Southern Silver Exploration (SSV.V) has tapped the equity markets at an excellent time in the summer of 2020 when it raised money to complete the acquisition of the majority interest in the Cerro Las Minitas flagship project. Subsequently, in the summer of 2021, the company raised an additional C$12M in a financing priced at C$0.50 and this helped the company to keep the exploration pace at Cerro Las Minitas quite consistent. This allowed Southern Silver to publish an updated resource estimate in the fourth quarter of last year, and the company met the expectations on all fronts.

Unfortunately, this did not result in an appreciation of the company’s share price despite it not being very difficult to argue Southern Silver has now reached the most advanced point it has ever been at.

Inflation is a hot topic, and in this report, we’ll once again run some back-of-the-envelope numbers to figure out the viability of the project. Southern Silver is gearing up to report its first-ever economic study on the project as it still aims to publish a Preliminary Economic Assessment by this summer.

The recent resource update is another step forward for the project

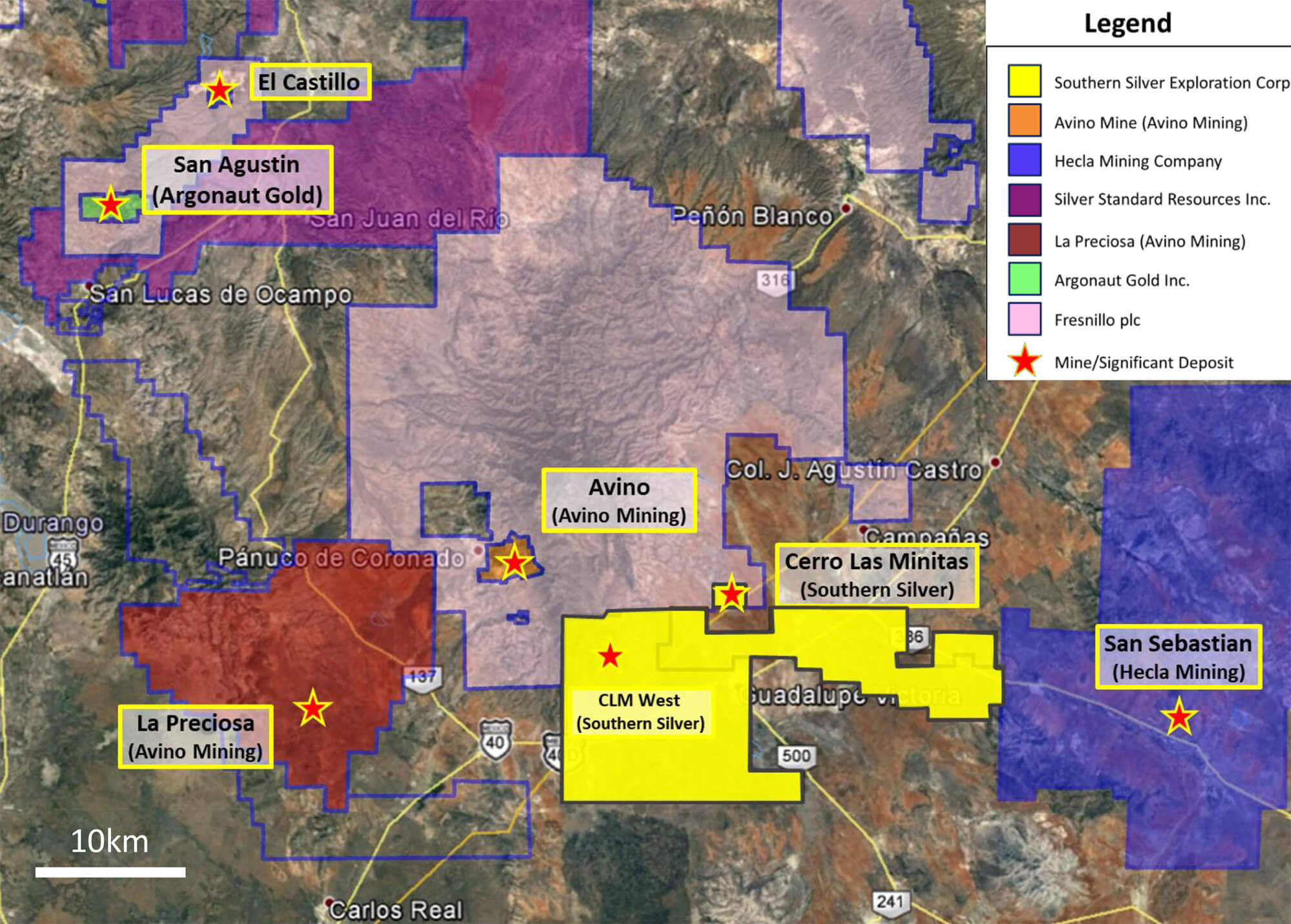

The Cerro Las Minitas project (here after ‘CLM’ for simplicity sake) is Southern Silver’s flagship project. The 34,450 hectare property is located just 70 kilometers to northeast of the city of Durango, in Mexico’s Durango state.

