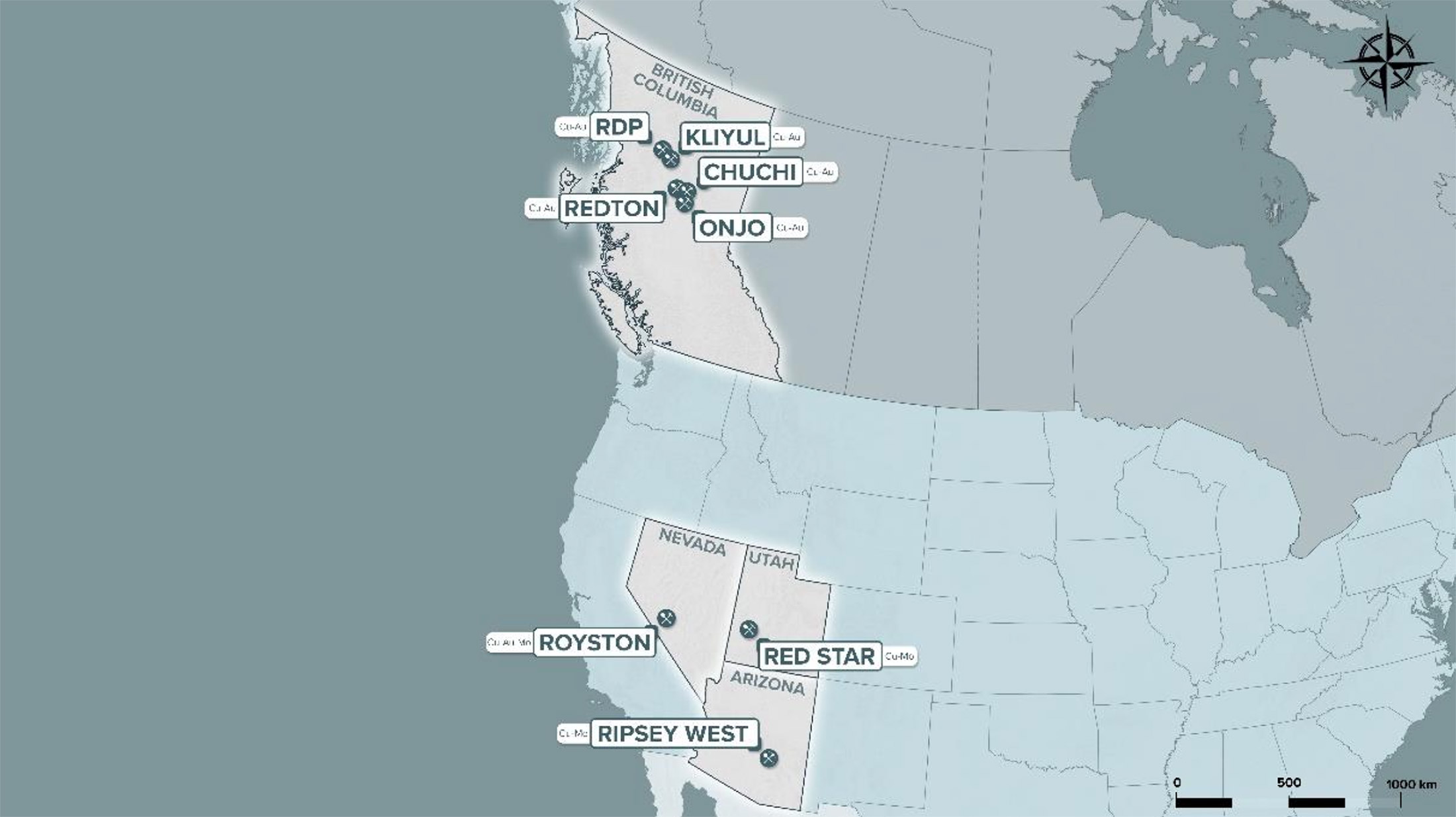

Pacific Ridge Exploration’s (PEX.V) share price has been sliding for the past year as the market gave a lukewarm response to the exploration results from its main copper projects in British Columbia. Although the Company was able to expand the mineralized footprint of the Kliyul Main Zone at the Kliyul copper-gold project and it did intersect copper mineralization in all the holes drilled at the Chuchi copper-gold project, the results simply weren’t good enough to excite the market.

