As the sentiment in the gold and silver sector is improving, Tocvan Ventures (TOC.C) has been able to tap the market again as the company raised a total of C$2.5M in the first half of May. The cash was immediately deployed to kick off a drill program on the flagship Pilar gold and silver project in Mexico’s Sonora state. That drill program started in early April, so assay results started coming out soon after closing the capital raise.

Positive drill results, combined with good momentum in the gold and silver space and a stronger financial position, have provided a nice boost to the share price, which is currently trading around C$0.50 per share.

It’s also encouraging to see that most of the funds raised will be spent on the projects. We received the company’s Management Information Circular for the upcoming AGM, and CEO Sutherland’s base salary remained unchanged at just C$5,000/month in FY 2023 (and no bonuses were paid). That is by far the lowest base salary we have seen for a company of Tocvan’s size and activity level.

The assay results from the 2024 Pilar drill program are trickling in

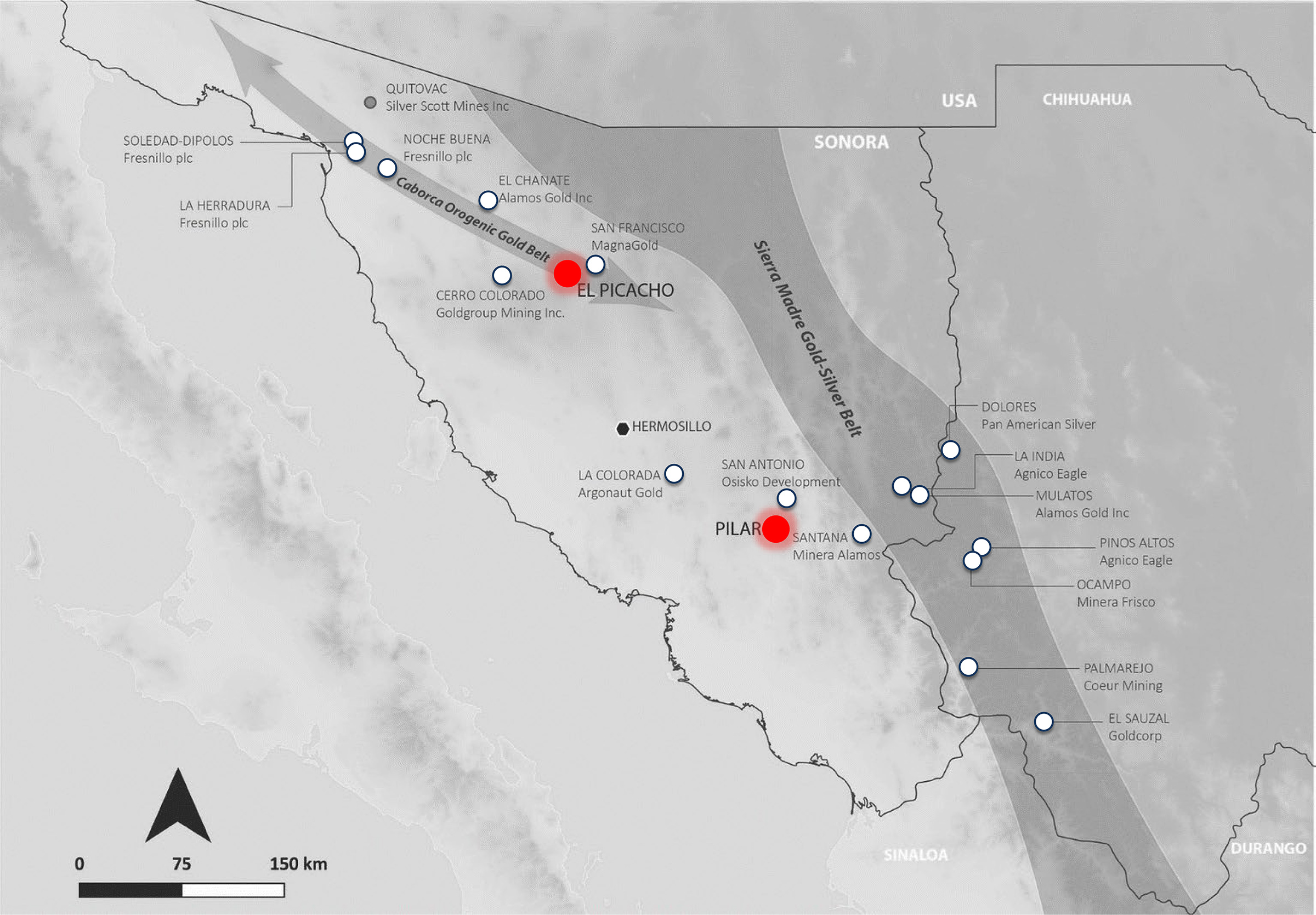

The Pilar project has changed dramatically from the moment Tocvan entered into the earn-in agreement with Colibri Resource Corp (CBI.V). The original plan was to initially establish a 51% ownership in Pilar and subsequent move closer to full ownership but market circumstances and the lack of availability of cash decided otherwise. In March of this year, Tocvan notified Colibri it would not be proceeding to the next phase of the agreement (which would have required a C$2M cash payment and the issue of a 2% NSR) and both companies formed a 51/49 partnership, which means Colibri will have to contribute 49% of the cash expenditures that will be incurred on the original claims.