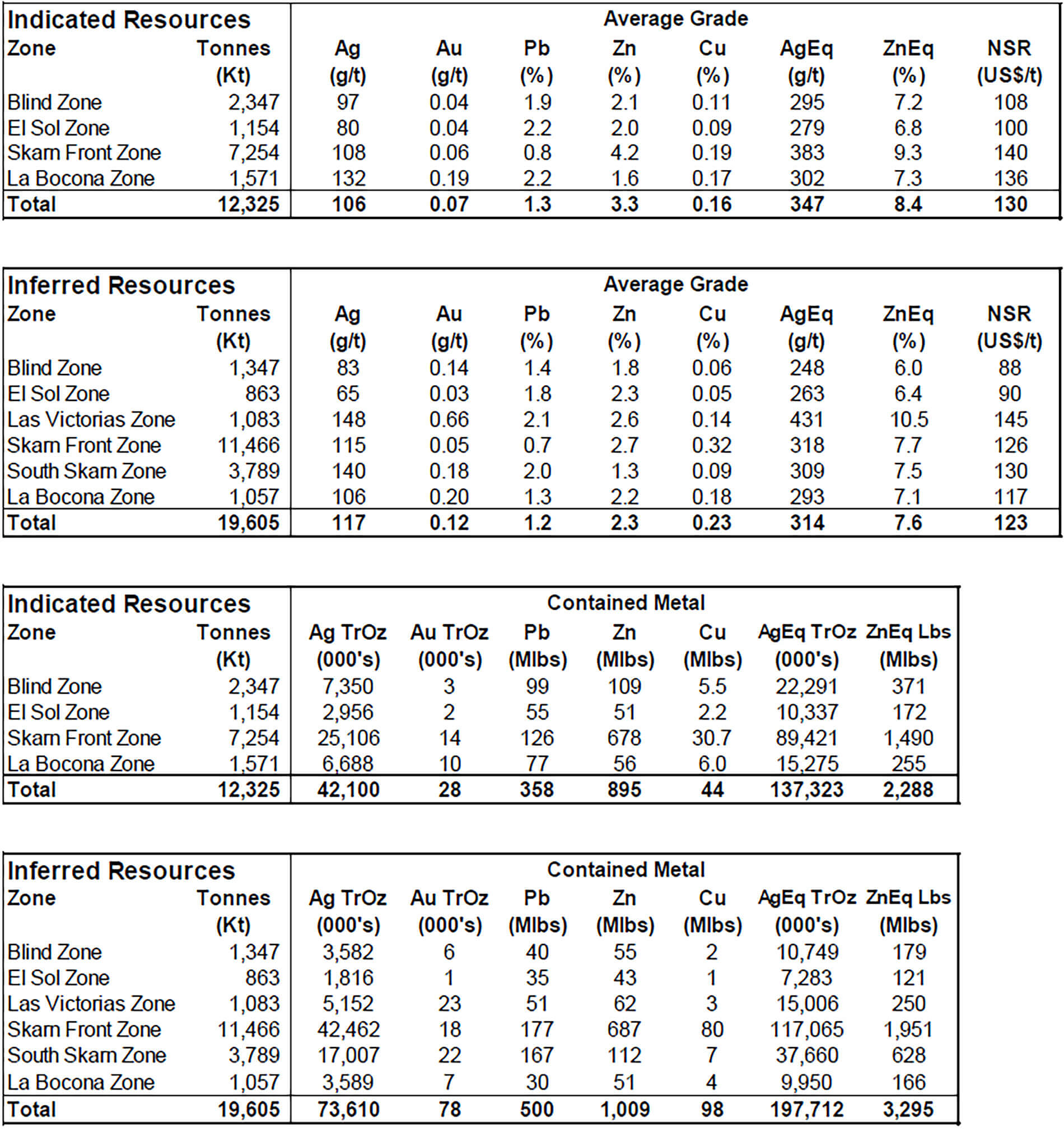

Southern Silver’s exploration team has an excellent track record when it comes to developing potential exploration targets. The past few resource updates have always come in above the expectations, and the recent update has once again increased the total resource on the project.

The total indicated resource came in at 137 million ounces silver-equivalent, consisting of 42 million ounces of silver, 358 million pounds of lead and 895 million pounds of zinc while there are some negligible amounts of gold (28,000 ounces) and copper (44 million pounds). The inferred resource now contains a total of 198 million ounces silver-equivalent including just under 74 million ounces of silver, 500 million pounds of lead and 1 billion pounds of zinc. There’s again some gold and copper (78,000 ounces and 98 million pounds respectively) but those two metals are just minor by-product credits.

As the project will evidently be developed as an underground mine, the average grade of the resource is important as well and in the next section of this report we will try to build an economic scenario using the currently known recovery rates and anticipated mining and processing costs.

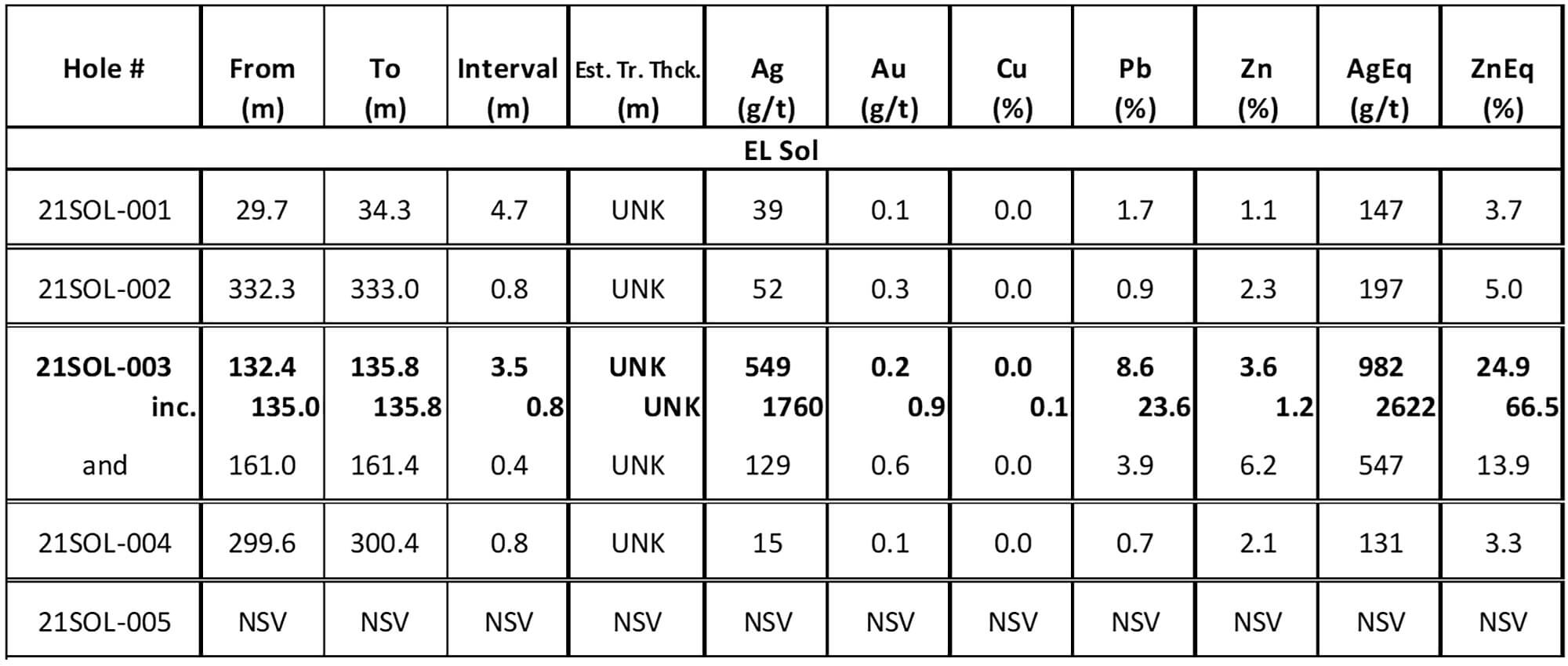

And although Cerro Las Minitas already contains in excess of 300 million ounces silver-equivalent let it be clear Southern Silver hasn’t reached the limits of the mineralization just yet. A little while ago, it acquired the El Sol concession, which is located directly northeast of and adjacent to the original Cerro Las Minitas claims. In January, the company reported the assay results of the first five holes ever drilled on that are.