On top of that, all Pacific Ridge’s copper projects are located in B.C. were it isn’t possible to explore year-round. And now that all the results from the 2024 exploration programs have been published, there likely won’t be any news flow for the next six months, which isn’t a good situation for any junior exploration company.

The company’s management was clearly aware of the issues that it was facing and announced last year that it was looking into acquiring new copper projects in the United States. Last week, Pacific Ridge announced it had entered into agreements with EMX Royalty Corp (EMX.V, EMX) to acquire four copper and gold projects in the U.S. We sat down with CEO Blaine Monaghan to discuss this transaction and how this may impact Pacific Ridge in 2025 and beyond.

The USA Deal

Last week you announced you entered into an agreement with EMX to acquire four copper and gold projects in the U.S. You had already previously disclosed your desire to acquire a U.S. copper project but acquiring four at the same time was a bit unexpected. Was this a ‘package deal’ and do you have freedom to drop projects that don’t meet your criteria?

We wanted a pipeline of new projects to explore and all of these projects met our criteria: discovery potential; road accessible; a year-round exploration season, and; the opportunity to acquire a 100-per-cent interest. On top of that, we were looking for projects located on BLM land in mining-friendly states. Although announced at the same time, it is not a package deal. There is a separate agreement for each project so we can drop a project while continuing to hold the others.

You surely must have a favorite project among the four that are part of the EMX deal. Which asset would be your preferred one and why?

I like them all for different reasons.

