With Silver at $34 per ounce and gold at $3000/ounce, a lot of mining projects look substantially better than a year ago. Southern Silver Exploration’s (SSV.V) Cerro Las Minitas definitely is one of those projects. The most recent economic study, a Preliminary Economic Assessment, was completed in June 2024 and used $23 silver and $1850 gold as prices in its base case scenario.

While those were definitely valid prices back in the day, it’s now difficult to imagine a world with a silver price below $30 and a gold price below $2500 with spot prices for both metals trading firmly above those levels. And as we initially commented, Southern Silver’s flagship project definitely benefits from higher prices. Although it predominantly is a silver-zinc asset (those are the two primary metals), the higher gold (and copper price) obviously also help and we will review the impact of these higher prices in this update.

The company recently also announced it entered into an option to acquire the Nazas silver project in Mexico’s Durango state. An interesting addition to the project pipeline, and we sat down with VP Exploration Robert MacDonald to discuss the merits of that acquisition.

At the current metals prices, the after-tax NPV5% at CLM comes close to US$1B

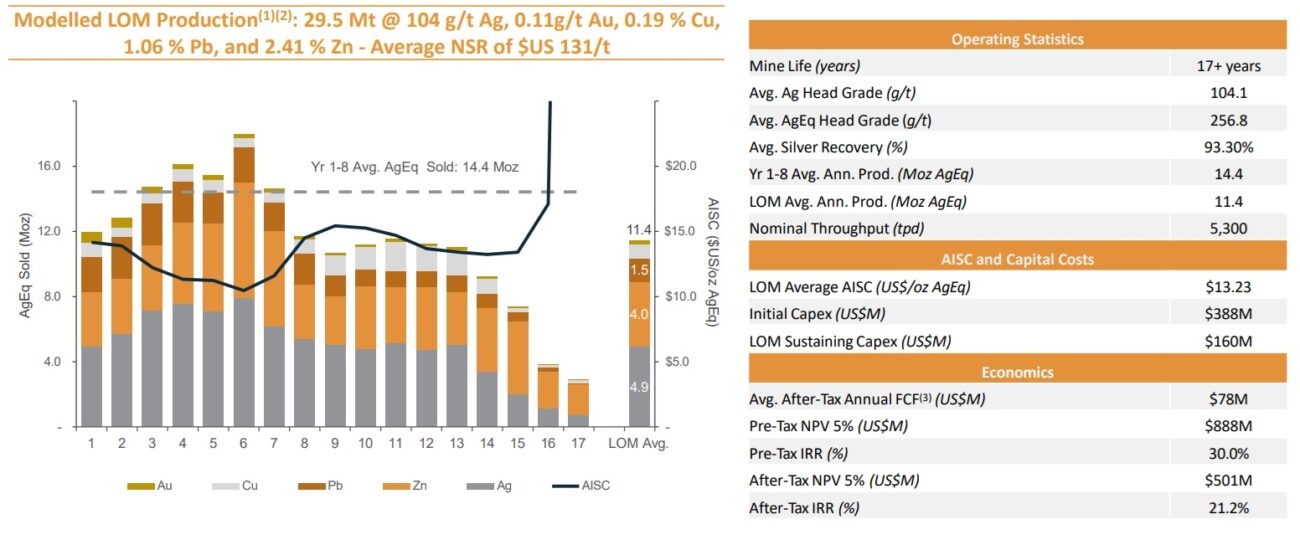

As we mentioned last time, the main purpose of updating the PEA in 2024 was to improve the economics, and Southern Silver definitely achieved the desired result. The mine plan was tweaked a bit and rather than focusing on a 4,500 tpd scenario, the company and its consultants settled for a higher throughput of 5,300 tonnes per day. That obviously meant the anticipated capex decrease didn’t occur but on a pro forma basis, the capita intensity improved. Whereas the capex per tonne of annual capacity was US$210 in the 2022 PEA, this improved to US$201/t.