It’s important to understand the 51/49 ratio is only valid on the initial claims of the Pilar project. All the land that has been staked and/or acquired by Tocvan subsequent to entering into the Pilar agreement is or will be fully owned by Tocvan.

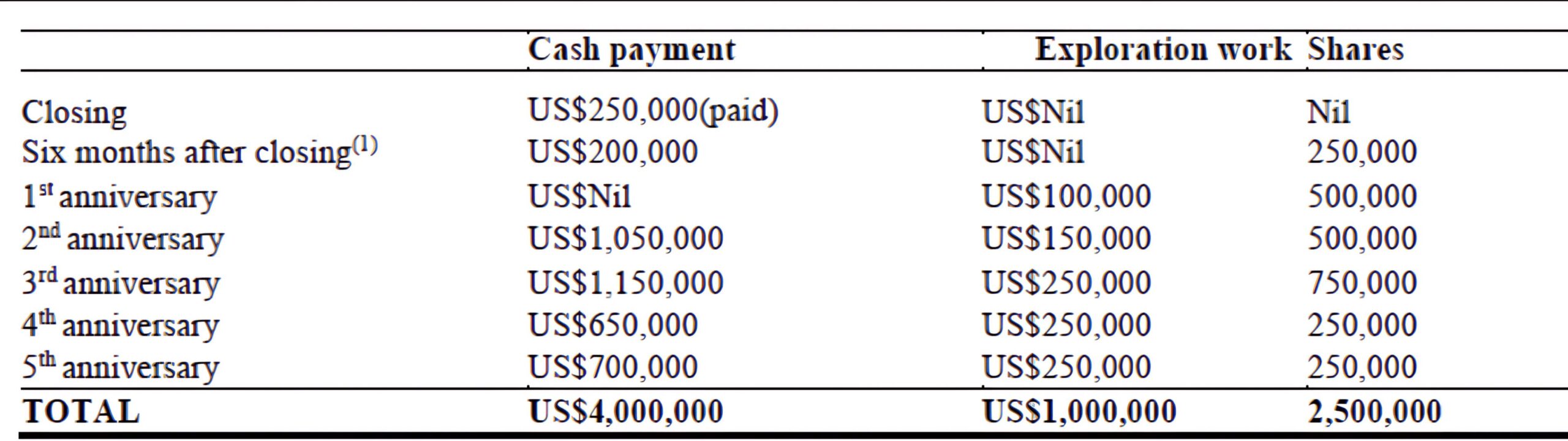

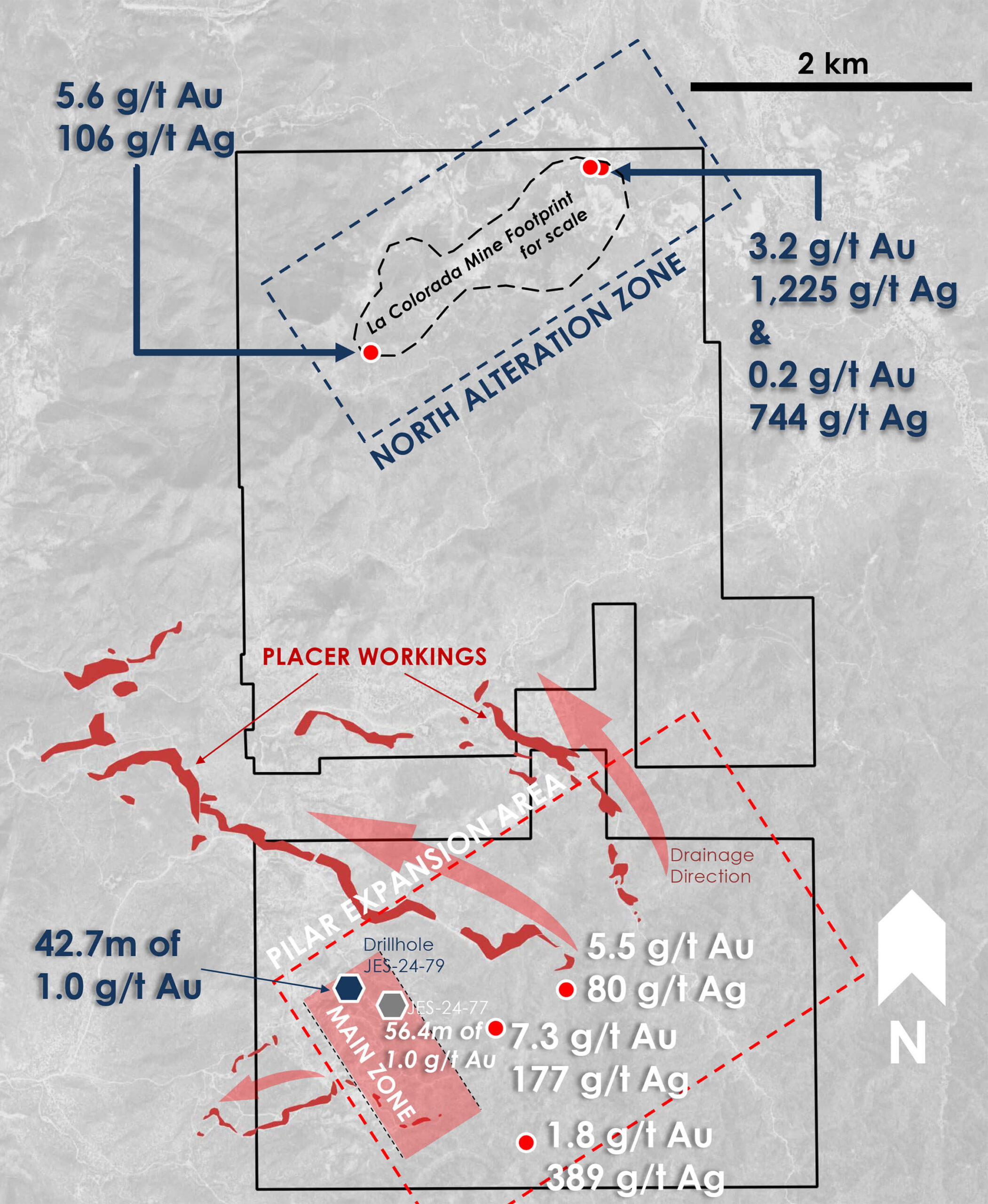

In the fourth quarter of last year, Tocvan massively expanded the size of the Pilar project. The initially optioned land package was just 105 hectares which is pretty tiny (especially if one would ever consider trying to develop the asset). The company added almost 2,200 hectares of land directly adjacent to and north of the optioned property. The acquisition comes at a cost. Under the terms of the agreement, Tocvan will have to pay US$4M in cash, issue 2.5 million shares and spend at least US$1M on exploration within a five year period while the seller will retain a 2% NSR.