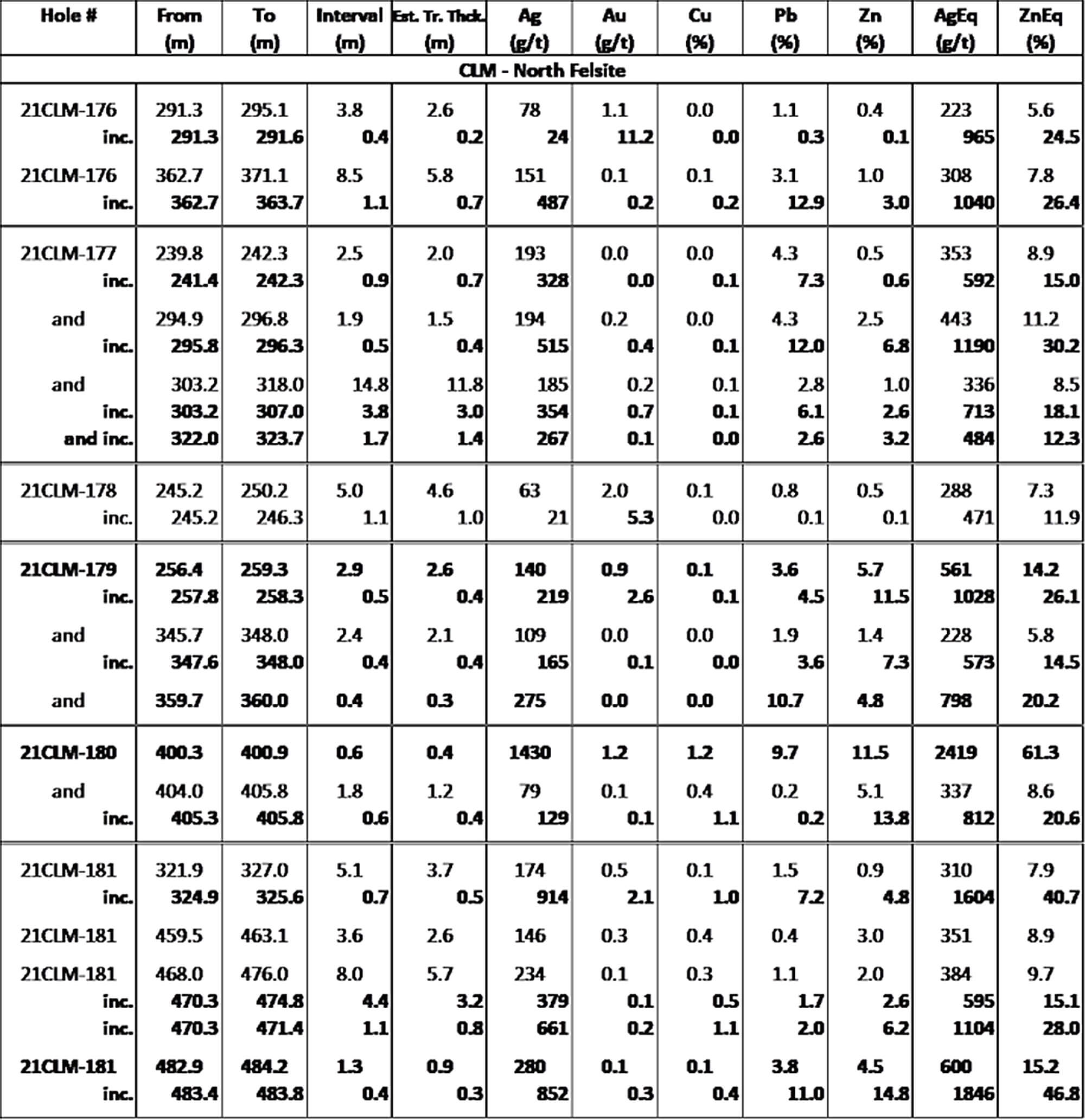

As you can see in the table above, hole 3 encountered 3.5 meters of 982 g/t silver-equivalent (including 549 g/t silver) with a higher grade interval of 0.8 meters containing 2,622 g/t silver equivalent. The main mineralized interval starts at a depth of just over 132 meters down hole. Keep in mind that the reported interval likely won’t be the true thickness. The true thickness could not be established yet as the company simply doesn’t have enough data to run the numbers on that.

Southern Silver decided to direct a drill rig back to the El Sol concession (before that rig will go back to the core area of Cerro Las Minitas to drill-test the North Felsite target) to complete an additional three holes. Two holes will be drilled to test the mineralization down dip of hole 3 and the third hole will be drilled along strike from one of the most northwestern holes of Blind-El Sol to fill the gap between Blind-El Sol and the new El Sol discovery.