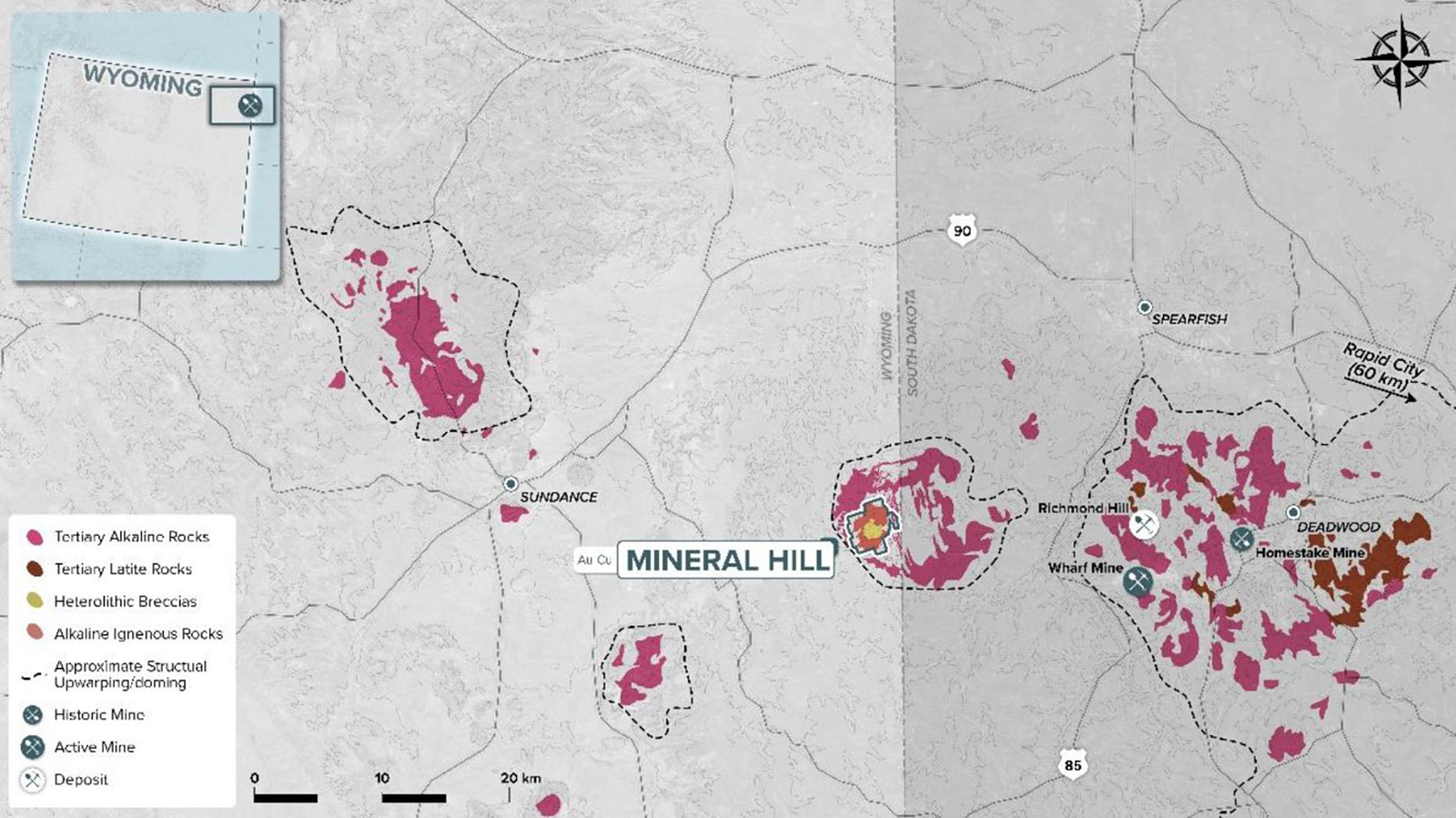

The Mineral Hill gold project in Wyoming is in a great neighborhood. ~25-km to the east, the historic Homestake gold mine produced more than 40 million ounces of gold . ~20-km to the east, Coeur Mining, Inc. is mining epithermal gold silver mineralization at the Wharf Mine and Dakota Gold Corp. is advancing their Maitland Gold and Richmond Gold Project. Mineral Hill will be the flagship project of the gold spinout company.