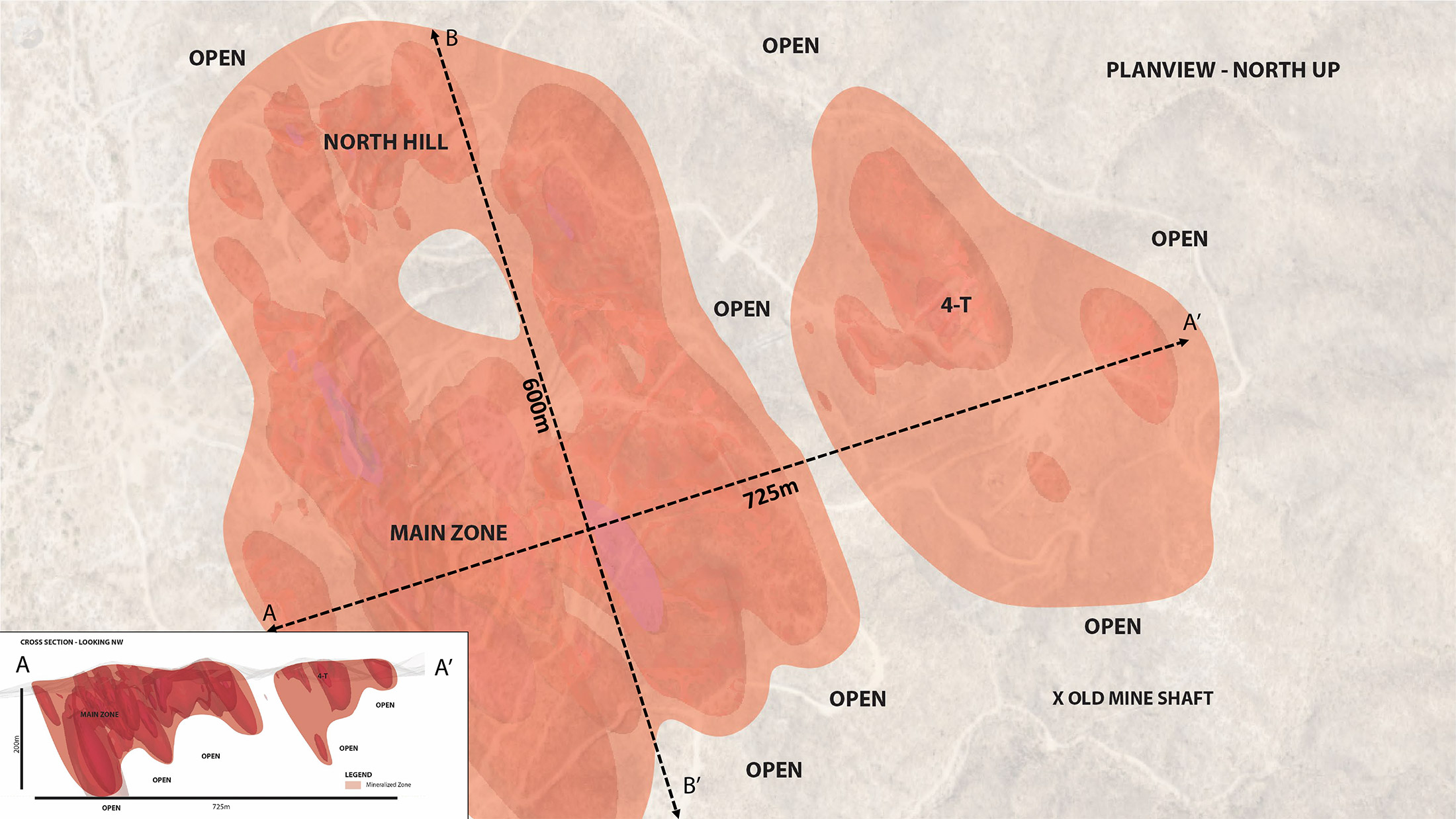

Before the 2024 drill program was kicked off, previous operators and Tocvan had already completed 23,000 meters of drilling, and Tocvan is hopeful to complete an additional 7,000 meters of RC drilling this year. The core focus is still on the Main Zone and that makes sense as we have the impression Tocvan would like to underpin its current market capitalization by releasing a resource calculation on Pilar.

As mentioned, drilling started at the beginning of April and the company started to release the assay results with the initial assay results exceeding our expectations.