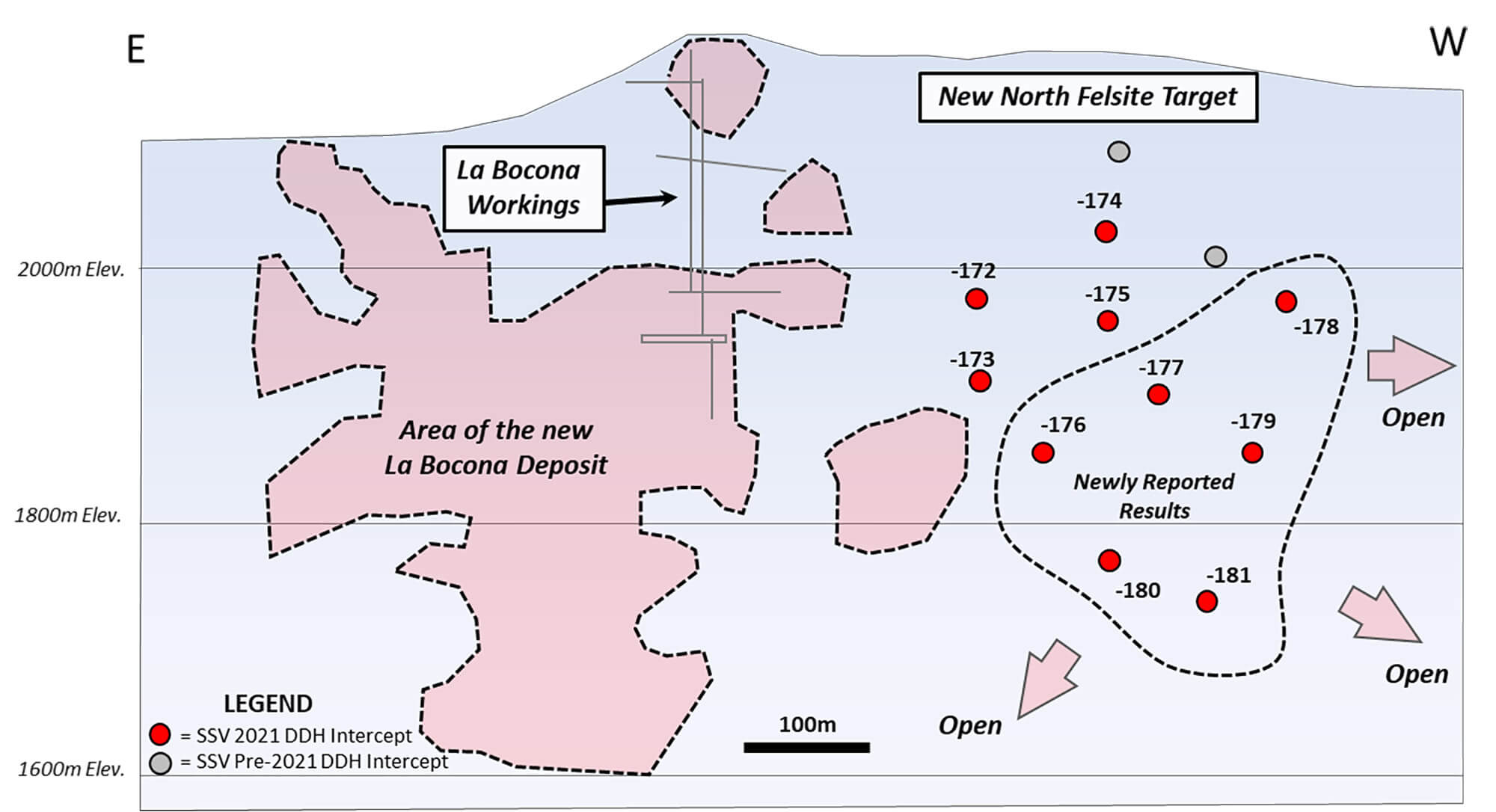

Additionally, an exploration update from the new North Felsite Zone, located about 400 meters to the northwest of La Bocona and Mina Pina area. As you can see on the image below, holes 176-181 were drilled in a completely new area.

And although this is an entirely new target, the assay results didn’t disappoint at all as all five holes intersected mineralization. This means the mineralized area remains open in all directions and we may for sure expect the company to drill more holes as increasing the drill density could be sufficient to incorporate this new zone in a future resource update as well. The rule of thumb is clear: every million tonnes at 310 g/t silver-equivalent added to the resource will add 10 million ounces of silver-equivalent to an existing resource. And then it will be up to the mine planners to actually incorporate these new zones into a viable mine plan.

What about inflation? Updating our assumptions for the economics of Cerro Las Minitas

The company will publish a preliminary economic assessment later this year, but we already wanted to have a first pass using the current publicly available information from the metallurgical test work and the resource estimate while adding capex and opex assumptions based on similar projects in Mexico.

Keep in mind these calculations should be seen as a theoretical exercise, a back-of-the-envelope calculation and it in no way represents an official guidance or expectation from the company. And in the current inflationary environment, we could be off by a double digit percentage. The sole purpose of these calculations is to have a rough idea of what we can expect.

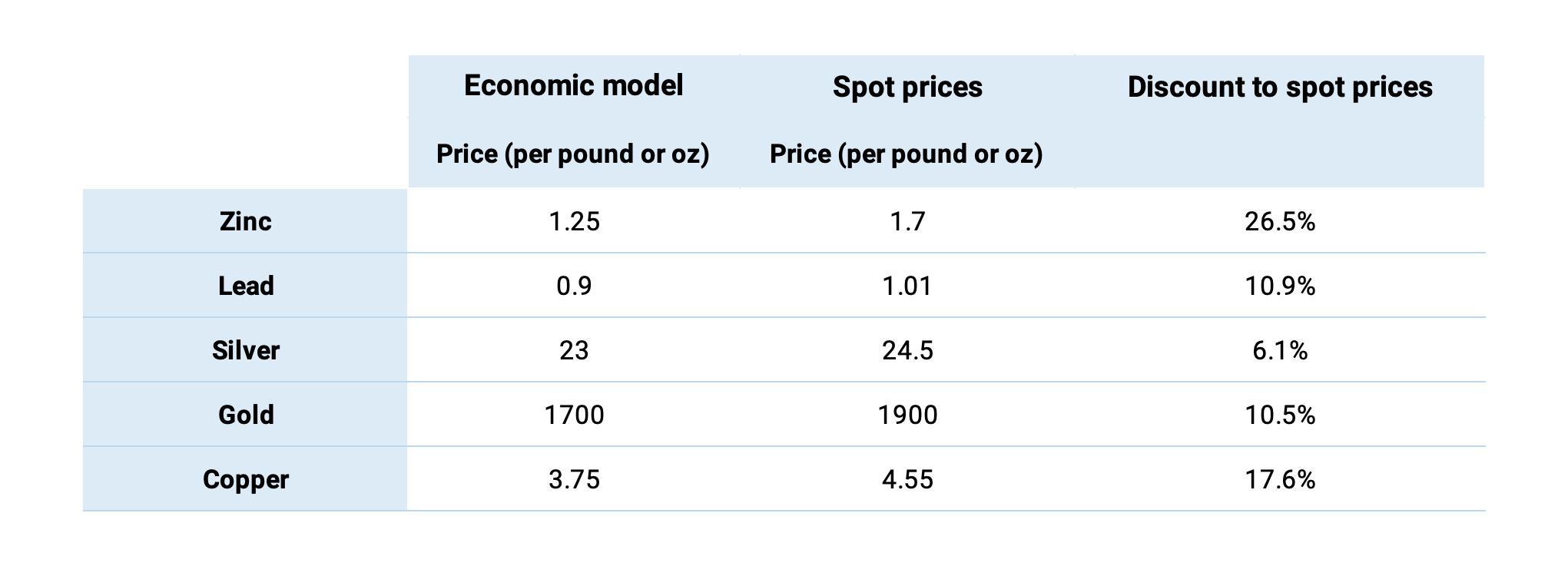

First of all, we are establishing the commodity prices we will use in our model.

The zinc price is very high these days and this once gain presents zinc as the dominant commodity in the production mix using spot prices. We are using slightly more conservative commodity prices