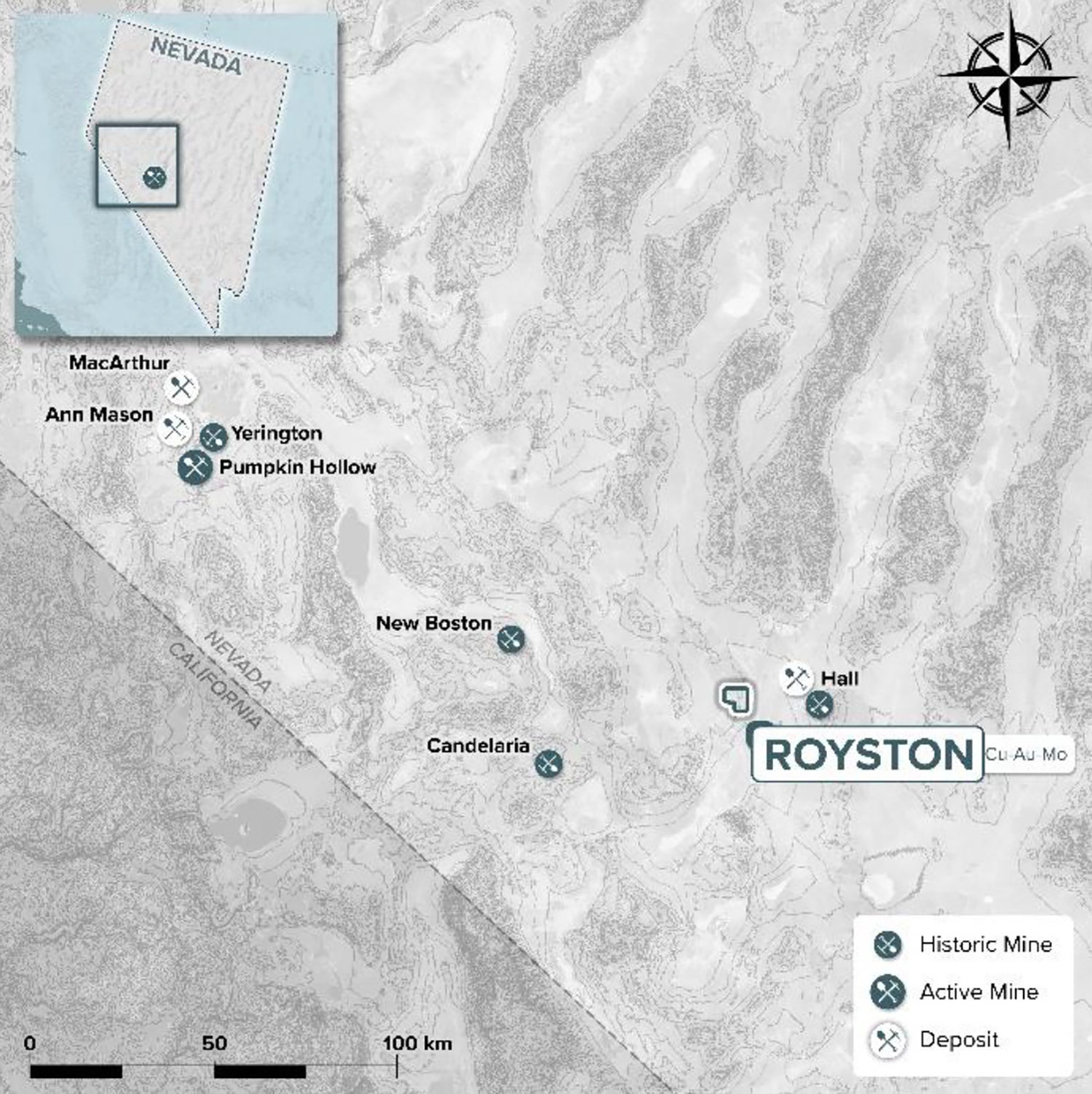

The Royston copper project in Nevada is permitted for drilling and ready to go – South32 (S32.AX) drilled five reconnaissance reverse circulation holes in 2023 and cased two of them. We want to open those two holes and drill them to depth. A quick, cheap test in 2025.