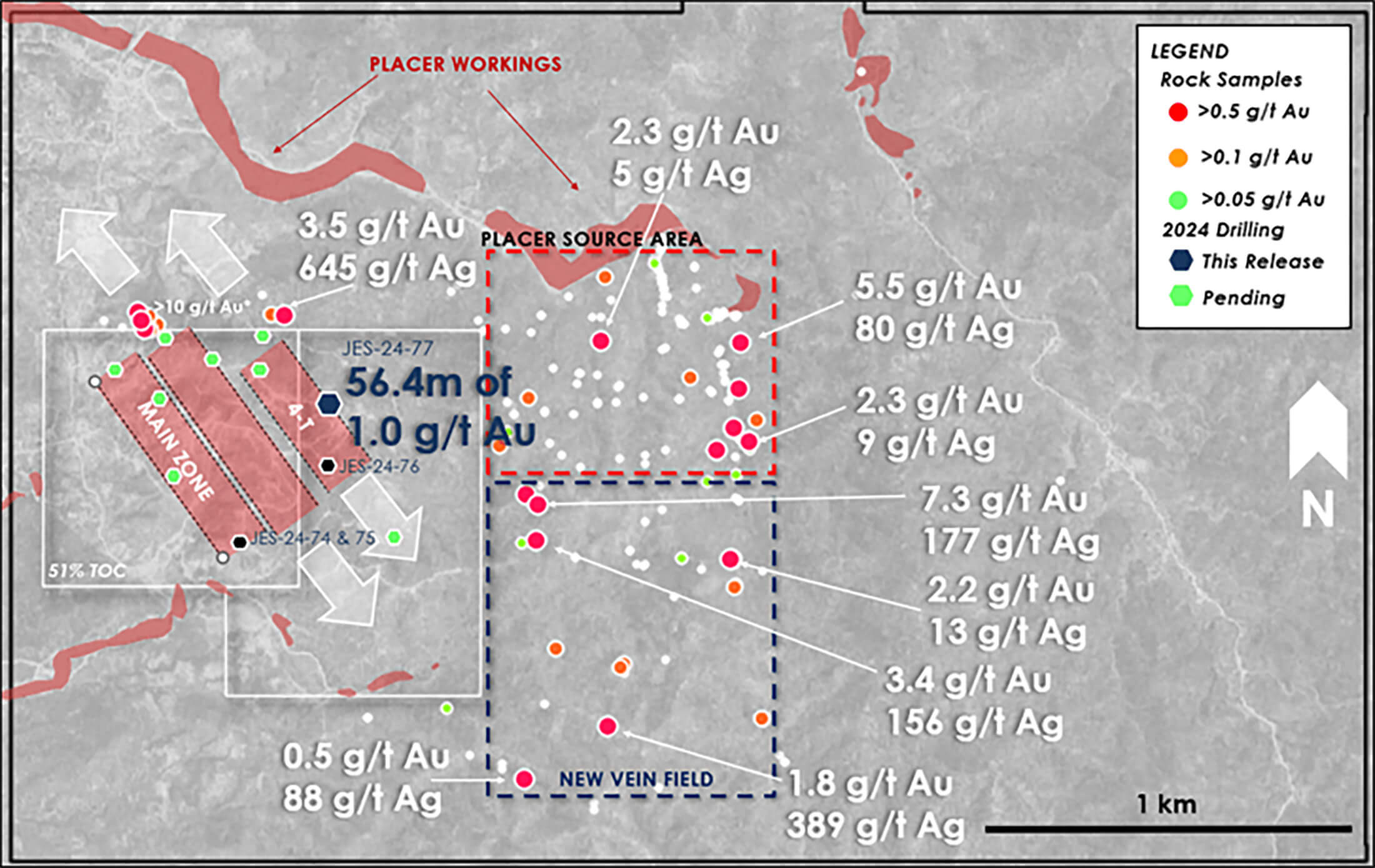

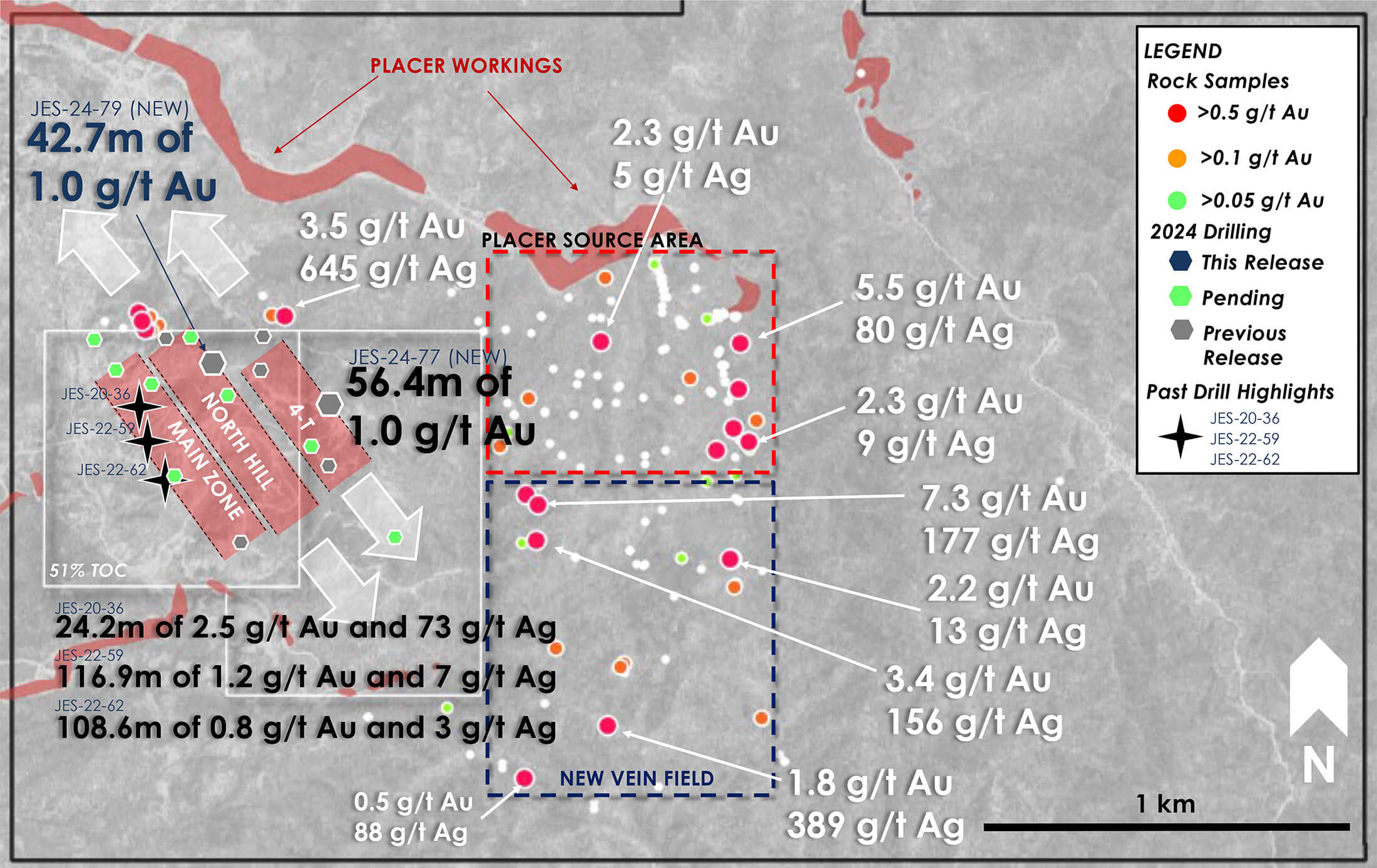

Indeed, in the first drill update, Tocvan announced the best ever drill interval encountered on the 4-T Trend, which is located a few hundred meters east of the Main Zone. The drill bit intersected 56.4 meters of 1.0 g/t gold starting at just 18.3 meters below surface. There also was 1 g/t silver but as the recovery rates for silver in heap leach projects usually aren’t great, the gold is definitely of greater economic importance to the project. It’s also important to note the entire length of the hole returned anomalous gold values with an average of 0.8 g/t over 76.3 meters, and the hole ended in mineralization confirming the additional exploration potential at depth.

