Pacton Gold (PAC.V) used to be a ‘pure’ Pilbara play as it joined other Canadian and Australian companies in the nugget-focused Pilbara Gold Rush. With the recent acquisitions in the Red Lake Gold district however, Pacton now pursues a two-pronged approach. Pacton’s Red Lake land package neighbours Great Bear Resources (GBR.V) that discovered high-grade gold mineralization at Dixie and Pure Gold Mining (PGM.V) that is planning to develop a gold mine.

News should be forthcoming on a year-round basis now Pacton Gold has two epicenters of exploration.

Pacton Gold started out as a Pilbara story

Hot on the heels of the market hype surrounding Novo Resources (NVO.V), Pacton Gold offered speculators a ‘cheaper option’ to gain exposure to the discovery of gold nuggets and underlying gold structures in Western Australia’s Pilbara region.

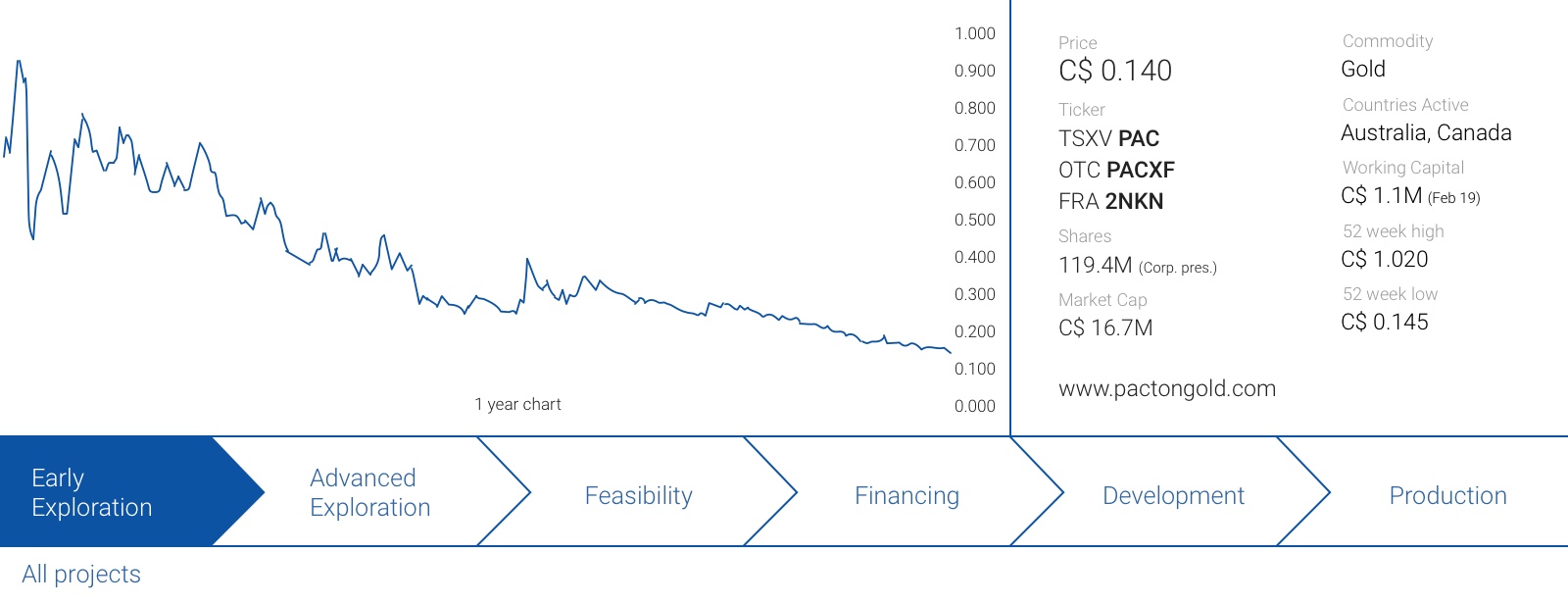

Although the company was originally already working on gold properties in Canada, Pacton Gold acquired a first piece of land in the Pilbara region in the first quarter of last year, followed by several additional deals to become one of the largest land owners in the region. This move had a substantial impact on Pacton’s market capitalization. As of the end of 2017, Pacton’s market capitalization was approximately C$15M, but this increased very rapidly throughout 2018 when the company was riding Novo’s coattails and just one year ago, in May 2018, Pacton reached a market cap of C$80M. Unfortunately, the company didn’t capitalize on its strong market performance and didn’t raise any money subsequent to the C$0.23 raise which closed in May 2018.

Hindsight is always 20/20 and although exploration companies should never refuse to take money, Pacton ended May 2018 with in excess of C$4M in working capital and C$9M worth of warrants (as part of the C$0.23 financing) with a strike price of C$0.35 that were deep in the money at that time (as well as 6.6M options at an average exercise price of C$0.25). So ‘raising money when your share price is high’ isn’t always a black-and-white story and it really depends on the circumstances.