The average daily throughput of 5,300 tonnes per day indicates the mine will produce approximately 11.4 million ounces of silver-equivalent per year, including 4.9 million ounces of pure silver.

Southern Silver presents the project and its operating costs on a silver-equivalent basis. While we are usually allergic to that, especially as the pure silver production of 4.9 million ounces per year is very respectable, we understand why, as silver represents less than 45% of the total revenue in the base case scenario. The net revenue generated from zinc sales is slightly lower than the revenue from silver sales, so Cerro Las Minitas could be seen as a primary-silver polymetallic project.

The total All-In Sustaining Cost (‘AISC’) is estimated at US$13.23 per ounce of silver-equivalent over the entire mine life but as you can see below, the average AISC in the first 14 years of the mine life remains firmly below US$12 and the AISC only starts to increase at the tail end of the operations when the output decreases.

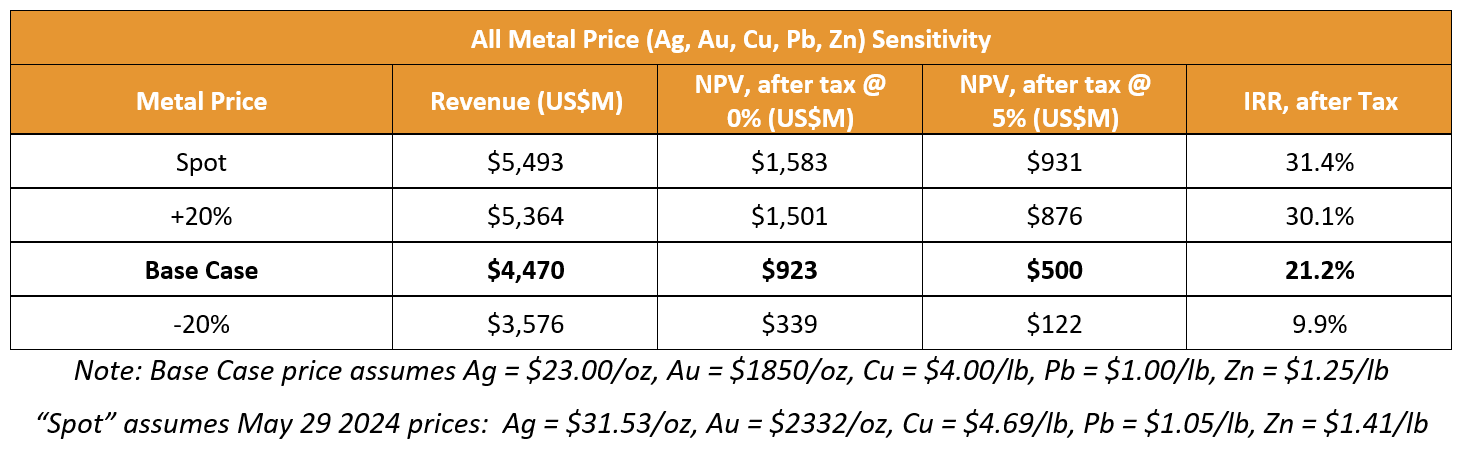

But what’s really interesting, is that the base case scenario in the 2024 PEA was based on a scenario with $23 silver and $1850 gold as main metal prices. The zinc price of $1.25 per pound is more in line with the current price, but it goes without saying that applying the current metal prices would provide a tremendous boost to the NPV and IRR of the project. As part of its PEA, the company published the table below.

It also comments the ‘spot case’ uses $31.53/oz for silver, $2332/oz for gold, $4.69 per pound for copper, $1.05 per pound for lead and $1.41 per pound as the main zinc price.

Gold and silver are obviously trading at higher prices than in the previous spot price scenario, while the zinc price is approximately 5% lower. The higher copper price has a smaller impact on the economics as the anticipated average payable copper production is less than 5 million pounds per year.