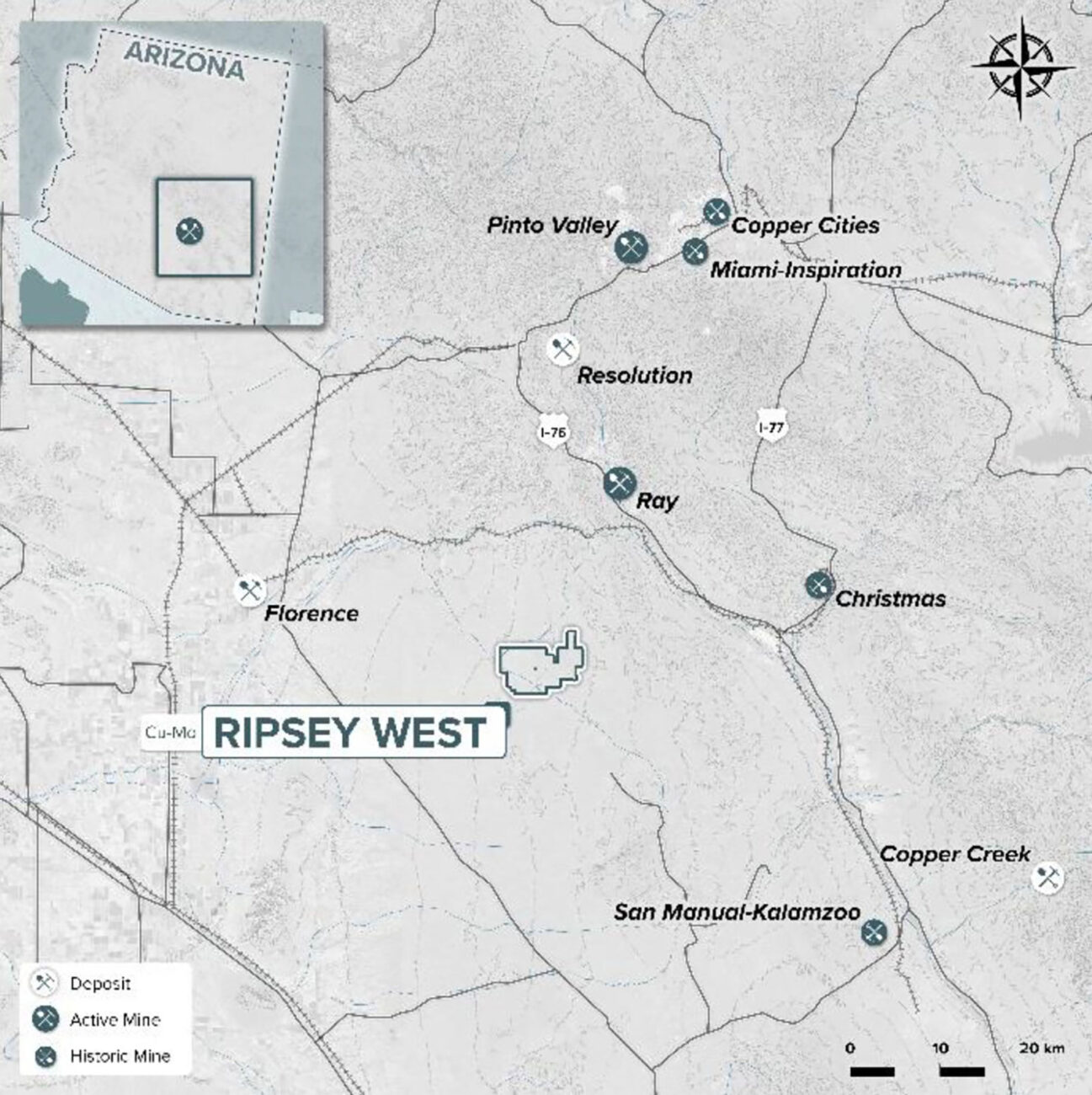

The Ripsey West copper project is located ~20 km south of the Ray Mine, one of the largest copper mines in the world, in Arizona. Another great neighborhood to look for more copper. A ~3.5 x 1.5 km target area has the potential for both hypogene mineralization and supergene enrichment.