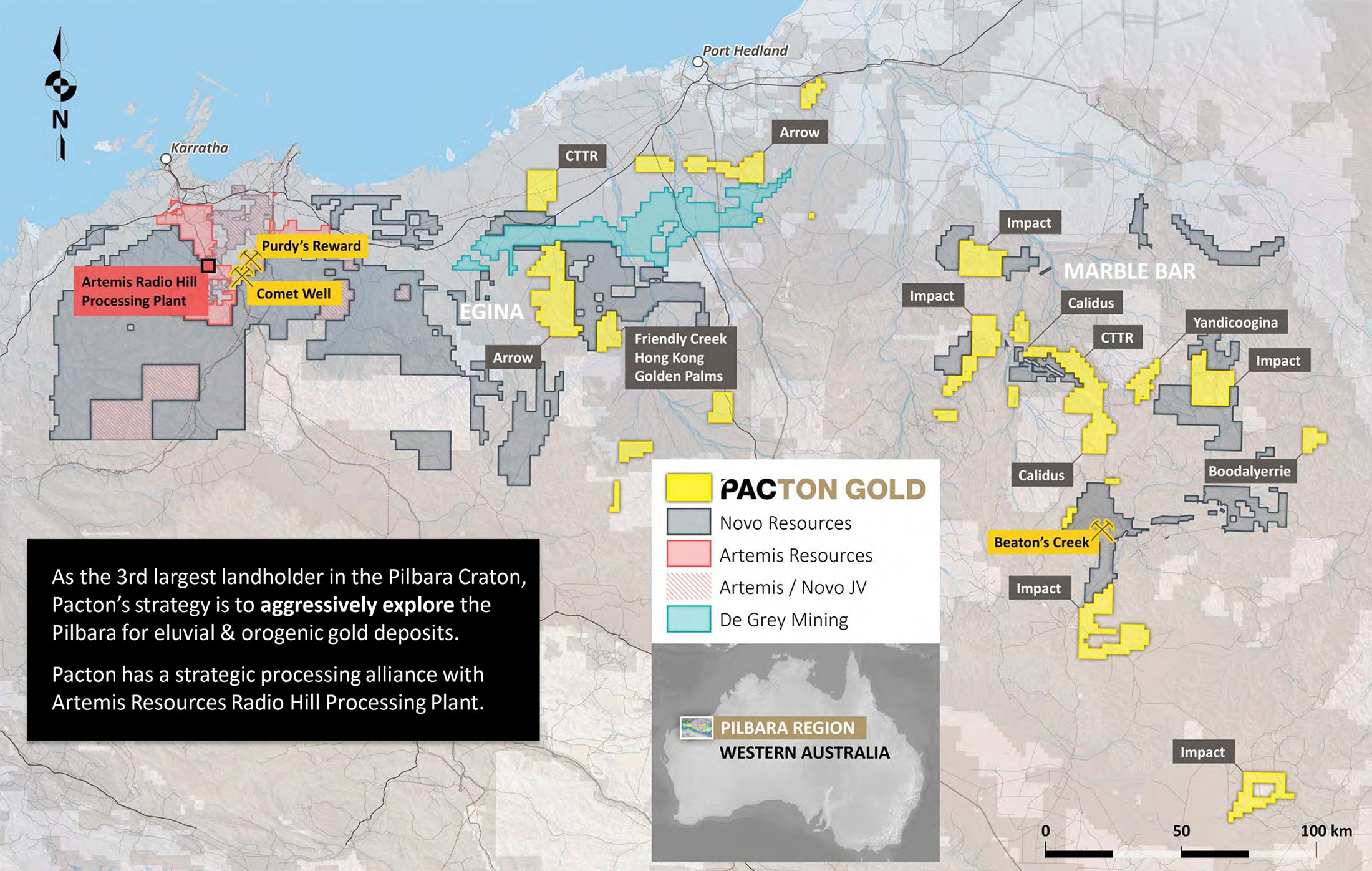

Pacton Gold was very busy in 2018 as it consolidated large land packages in the Pilbara region (which we discussed in-depth in 2018 ), and additional exploration updates confirmed the presence of gold nuggets.