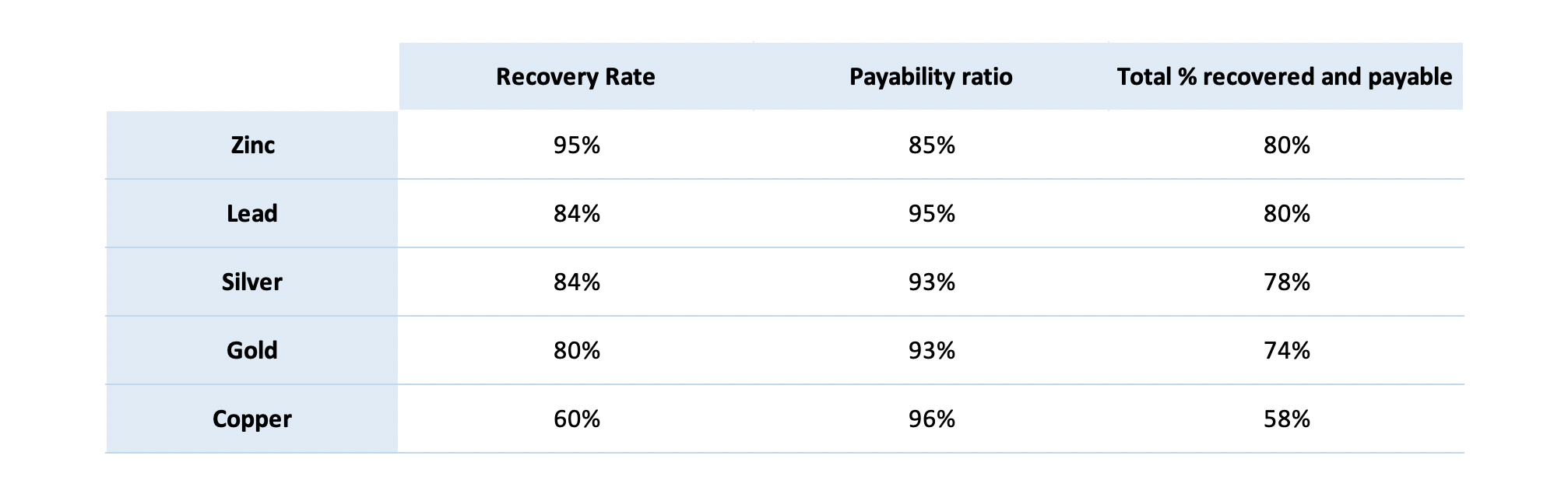

The anticipated recovery rates have not changed, and we will use the respective recovery rates as indicated below.

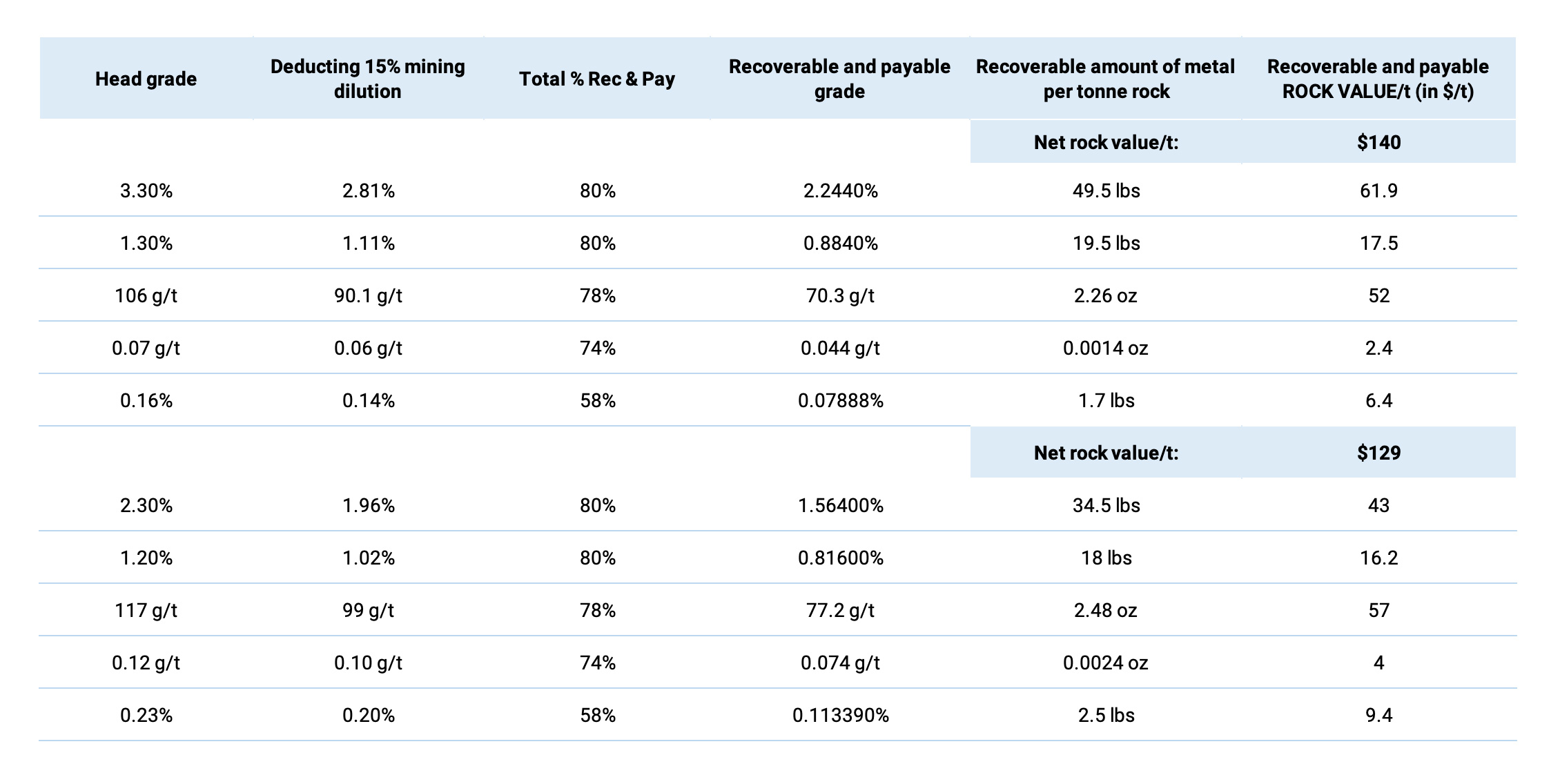

This now allows us to calculate a NSR value per tonne of rock, taking the respective recovery rates and payability percentages into account. In the table below, we have reduced the average head grade by 15% to account for mining dilution. This differs slightly from our previous approach where we accounted for the mining dilution by increasing the operating costs per tonne. Diluting the head grade of the rock that actually gets fed to the mill seems to be a more fair approach.

Based on the price deck we use, the net recoverable and payable rock value per tonne is $140/t in the indicated resource category and $129/t in the inferred resource category. In the indicated category, zinc is the main metal (even at $1.25 zinc) but it’s the opposite scenario in the inferred resource category where silver becomes the dominant commodity.