But if you look at the NPV5% on an after-tax basis in the Spot Case scenario above, the after-tax NPV5% increases to US$931M, which currently represents approximately C$1.3B. This means Southern Silver is trading at a substantial discount to the project’s NPV considering its market capitalization is currently just C$65M. The current spot prices are even higher than the ‘spot case prices’ used last year, so the after-tax NPV5% is now likely closer to or exceeds C$1.4B on an after-tax basis.

We would argue companies in this stage of the development curve are generally trading at 0.10-0.20 times the NPV, and a multiple of 0.15 would result in a ‘fair’ value of C$200M. That is of course quite arbitrary, but it’s difficult to understand why the company is currently trading at just 0.05 times the NPV. And as this is a 100% underground project, we can’t even point to the Mexican open pit issues as a main driver for the low valuation.

At $20 silver and $1 zinc, this project doesn’t work and won’t get built. At $30 silver and $1.25 zinc, the economics do make sense and the NPV is approximately twice the initial capex.

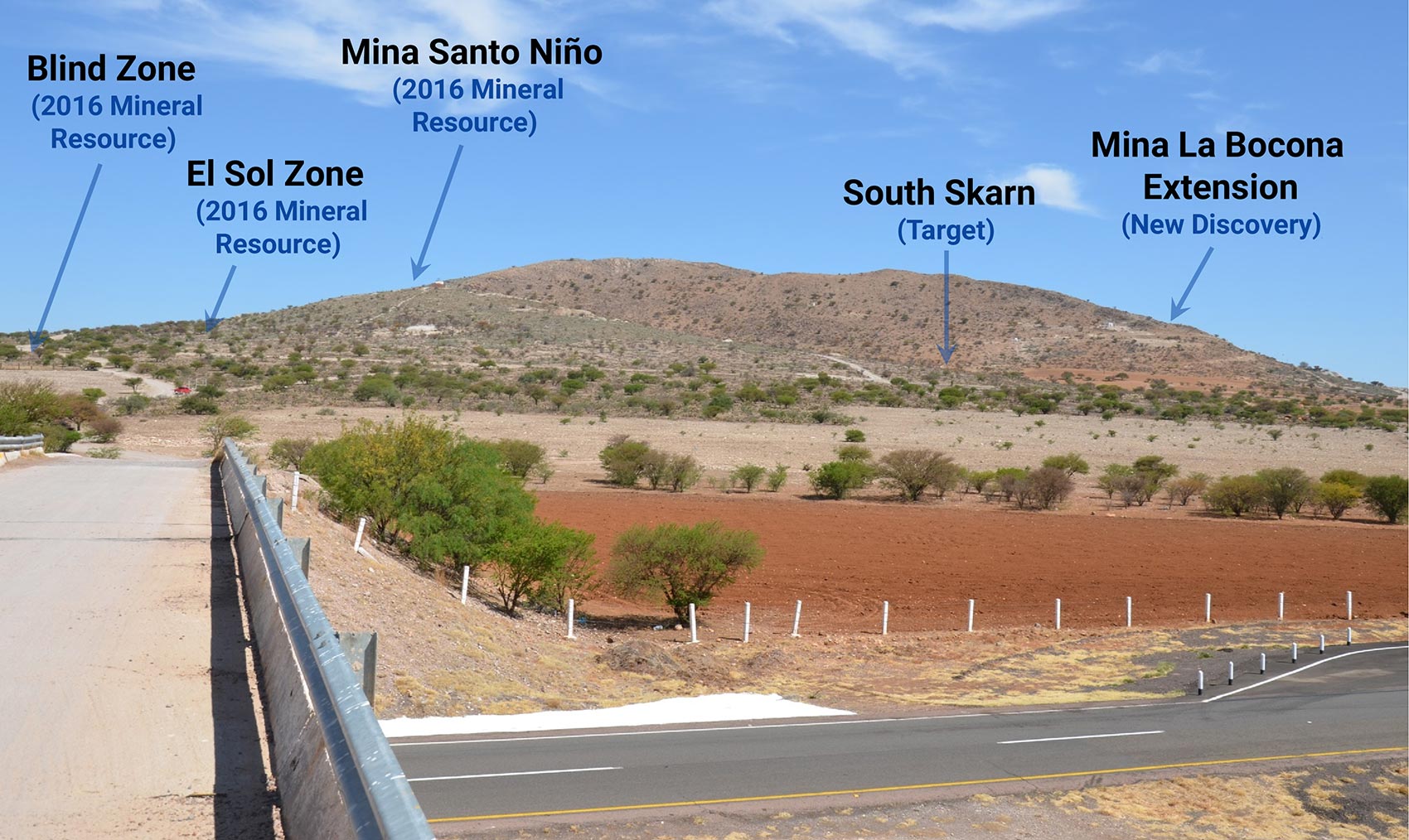

The recently acquired Nazas asset beefs up the Mexican pipeline

The company also recently announced it is expanding its asset base as the company recently signed an agreement with a private company to acquire full ownership of the Nazas silver-gold-lead-zinc property in Mexico’s Durango state. The project is located just 15 kilometers east of Endeavour Silver’s Pitarilla deposit, which hosts one of the largest silver resources in Mexico. According to Southern Silver’s technical team, the Nazas project has a similar host stratigraphy and mineralizing systems like Pitarilla.

Southern Silver can obtain full ownership of Nazas by making cash payments of US$130,000 over a three year period with semi-annual payments of US$25,000 after the initial six months and as long as the asset isn’t in production. The company also had to commit to drilling at least 8,000 meters during a four year period while the company will also have to cover US$25,000 in concession taxes. The seller will also obtain a 2% NSR on the current claims, a 1% NSR on any of the new claims ‘within an area of influence’ and a 0.5% NSR on third party owned lands within the area of influence. The royalty rates will be cut in half as soon as the seller receives US$10M in cumulative payments (including royalty payments and the pre-production cash payments).

We recently sat down with Robert MacDonald, VP Exploration for Southern Silver to discuss the Nazas project in greater detail.

Rob, what was the main reason to add the Nazas project to the company’s asset pipeline?

Several months ago, we were contacted by the vendors of the Nazas Property. We reviewed the data and quickly recognized Nazas as a first class project with the exploration potential to develop significant gold and silver resources, The project bolsters Southern’s asset pipeline will form a keystone component to the company’s future exploration plans.