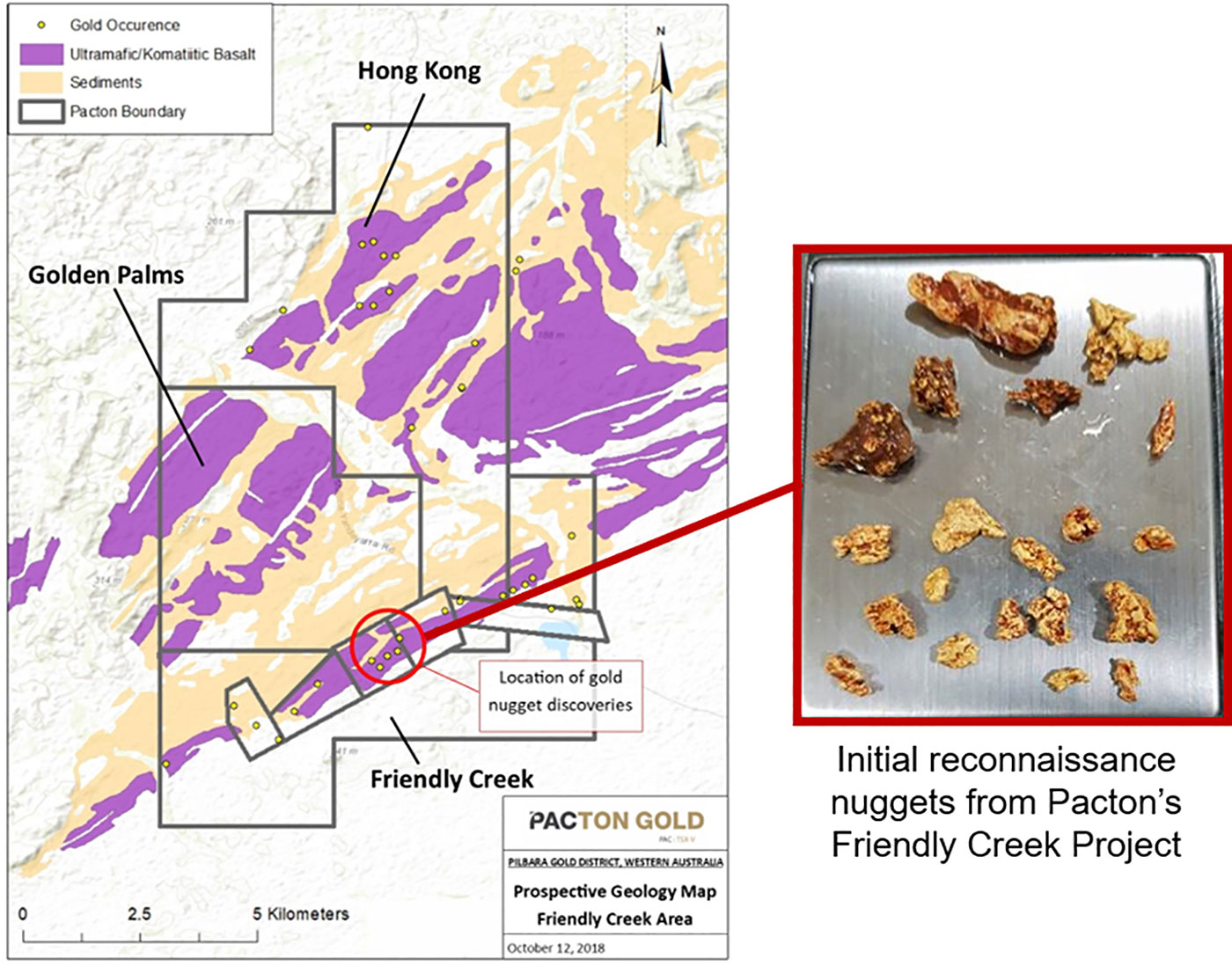

As a first step, Pacton’s prospectors discovered gold nuggets on six different locations on Pacton Gold’s Friendly Creek tenement. The nuggets were encountered in weathered material, and although the origin of the nuggets hasn’t been confirmed yet, the company’s initial interpretation is that these nuggets have not been transported and represent eluvial material that was disconnected from the underlying bedrock. Pacton said this interpretation matches the interpretation and assumptions of historical work on the Friendly Creek property, as well as previous interpretations of the Hong Kong tenement (which was the subject of an earn-in agreement in October and included a minimum exploration commitment).

And just a little bit later, Pacton’s interpretation gained even more credibility when prospectors also confirmed the discovery of gold nuggets on that Hong Kong tenement, which is located directly adjacent to the original Friendly Creek land package.

Since Hong Kong was acquired, Pacton Gold added just one additional property to its portfolio when it announced a binding LOI to acquire full ownership of the Tardarinna project which is surrounded by Novo Resources. There is evidence of historical eluvial gold workings on the claims, and this very likely attracted Pacton’s interest as this property remained underexplored despite the existence of quartz veins and surface samples which returned gold values up to 328 g/t.