The image above was published by Tocvan when the first drill hole of the season was released. As you can see, the red ‘area of interest’ in between the Main Zone and the 4-T Zone didn’t have a name yet. That changed two weeks ago when Tocvan released the assay results of hole JES-24-79 which returned the second best interval outside of the Main Zone with almost 43 meters of 1 g/t gold, including 3.1 meters of 10.9 g/t gold. The area in between the Main Zone and the 4-T Trend is now called the North Hill Zone.

All holes drilled so far were on the 51/49 joint venture land packagef held with Colibri Resource Corp.

Sitting down with CEO Brodie Sutherland

Pilar

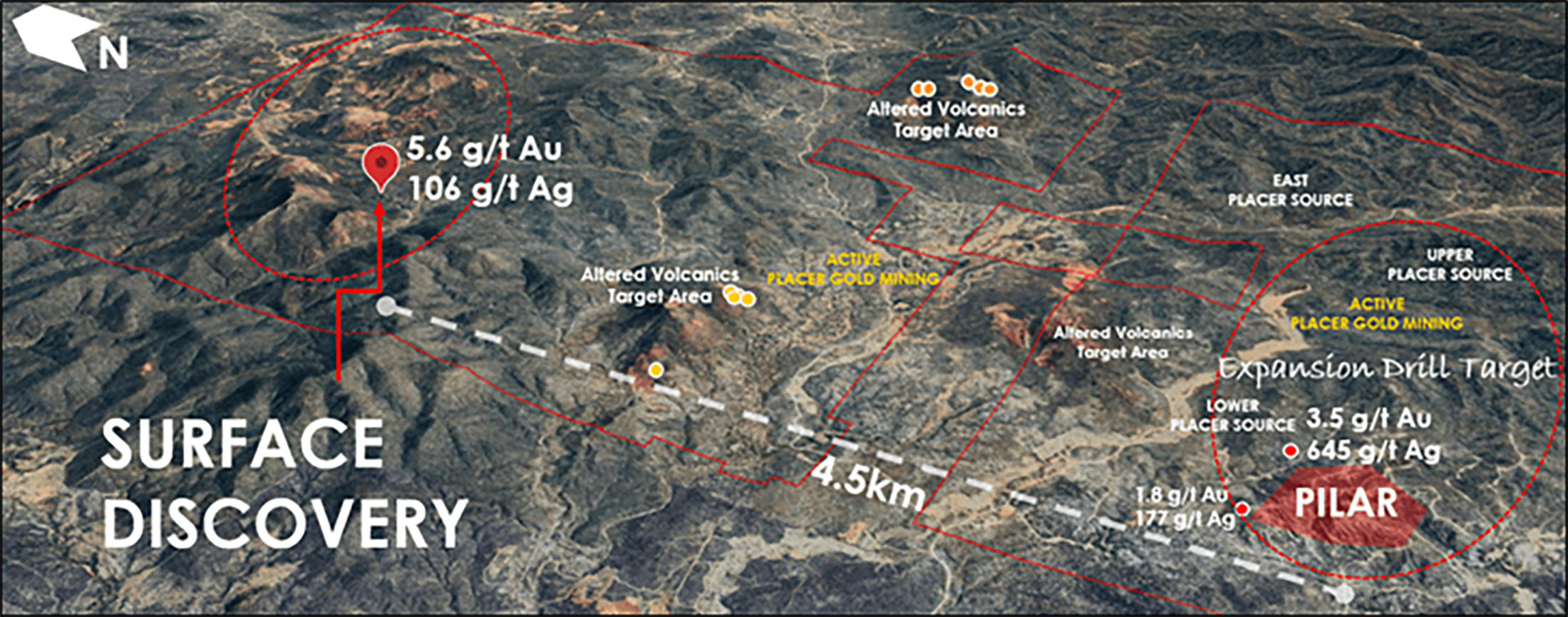

Let’s kick off with Pilar. Your initial press releases of the year were all focusing on Pilar and your ambition to further expand the mineralized system. Last year, you signed an agreement with a private vendor to add almost 2,300 hectares to the Pilar project and you have recently completed some ‘boots on the ground’ work on the new land package. You mentioned you detected a large gold anomaly measuring 1,500 meters by 800 meters, of which about 700 by 600 meters was directly related to placer gold mining. Did you use a bottoms-up or top-down approach here? Did you start from the known placer mining operations, expanding to see how the system evolves?