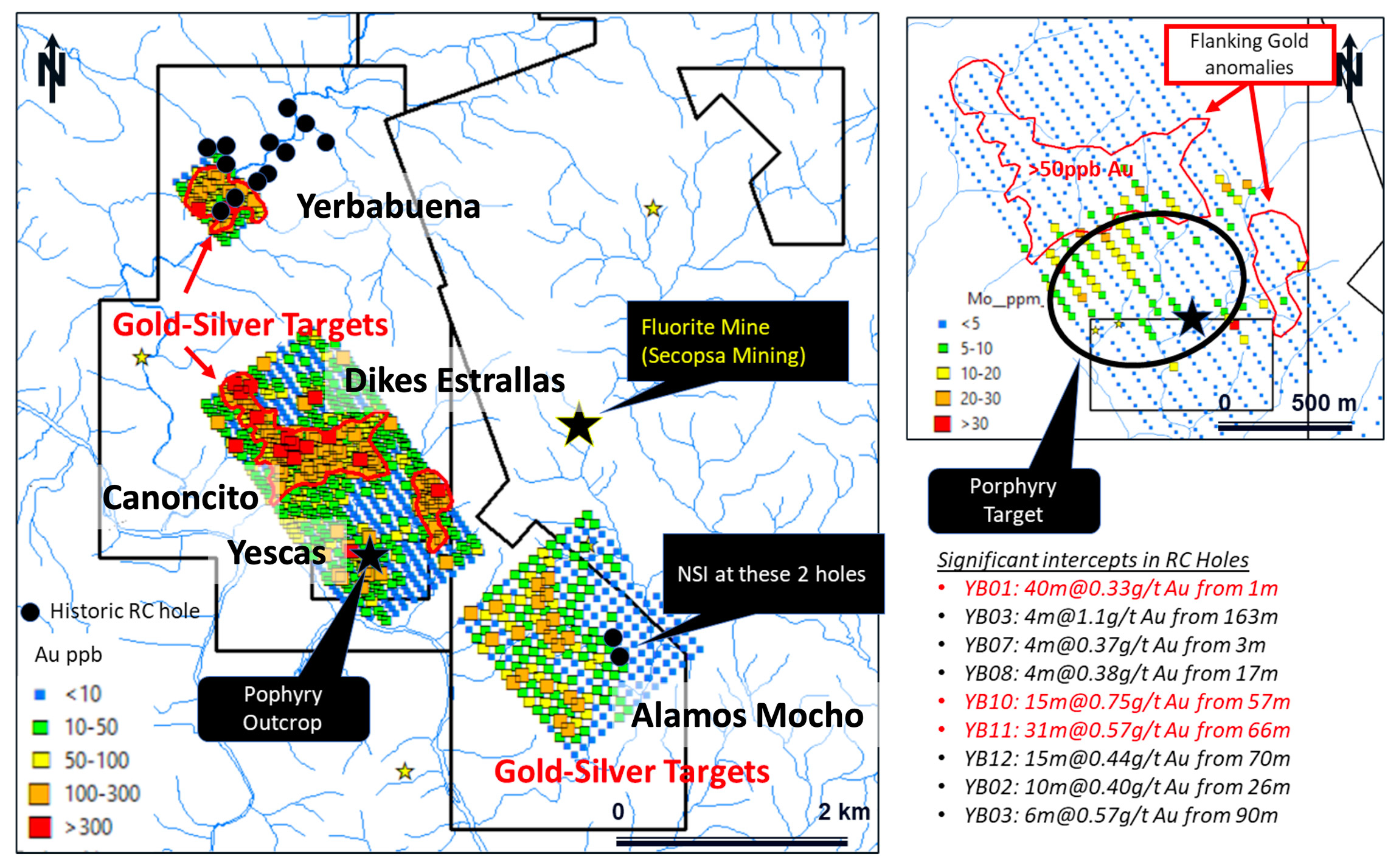

You have access to the data of 18 drill holes, how were the assay results and do they lend credibility to the claim Nazas looks like a Pitarilla-style deposit?

The 18 drill holes represent a preliminary test of only two of the seven targets identified on the property and support the concept of a large, zoned Au-Ag epithermal mineralizing system of a similar scale to Pitarilla. The mineralizing system at Nazas may be more deeply eroded and as a result appears more gold-enriched than Pitarilla with previous drilling intersecting numerous intervals of shallow gold mineralization including 40m averaging 0.33g/t Au, 15m averaging 0.75g/t Au and 31m averaging 0.57g/t Au. Overall, this is good news as it increases the project potential for significant low-cost, oxide-gold resources as one of several potential target deposit types identified on the property.

The acquisition terms are quite favorable as the main focus appears to be on the commitment to drill 8,000 meters within the first four years. Is the seller mainly interested in the NSR, because as it currently stands, there are only cash payments owed and not even a single share of Southern Silver is required to be issued to the seller.

We have optioned other properties from these vendors before, each with a similar deal structure. We like this style of deal as it gives the company the ability to earn 100% of the property and leaves the biggest consideration to the vendors contingent on success and ultimately the development of a mine. The vendors themselves, La Cuesta International, have historically had terrific success in identifying major mines and deposits throughout Mexico. These include the San Sebastian, San Agustin, Camino Rojo and Los Gatos mines and of course the Pitarilla deposit. We like to think that at Nazas, they have identified another major mining project.