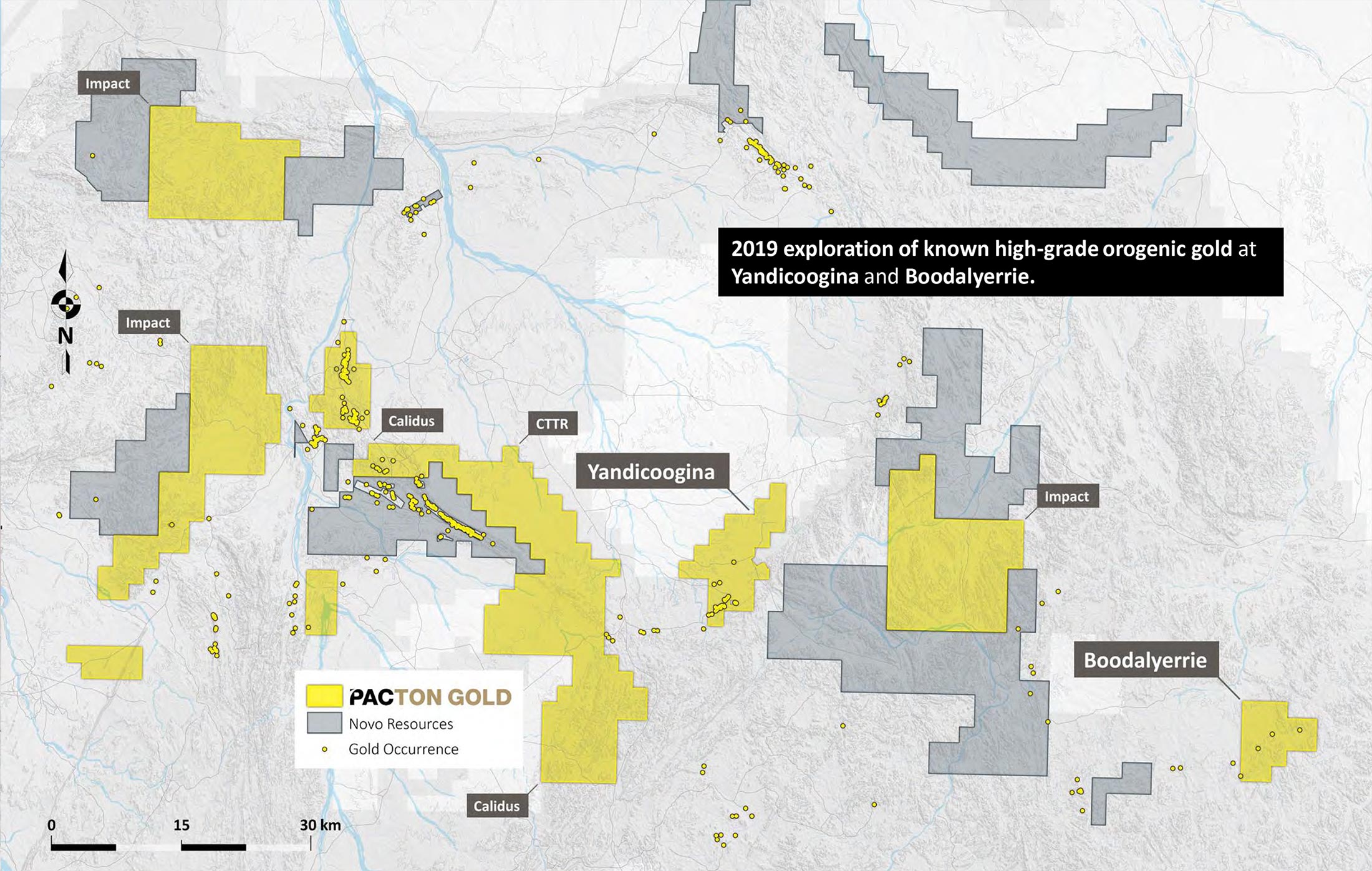

Back in March, Pacton Gold kicked off its 2019 exploration campaign at the Yandicoogina property (towards the east of the Pilbara region, and about 75 kilometers north of Novo Resources’ Beaton’s Creek project and about 50 kilometers southeast of Marble Bar). This exploration program was designed to follow up on historical sampling results which confirmed the presence of high-grade gold mineralization at surface with values of up to 200 g/t gold.

More work needs to be done before some of the targets could be drill-tested, and the current exploration program is meant to refine the potential drill targets and narrow it down to a few high-priority zones.

Pacton hasn’t released any exploration results yet, but we hope to see some initial results and assay results in the next few weeks.