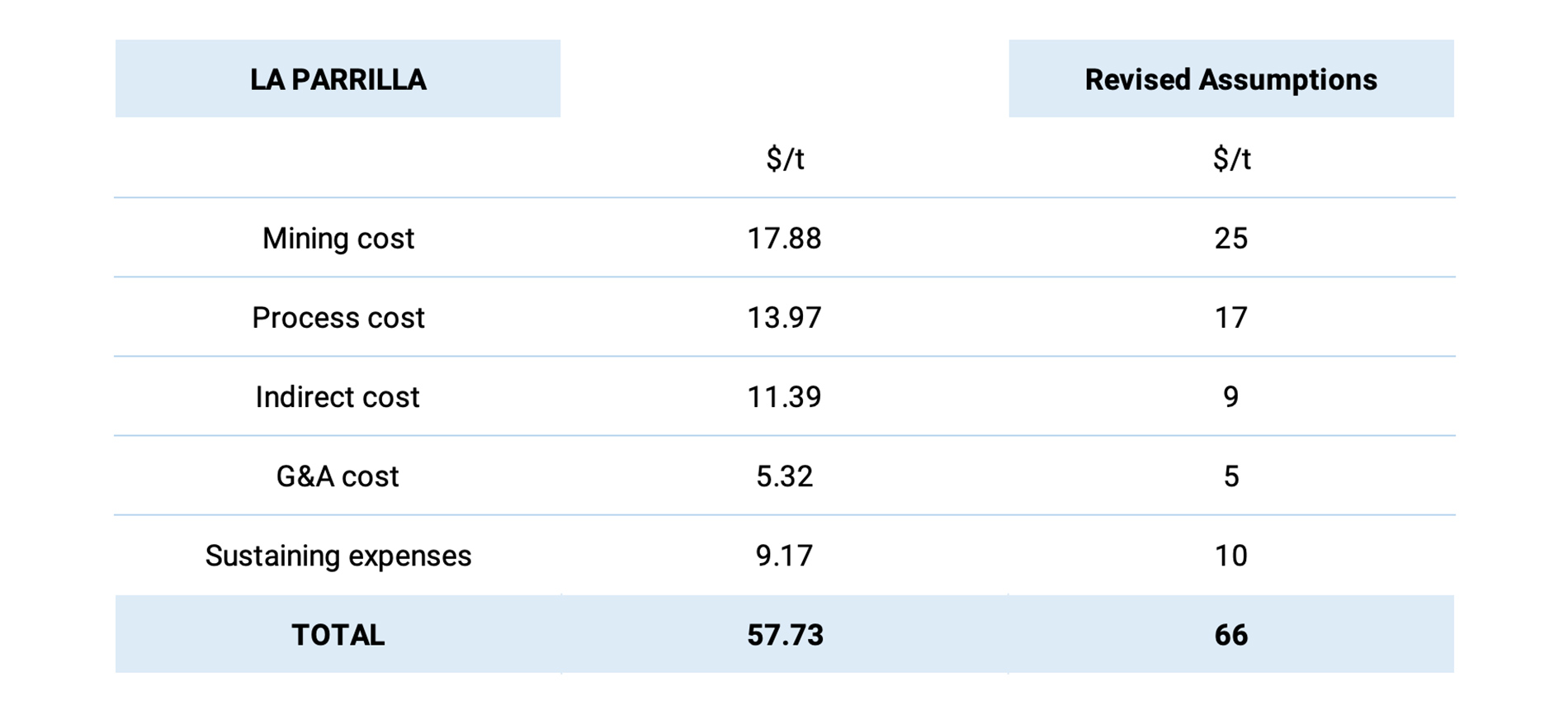

Now we have established the anticipated net smelter revenue per tonne (important: there are no royalties on the Cerro Las Minitas project, so ‘what you see is what you get’) and we will continue to use the data used by First Majestic Silver (FR.TO, AG) in its economic studies on the La Parrilla mine in Mexico. We also looked at the recent pre-feasibility study of Integra Resources (ITR.V) which included a processing cost of $9.45-15.45/t which is substantially lower than for instance the recent numbers used by fellow Mexican companies Vizsla Silver and Silvercrest Metals and that difference could be explained by the fact that Southern Silver’s economic model will contain more economies of scale as it is targeting a 4-4,500 tpd operation versus the 1,250 tonnes per day used in for instance Silvercrest’s model. In our assumptions we are using a processing cost of $17/t (but the upcoming PEA will obviously provide more details here).

We will use a total opex of $66/t which is in line with the cut-off calculation used by the company for its resource model. Keep in mind the infrastructure at and around Cerro Las Minitas is excellent and this should help to keep the costs down.

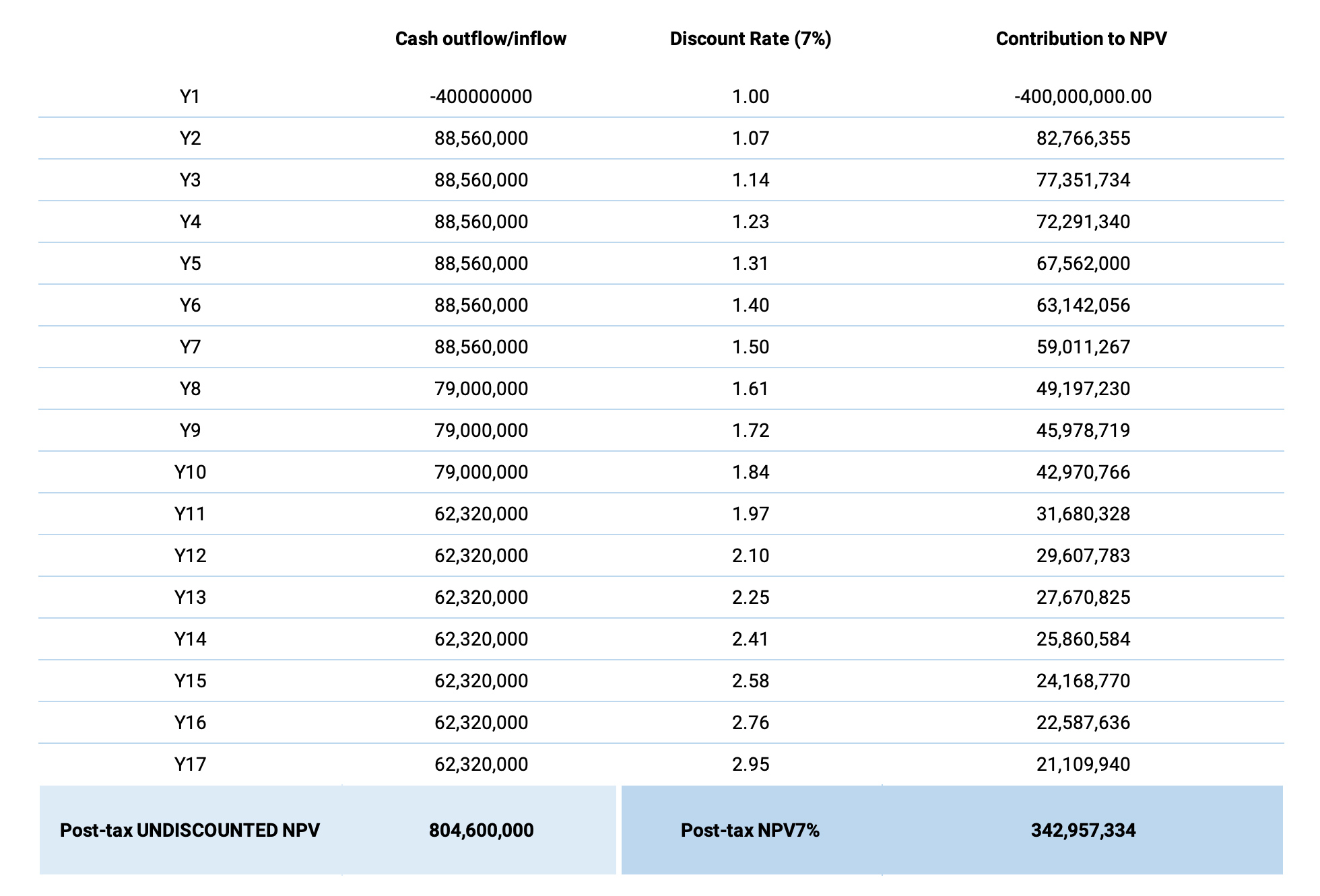

The anticipated capex is a more difficult one to consider given the current inflationary environment. We already had a rather high capex of US$380M in our previous calculations and this still seems to be a fair number. Integra Resources is budgeting US$190M for a 6,000 tpd mill in Iadho, which includes almost US$60M in tailings facilities. Of course there’s equipment and initial groundworks to be considered as well. We are now using a US$400M initial capex for a 4,500 tpd operation and feel quite comfortable with that number. Of course this is just an educated guess at this point and it will be interesting to see what Southern Silver ends up with.