Any plans for this year at Nazas?

We are still in the final due diligence phase of the acquisition and are in the process of assembling the necessary data to file a drill permit application. While we go all through this, we continue with data compilation, interpretation and drilling targeting.

There is a lot of data to look at, including several thousand surface samples, geological mapping and interpretation, drill data and numerous geophysical surveys to go through. Our exploration team continues review all of this data as we formulate a priority of targets and a plan moving forward. We will conduct site visits in Q2 and Q3 2025, complete any additional mapping and sampling to assist in the prioritization of targets and anticipate drilling the project in Q4 2025. The size of the drill program has yet to be determined, but I would expect to complete at least 3000 metres of drilling on multiple targets.

The recent placement filled up the treasury

Southern Silver announced its plans to raise money in the final quarter of last year, but unfortunately the financing window closed and as the flagship project is located in Mexico, Southern Silver was obviously also unable to tap into the active flow-through market.

At the end of January, the company made the difficult decision to reprice the financing to C$0.18 per unit (with each unit consisting of one common share and half a warrant with each full warrant allowing the warrant holder to acquire an additional share at C$0.28 during a three year period). Southern Silver initially also reduced the size of the placement to C$2.52M but the repricing made the unit so attractive (especially in a stronger silver market) the placement had to be upsized twice.

In the end, Southern Silver closed the financing in a single tranche at the end of June, issuing 19.9 million units for total proceeds of C$3.58M and net proceeds of around C$3.4M after taking the finders fees into account.

At the end of January Southern Silver had a positive working capital position of approximately C$0.8M so the recent financing has put the company in a much stronger position to advance its discussions with third parties to advance the project.

At the end of February, Southern Silver had approximately C$4.6M in cash and cash equivalents, and we expect the bank account to still contain north of C$4M right now.

It’s also interesting to see there are about 1.4 million options expiring soon with an exercise price of C$0.12 which will likely also bring in about C$0.17M and while that’s not a big ticket, it helps to cover the G&A for a bit.

