk’. If a company – and this is a theoretical example – has a NPV of $500M after spending $2B on capex, you don’t need a big capex overrun to wipe out your entire theoretical NPV. And it simply isn’t appealing to spend $2B on a project that will net you $500M after all investments are recouped.

In Oroco’s case, the NPV to initial capex ratio comes in at 1.34 which – according to the image below, supplied by Oroco Resource Corp – puts it ahead of the pack. One caveat: the base case copper price used for the other projects below likely isn’t US$4/pound, but mitigating this may be that their CAPEX figures, if more than a year or two old, will not include a period of high cost inflation . Additionally, the newest PEA on the Cactus copper project highlighted a NPV versus initial capex ratio that is higher than the 1 shown in the image below so the comparison below should be taken with a grain of salt, and the ‘absolute’ number of 1.34 is what matters.

About the open pit mining ban proposal in Mexico

We are convinced one of the main reasons why Oroco’s share price is held back, is the continuous rumblings about banning open pit mining in Mexico. Although president-elect Sheinbaum will only take office in a little over one month from now, the incumbent president seems to be adamant to try to push the new law through parliament.

As per Morgan Stanley,

“The proposal indicates that no new concessions for open pit mining will be granted, except in specific cases of strategic importance for the country’s development, which should be approved by the President through the committee responsible for the new law. The proposal also mentions that contracts, concessions, permits and authorizations already granted before the approval of the proposed reform will be respected.”

We will have to wait for the dust to settle, but there is a case where the development of a copper asset could potentially be ‘of strategic importance’ to Mexico. Only time will tell, but we consider it quite likely that it is a major factor holding Oroco back. Any clarity on this subject matter would be welcome.

Conclusion

The economics in the updated PEA are definitely substantially better than the results that were released in the final quarter of last year. There still are some additional ‘enhancement opportunities’ to further improve the project, including approximately 250 million tonnes of mineralization included in the resource calculation but excluded from this mine plan. Additional resources could potentially be identified in the current pit by infill drilling in the area between the North and South and mineralization south of the current resource which has been already identified by Oroco’s prior drilling, not to mention mineralization north of the North Zone, where mineralization remains open and has been drill confirmed 1.5 km north at Brasiles. Although the impact on the NPV and IRR would likely be rather negligible, it could add more pounds of copper to the total output, thus making the asset more attractive for potential buyers.

While the first PEA didn’t clear all the hurdles, the second PEA is much better. With an after-tax IRR of 22.2%, the symbolic threshold of 20% has now been cleared with a considerable margin.

Now it’s up to Oroco’s team to continue to advance the project and make it as appealing as possible to a larger company that would be interested in acquiring an asset that could produce around 4.75 billion pounds of copper and in excess of 5 billion pounds on a copper-equivalent basis.

Disclosure: The author has a long position in Oroco Resource Corp. Oroco is a sponsor of the website. Please read our terms & conditions.