At 4,500 tonnes per day, Southern Silver will be processing just over 1.6 million tonnes per year. We will assume the indicated resources will be processed in the first 7 years of the mine life, followed by 11? years using the inferred resources. Using this number, about 25 million tonnes of the 32 million tonnes would end up in the mine plan. Of course this is a simplification of how a mine plan works and there will for sure be variations and differences in the eventual mine plan. But this is just a back-of-the-envelope calculation to get a rough idea of the economics. So just take everything with a pinch of salt.

Another assumption is to use a 10-year depreciation schedule for the initial capex and will use an annual depreciation of $40M, and using a total tax pressure of 40% (corporate tax + the specific mining taxes). This means that the total average tax per processed tonne of rock in the first 7 years will be 0.40 X [(1.64Mt X $74/t) – $40M] = $32.5M, or $20 per processed tonne.

For years 8-10, the numbers are: 0.40 X [1.64Mt X$63/t) – $40M]= $25M, or $15/t for the tax pressure.

For years 11-17 there will be no depreciation allowance and the tax pressure will be 0.4 X 63/t = $25/t.

This results in an after-tax NPV7% of US$343M.

Of course this is just a back of the envelope calculation and we will have to wait for Southern Silver to publish its Preliminary Economic Assessment to see how far off we are.

And the NPV can change fast. If the operating cost per tonne comes in $2 lower, the undiscounted NPV will increase by over $50M. A $50M reduction in the capex will have the same impact while extending the mine life by a year will add $20M. And applying a 5% discount rate compared to the 7% we used would also add almost US$100M to the after-tax NPV.

Drilling Oro and acquiring another project

Although most of the attention (deservedly) goes to the flagship Cerro Las Minitas project, we shouldn’t forget Southern Silver is currently working on a 4,000 meter diamond drill program on its Oro project in New Mexico.

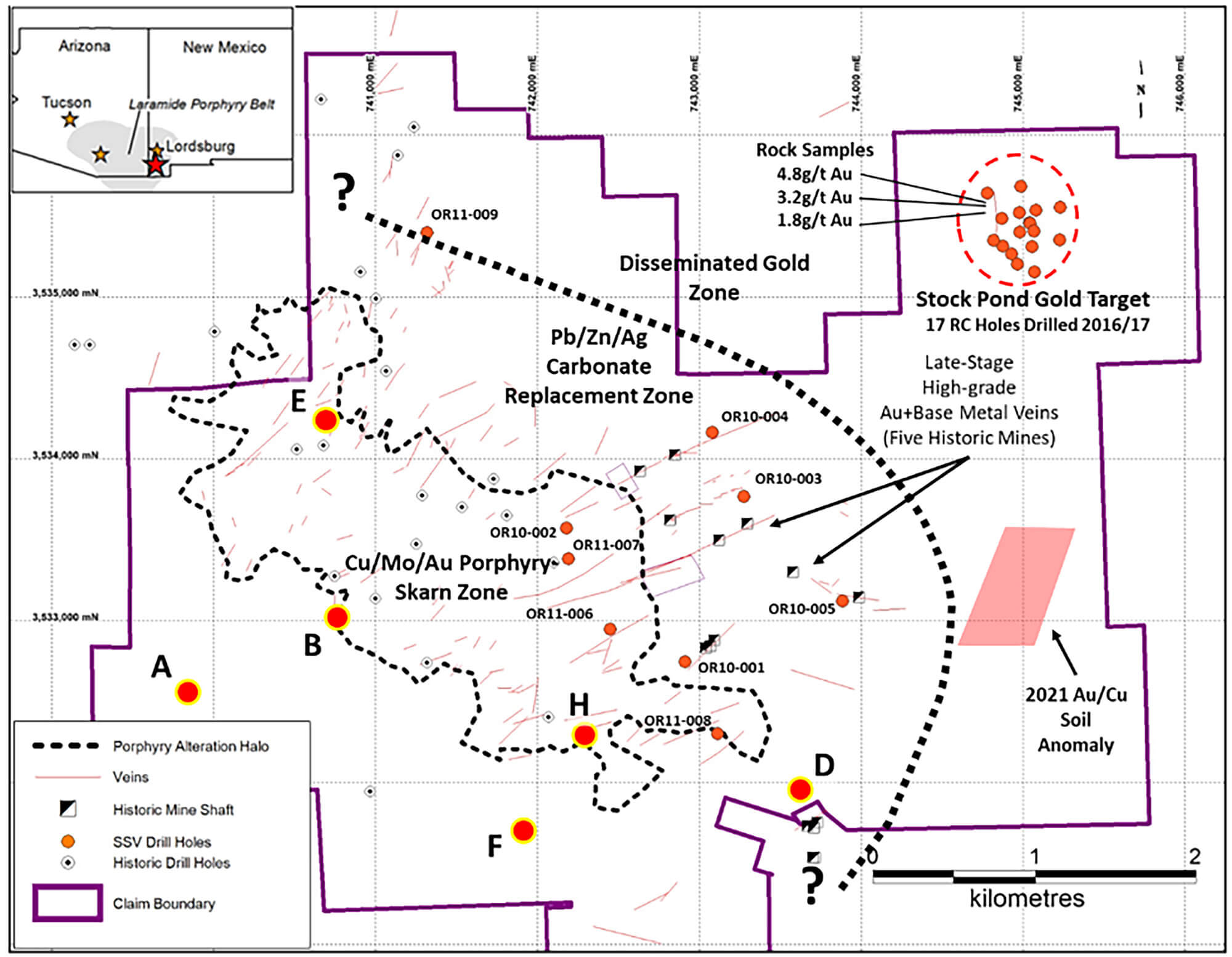

It has been a while since anyone has done any work at Oro as Southern Silver was very understandably directing all its resources towards Cerro Las Minitas, but it has now earmarked a portion of the budget for the Oro project. As a reminder, Oro consists of a series of Carbonate Replacement Deposits and the exploration theory of the company is that the clay mineralogy is actually overlying an unexposed porphyry zone.