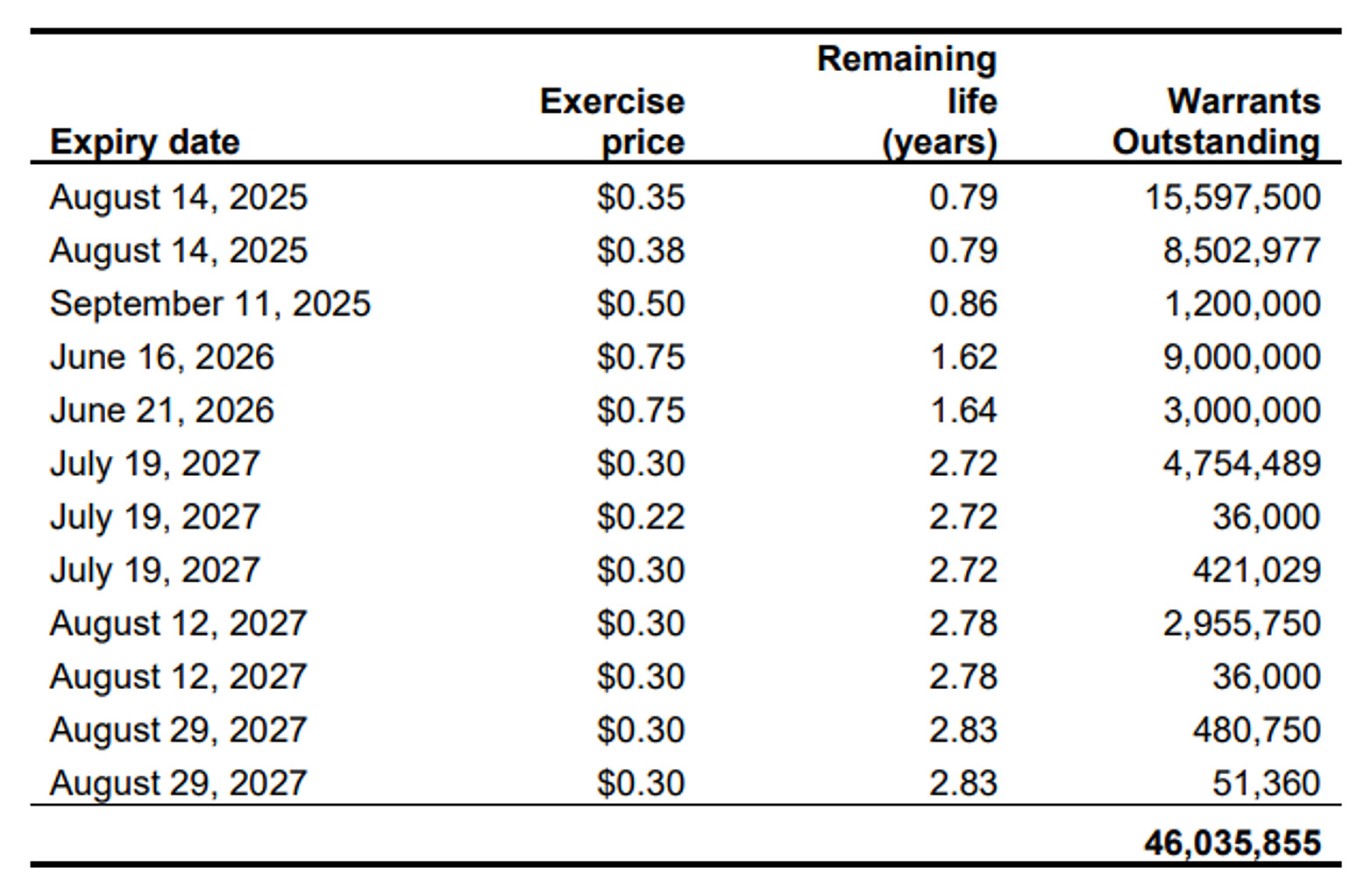

As shown below the company also has about 56 million warrants outstanding. The image below shows the warrant count as of the end of October, and does not include the almost 10M warrants at C$0.28 yet that were issued as part of the recent capital raise.

While virtually none of these warrants are currently in the money (except for the paltry 36,000 at C$0.22), a strong silver market and renewed interest in the project could potentially push the C$0.30 warrants in the money. Those 8.6M warrants could then bring in C$2.5M into the treasury while the almost 10M warrants at C$0.28 that were issued as part of the recent financing would bring in an additional C$2.8M if exercised.

That’s just daydreaming and wishful thinking for now, as none of the warrants are currently in the money. But additional strength in Southern Silver’s share price could bring these warrants ‘in play’ and provide additional funds.

Conclusion

Southern Silver’s flagship Cerro Las Minitas project still isn’t getting the recognition it deserves. Using a silver price of $31.5, a gold price of $2332 and a zinc price of $1.41 per pound and $4.69 copper, the after-tax NPV5% is a very impressive US$931M resulting in an after-tax IRR of 31.4%. As the Canadian Dollar has gotten substantially weaker versus the US Dollar, US$931M currently represents approximately C$1.33B in after-tax NPV5% at the aforementioned prices.

It will be interesting to the plan Southern Silver comes up with for the Nazas property and although markets generally don’t give companies full value for a second asset, it’s also not really giving the flagship Cerro Las Minitas project the valuation it deserves based on the PEA.

Disclosure: The author has a long position in Southern Silver Exploration. Southern Silver Exploration is a sponsor of the website. Please read our disclaimer.