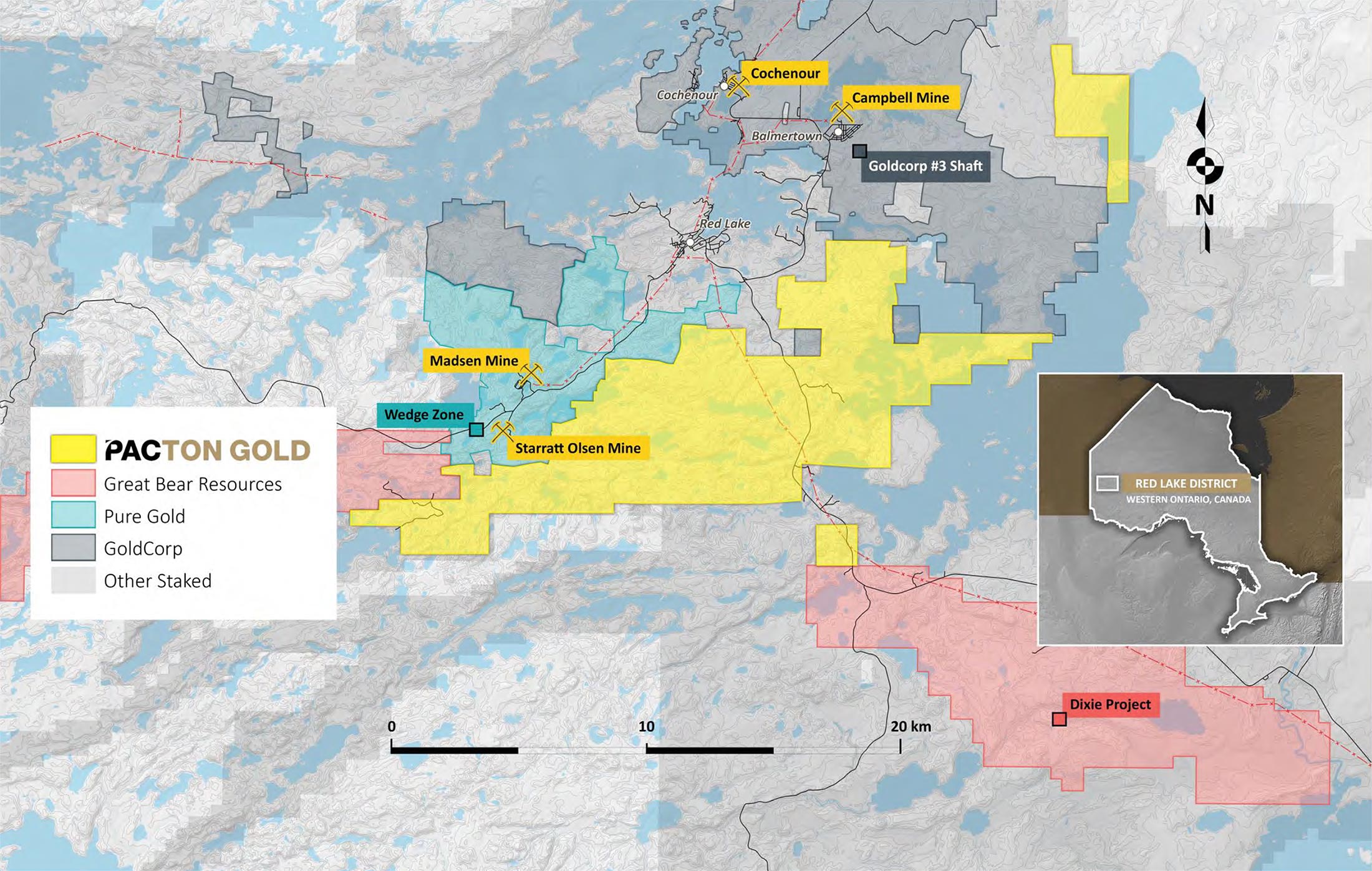

The company returned to its roots with an increased focus on the Red Lake gold camp

Although Pacton was one of the newest and smallest players in the Pilbara Gold Rush, the company was originally exploring for gold in Canada where it had a small land package in the Red Lake Gold camp. The majority of those tenements were scooped up before the discovery made by Great Bear Resources on its Dixie gold project, and Pacton was able to secure full ownership of its original claims for just a few hundred thousand dollars, and continued to expand its land position in 2019.