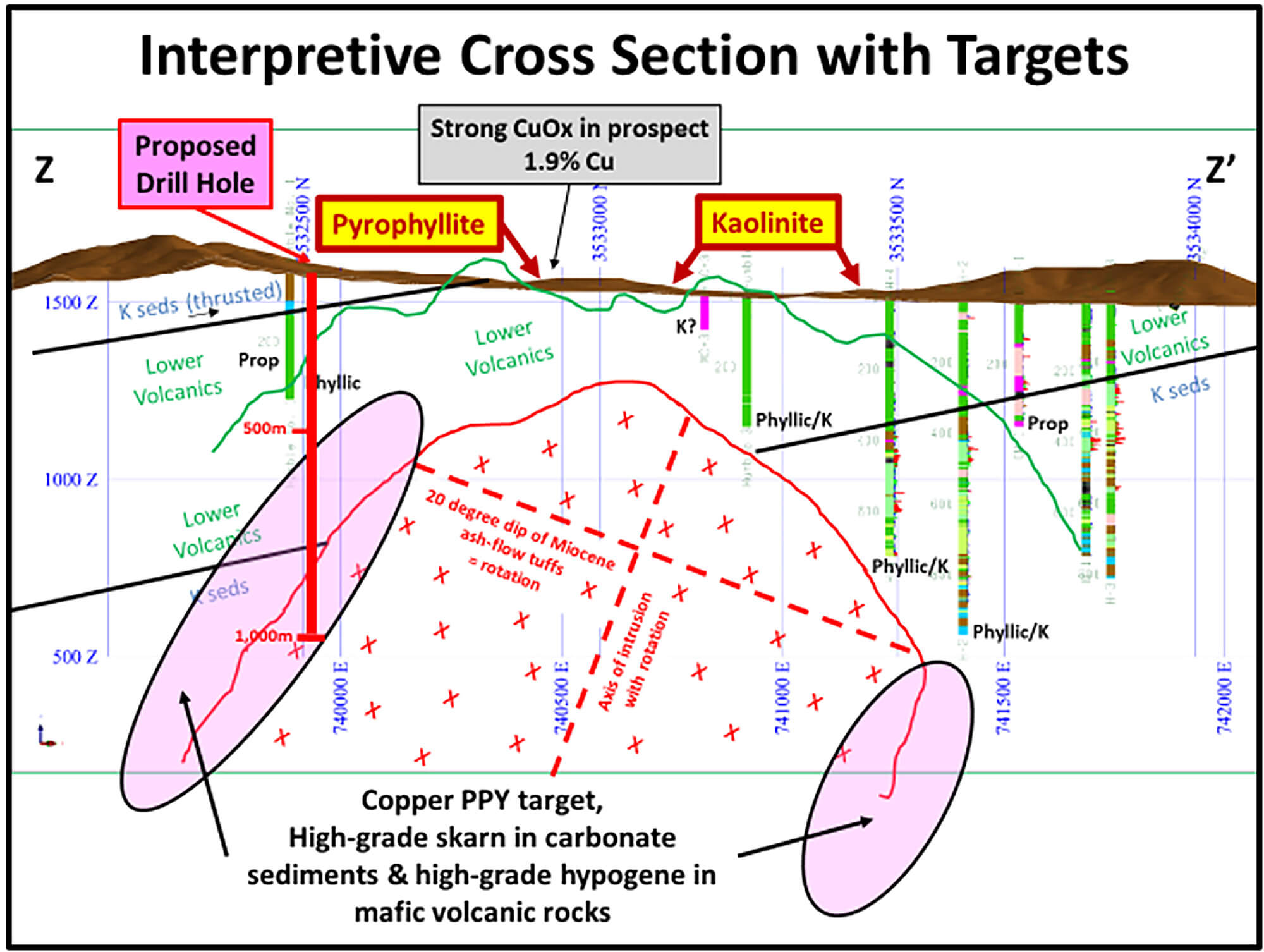

The drill program consists of six holes for a total of 4,000 meters of diamond drilling, so it’s clear Southern Silver is targeting mineralization at depth. One of the holes will for instance target an area about 1,000 meters below surface as you can see on the image below.

As these are deep holes, drilling will take a while and as the labs are still rather backed up, we don’t anticipate seeing drill results before the end of April.

One of the positive features of having an exploration project in New Mexico is obviously the weather as it’s easy enough to explore on a year-round basis. Southern Silver entered into an agreement to acquire the Hermanas project in the fourth quarter of last year, but it has already wrapped up its mapping and sampling program on the new project. Upon receiving the assay results from the lab, Southern’s technical team will assess the results and design (and permit) a maiden drill program which will likely start either at the end of this year, or early next year. At that point Southern Silver could be working on three fronts simultaneously, but we expect the company to spend its exploration dollars wisely and only invest in the assets and programs where it can get the biggest bang for its buck.

As a reminder, Southern Silver optioned the Hermanas gold-silver project from Bull Mountain Resources, a privately owned company. The company can earn full ownership of Hermanas by making US$182,500 in cash payments structured as Advanced Minimum Royalty payments to the vendors. Once the option has been exercised, Southern Silver will continue to make annual advance royalty payments to the tune of US$50,000 as part of the NSR the vendors will obtain on the project. That NSR has been established at 2% on the claims and 0.5% on the production coming from other zones within a pre-defined area of interest. Upon a total payment of US$10M in royalties (including the advance royalty payments), the 0.5% NSR will be extinguished while the 2% NSR on the core claims will be reduced to 1%. Given how the deal is structured with low cash payments, the downside for Southern Silver is low as it can just walk away from the project without too much damage.

Conclusion

While the focus of the company is obviously still very much on the flagship Cerro Las Minitas project in Mexico, Southern Silver is spending some of its exploration budget for this year on the ‘dormant’ Oro project and the newly acquired Hermanas project in New Mexico. And perhaps that’s not a coincidence as it could make sense to for instance advance these projects to continue to ‘carry’ the company should a transaction materialize at Cerro Las Minitas.

Of course, that’s just us thinking out loud, but we wouldn’t be surprised to see more interest in Cerro Las Minitas once a positive PEA will be published on the project. The appeal of the silver is quite easy to understand but let’s not forget the main driver of the project value comes from the zinc component. That was already the case at $1.25 zinc, but is even more so at the current zinc price of in excess of $1.50 per pound. As the project now contains 115 million ounces of silver and almost 2 billion pounds of zinc across all resource categories (with 42.1 million ounces of silver and almost 900 million pounds of zinc in the indicated resource category), the project now seems to have reached the critical mass.

The current market capitalization of Southern Silver is just around C$90M which means the company is trading at less than US$0.65 per ounce of silver (not silver-equivalent, but real silver) in the ground. According to our calculation, the after-tax NPV7% of Cerro Las Minitas may very well come in at around C$400-425M with additional upside potential and that makes CLM a very appealing zinc-silver project in the current commodity price climate.

Disclosure: The author has a long position in Southern Silver Exploration. Southern Silver Exploration is a sponsor of the website. Please read our disclaimer.