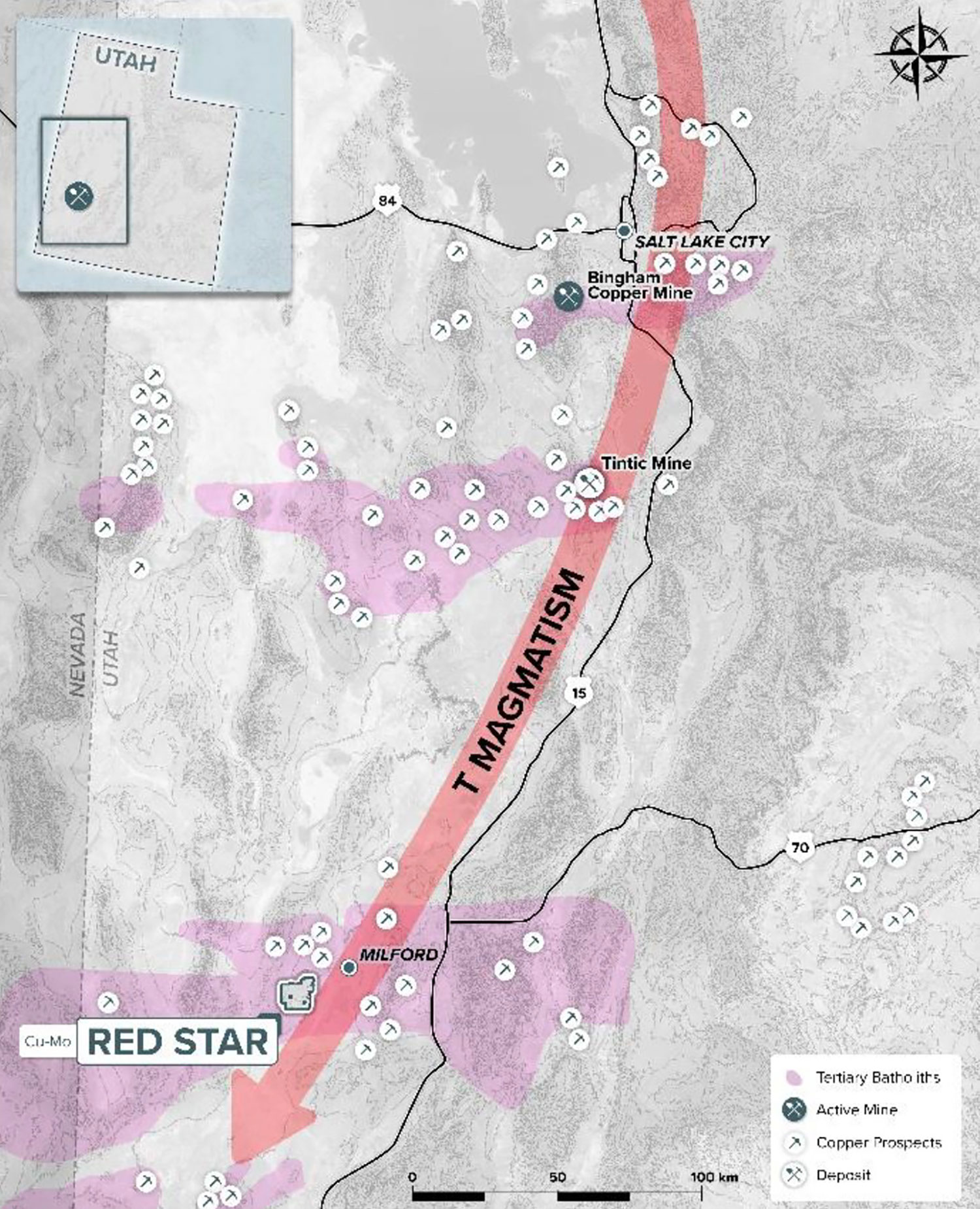

The Red Star copper project is a large grassroots project in Utah that’s never been drilled before. However, surface alteration and mineralization suggest the presence of a porphyry copper system beneath post-mineral cover. Further, it shares a similar regional geophysical signature with Bingham. Red Star is a high-risk, high-reward copper project that needs to be drilled.

All of us at Pacific Ridge are excited to get to work on these projects.

All assets will be subject to a 3% NSR which can be reduced to 2%. Is this the only NSR on the projects are are they encumbered by additional (non-EMX) royalties?

There are no additional royalties on the projects beyond the EMX royalties.

Surprisingly, all four projects are located in different jurisdictions so there appear to be little synergy benefits between the projects as your on-the-ground teams would still have to travel quite a distance. Is there a reason why the projects are so sparsed out?

We picked these projects because we felt that they were the best ones. It’s unlikely that we would be advancing all four of the projects at the same time so the distance between them shouldn’t be an issue.

Will you need to assemble a U.S.-based exploration team?