The company has recently picked up more land in the Red Lake district in Ontario, where it purchased an additional 1,760 hectares of land from Frontline Gold (FGC.V). The new tenements are directly adjacent to the company’s existing land package right in between Pure Gold Mining’s (PGM.TO) Madsen project and Great Bear Resources’ (GBR.V) Dixie project where it recently found ultra high-grade gold mineralization. Two additional acquisitions were completed in March and April, and Pacton Gold will be able to earn a 100% stake in both properties by making cash payments up to C$230,000 and issue 575,000 shares (on a combined basis and spread out over two years).

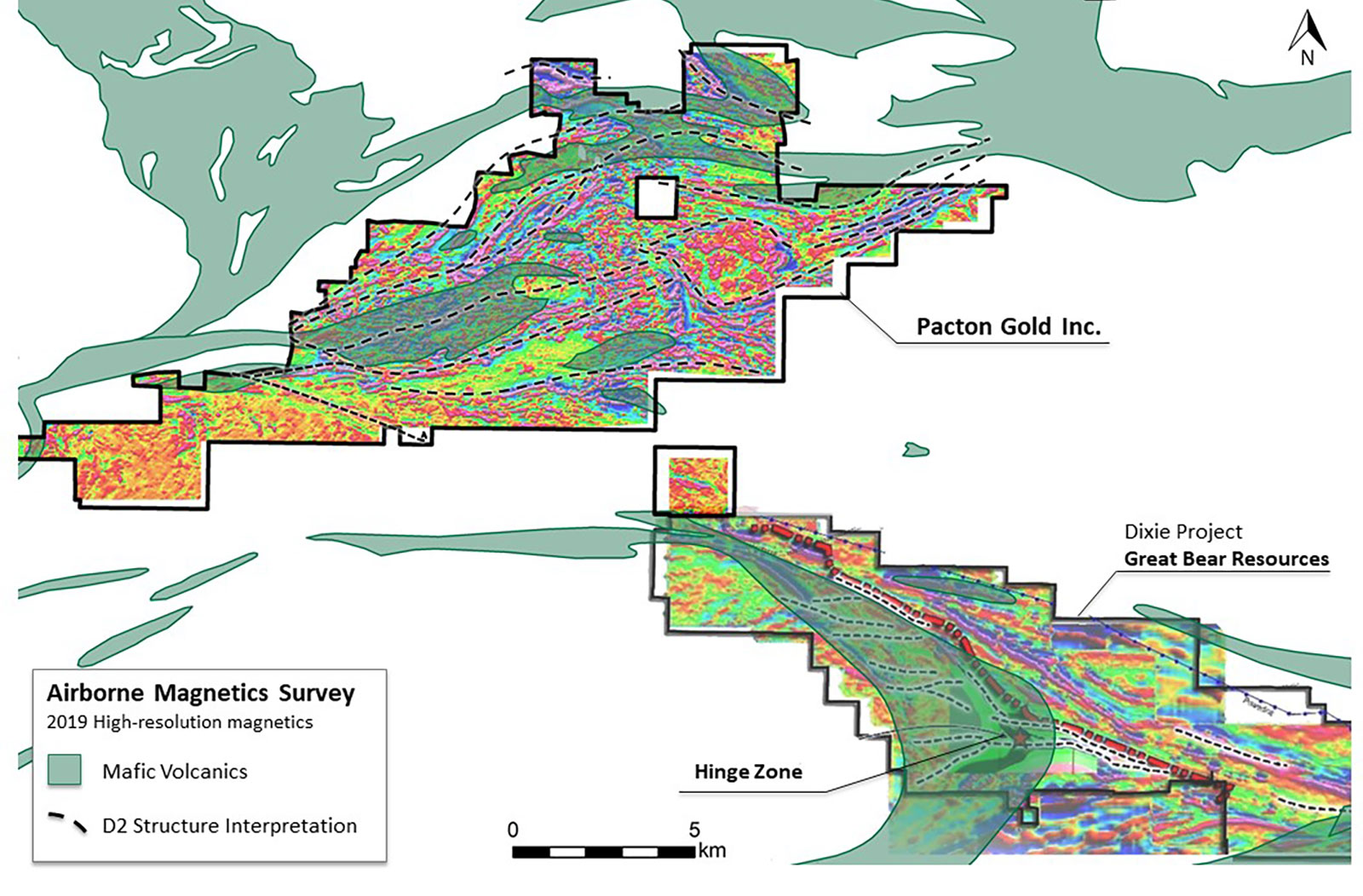

Since the exceptionally high-grade discoveries made by Great Bear Resources, the Red Lake camp enjoyed quite a bit of attention as well, as the new discoveries indicate there could be much more to be found in the immediate vicinity of the already prolific mines and projects in the district. And Pacton appears to be getting quite serious with its plans to advance its Red Lake assets in Ontario. Last month, the company completed almost 3,000 line kilometers as part of a high-resolution airborne magnetic survey (which was conducted immediately after acquiring the land from Frontline Gold). The results of the survey show linear structures which contain folding and faulting, and Pacton appears to be encouraged by these initial findings.

According to Pacton, ‘The central-west area of the property, mapped as basalt, demonstrates numerous east-west D2 fault structures that appear to be axial planar to repetitive folding. […]Historical trench and surface sample results from the Boyden Lake showings appear to lie along an eastwest D2 fault that bisects folding to the west, within or near mapped basalt units.’

Pacton Gold will now follow up on the results of the airborne survey with a summer field exploration program where the company will follow up on historical sampling and complete some trenches in anticipation of a drill program. The main task for the field geos will be to discover and map the D2 structures and mafic contacts, whereby the main focus will be on the mafic to felsic contacts on Pacton’s claims. It’s still early days for Pacton Gold at Red Lake, but the company anticipates to start drilling the highest priority drill targets towards the end of the summer.