We always felt the exploration potential in the area surrounding Pilar was high. It was unlikely the mineralization just stopped and as we identified more parallel systems to Pilar, we wanted to fully evaluate that potential. After seeing the placer mining advance and increase its focus east of Pilar, we knew our model was correct but it needed to be proven with ground work. We have an excellent relationship with the placer miners who are primarily from the local community. Through conversations with them and the locations of their workings, the logical place to start exploration was immediately above them in the surrounding hills. Quickly we were able to identify new zones of high-grade gold and silver mineralization that looks very similar to what we see at Pilar, same host rock same epithermal style. As we extended our sampling to the south, zones of faulting and veining hosting gold and silver continued. It is still very early in its development but there is no doubt the footprint of the Pilar mineralized system is much bigger than previously thought. The other thing to note about the placer development leading us to this new location is much larger than any others in the area, significantly larger than those shedding off of Pilar’s Main Zone. We feel the size and grade potential of this new target area can be significant.

How are the sampling and mapping data helping you to define drill targets? Will you need to do any additional work or do you think you will have drill-ready targets?

We have flown LiDAR and detailed drone imagery over the area already. We are looking at airborne magnetics to assist in identifying structures. The mapping and sampling thus far has provided some strong targets, some with related artisanal underground workings that we can target with drilling very quickly. The added bonus of the placer mining is new road access, so getting a drill into these areas is very easy.

In your image (shown below), you have highlighted some of the samples. Can you elaborate on the ‘pattern’ you followed? And would you say the location directly adjacent to the placer area would be the highest drill priority?

The sampling was first pass reconnaissance so the pattern was simply to identify structures close to the new roads and start to walk them out. That leaves much of the areas in between still largely untouched for sampling. To infill the area we are looking at a grid sampling approach to identify anything in between. Based on what we are seeing I expect we will find more on surface mineralization through this area. There is also an additional 1.5 kilometers to the east of this area that has yet to see any surface sampling.

If we are not mistaken, your newly acquired 2,000+ hectares extend further to the east from the area shown on the image above. Have you done any work there too? Or is your immediate focus on the areas close to your ‘main’ Pilar zone?

No as mentioned above we have not done any work other than a quick recon up the existing roads to look at the geology. Placer mining has been present in that area as well and we believe it is highly prospective. The focus will be on the areas immediately adjacent to Pilar to start.

Minera Alamos recently announced the acquisition of a copper project in your back yard. Does this change anything for you?

We welcome more activity in the area. Clearly the work we are doing is creating more interest in the area as we feel it has been overlooked in the past. We know there is a long history of copper exploration around Pilar. Our focus is on the gold and silver potential which we think we are rapidly showing exists beyond Pilar.

How are the exploration circumstances in Mexico? Any issues with rig availability and rill costs? How much do you anticipate paying per meter of drilling this year?

If anything with the subdued markets exploration has gotten easier in Mexico with increased availability of personnel and contractors. We were fortunate early this year to lock in a long-term drilling arrangement with a local contractor, CANMEX. Our all in costs for drilling are $130 USD per meter, that allows us to complete a lot of work in a cost effective way. Lab turnaround times are also quick seeing most assays come back in 2 to 3 weeks, allowing us to make faster decisions while drilling.

How many meters would you like to drill, and will this be sufficient to get to an initial resource estimate on the project? At this point, it’s all about the balancing act between reaching critical mass and watching the treasury and shareholder dilution.

We have 7,000 meters planned for 2024 to outline a maiden resource estimate at Pilar. We may expand beyond that depending on other targets we want to evaluate. We have completed 2,000 meters of that drilling so far with the drill still turning on site today. We have always been mindful of dilution, not easy to be around for 4 years and have only 51M shares outstanding. As always, we will look to make the most with the capital we have.