No, our VP Exploration, Danette Schwab, has considerable experience working in the U.S. Danette worked on the Long Canyon gold deposit with Fronteer Gold, as does our Chief Geologist, Paul Jago. Paul worked on the Sierrita and Bagdad copper-molybdenum mines in Arizona for Freeport McMoRan. If we need additional resources, we can always draw upon Bronco Creek Exploration (a subsidiary of EMX Royalty) for help. We optioned these projects from Bronco, and they are the ones that developed the models and the targets.

Other Assets

What are the plans for the B.C. assets this year? Will the projects be put on the backburner while you focus on the U.S. assets? Are you actively pursuing partnerships or joint ventures on the B.C. assets?

Since 2020, over C$18.0M has been spent on Kliyul and RDP. We are fortunate to own them 100% and that the claims are in good standing for over decade. This provides us with a lot of flexibility. We will look to partner with a senior mining company to advance these projects while we focus on our newly acquired U.S. assets.

Your recent press release mentioned that Pacific Ridge will move forward with a plan to spin off the Company’s Yukon gold projects and the newly acquired Mineral Hill gold project into a new gold-focused company. Is that the best way forward? After all, a new company will require a cash injection and an additional management team. Are other possibilities (a sale) still an option or is a spin-off the most likely scenario at this point?

Although there is a cost to spinning out the gold projects, I believe it is the best option for two reasons: costs savings and to unlock shareholder value. With respect to costs savings, we would share management, and other G&A expenses, between Pacific Ridge and Gold NewCo . The cost savings will exceed the costs of the spin out in the first year and result in lower G&A for both Pacific Ridge and Gold NewCo going forward. Further, the spin out will enable us to unlock shareholder value as the Yukon gold projects are not being advanced because the Company is focused on copper. Spinning out the Yukon gold projects, and the newly acquired Mineral Hill, will give shareholders exposure to a robust portfolio of North American gold projects.

Corporate

You also simultaneously announced a 1:10 share consolidation and that likely is a prelude to a raise given the majority of your C$1M working capital position at the end of Q3 consisted of prepaid expenses?

That is correct.

Will the lack of access to flow-through funding for US exploration be an issue to actually raise money for exploration programs given your current market capitalization of just C$3.5M?

With no expenditures required for our B.C. copper projects and only US$400K required to be spent on the four projects optioned from EMX during the first year, total, our 2025 capital needs are fairly modest. Combined with a dramatically reduced share count, I don’t foresee any problems raising the capital required.

Is there a standstill clause agreed with EMX whereby they can’t sell their shares within a certain period, and do they have to provide you notice so you could try to find a buyer instead of facing open-market stock sales?

There is no standstill. However, they will only receive 800K shares, or 200K shares per project on a post-consolidated basis, once the deal is approved, which isn’t a large amount. If we kept every project 3M shares, or 750K shares per project on a post-consolidated basis, would be due at the end of the fifth year. If EMX wanted to sell some or all of their shares, I’m sure that an orderly transaction could be arranged.

Conclusion

Pacific Ridge is changing its strategy and the addition of three copper porphyry projects to its asset base will allow the company to conduct year-round exploration. On top of that, we can expect the Company to make progress with its plans to spin off the gold projects.

Pacific Ridge is consolidating its shares on a 1:10 basis, which will result in 17.3M shares on a post-consolidated basis, and will be raising money soon so they can advance their newly acquired U.S. projects. Although market conditions remain extremely challenging, CEO Blaine Monaghan is confident that this new strategy, focusing on the new U.S. copper assets, finding senior mining partners to advance the B.C. copper assets, and spinning off the gold assets, will enable him to raise the funds required to conduct meaningful exploration this year. If Monaghan can pull this off, both Pacific Ridge and Gold Newco will be two companies to watch in 2025.

Disclosure: The author has a long position in Pacific Ridge Exploration. Pacific Ridge Exploration is a sponsor of the website. Please read our disclaimer.