How did Pacton spend its cash in FY 2018?

FY 2018 (which ended in November) was a transition year for Pacton Gold as it acquired more properties in Australia, and a large part of these acquisitions were covered by issuing new shares in Pacton Gold to vendors. That’s why the operating expenses increased to C$6.3M in FY 2018, but approximately C$2.65M consisted of share-based payments (mainly to the property vendors) while an additional C$1.4M was spent on consulting fees and C$1.23M on ‘shareholder communications’.

On a pure cash basis (so excluding the share-based payments), the company expensed approximately C$3.7M, while it also capitalized C$2.8M in exploration expenses on the tenements. We expect to see more funds to be spent on exploration this year, and a first glance at the Q1 results (the first quarter ended in February) seems to confirm this. Pacton expensed C$635,000 as operating costs (including C$36,000 in share-based payments), but also spent almost C$600,000 on capitalized exploration efforts.

With a working capital position of just over C$1.1M as of the end of February, there doesn’t appear to be an immediate need for Pacton to tap the equity markets. And perhaps good exploration results in either the Pilbara region or the Red Lake gold camp could allow Pacton to raise money at a higher valuation when it needs to top up its treasury.

Conclusion

Pacton Gold has evolved from being a ‘pure’ Pilbara play to an entity with two irons in the fire. In our first report we already mentioned Pacton would very likely mainly act as a ‘proxy’ on the Pilbara Gold Rush due to its market capitalization that was significantly lower than the first mover in the sector, Novo Resources. Pacton was able to pick up promising tenements and is now advancing towards the drill stage.

Meanwhile, it blew the dust off another project it had on the shelf and the renewed interest in the Red Lake gold district on the back of the discovery holes at the Dixie Gold Project by neighbour Great Bear Resources. We expect Pacton Gold to remain busy on both fronts, and hope to see the company publishing exploration updates at regular intervals.

Disclosure: Pacton Gold is a sponsor of this website. The author has a long position in Pacton Gold. Please read the disclaimer