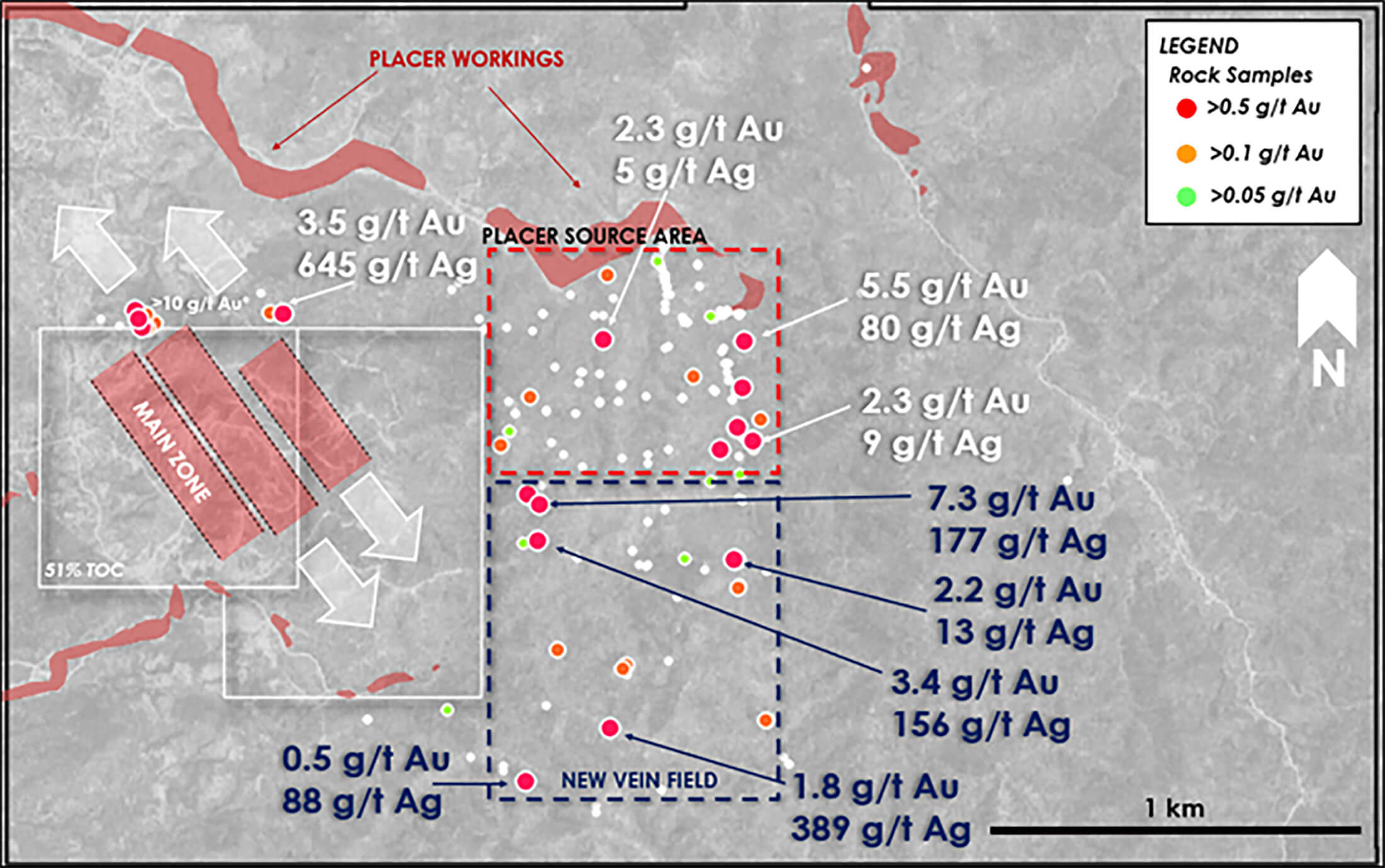

In your two drill updates you highlighted the strong results in a hole on the 4-T Trend and the North Hill Trend. However, in each release there were other holes that came up empty. On the Main Zone for instance, holes 74 and 75 didn’t encounter any significant mineralization. Does this mean the Main Zone is closed off towards the southeast? The images you used in your press releases don’t have arrows pointing towards the anticipated expansion areas, unlike the other zones on the project.

We feel the Main Zone trend to the southeast of drill hole 62, (108.6m of 0.8 g/t Au, from core drilled in 2022) does get offset, not completely closed off. Important to note that at surface where holes 74 and 75 were drilled sampling has returned excellent gold values, ranging from 1.2 to 5.1 g/t Au and up to 24 g/t Ag, so we know mineralization is present there. The holes were not complete ‘dusters’ or empty as they hit quartz veining with anomalous Au, Ag, As, Mo, and Sb. That indicates we are close to something more significant. These are exploration holes on the outer edge of known mineralization, often it takes time to focus in on significant mineralization. We can’t expect to hit exceptional oxide intervals with every exploration hole, but if new holes lead us in the direction we need to go, that is still a significant value add.

In the May 23 release, the assay results of four other holes were very weak as well. Those holes were drilled on the northern side of the 4-T Trend. What do the assay results tell you and what would be your next step at the 4-T Trend?

Again, we were encouraged by the alteration seen in the rock and the anomalous values of Au, Ag, Cu, As, Mo and Sb. Silver values up to 22 g/t, arsenic up to 4710 ppm are clear indicators there is a bigger system present that we are getting closer to. Surface sampling to the north returned 3.5 g/t Au and 645 g/t Ag, another strong indicator there is much more to uncover with the 4-T trend to the north. Similar values have been returned to the southeast along the same trend, so we just need to be persistent in targeting. The 56.4m of 1.0 g/t Au drilled recently is the best hole ever outside of the Main Zone, the drill density along this trend is low at the moment so we will continue to fill the gaps to determine the overall size potential.

So far you have seen the best of both worlds. Two holes contained really strong assay results with excellent gold values that would make any heap leach operator jealous. But you also had plenty of barren holes. Does this indicate the mineralized structure is perhaps more complex than initially thought? What’s your view, take and interpretation?

Pilar is complex and host to multiple mineralized events, that complexity is what makes it an attractive target and also is an important requirement for any robust mineralized system. All indications there is a much bigger picture to the size potential of Pilar. Epithermal systems in general host high-grade mineralization along narrow veins that can break out into wider vein sets and breccias. The fact that every hole continues to hit key indicators of mineralization tells us the system has a lot of room to grow. As we continue to drill we will no doubt hit more of the near surface, wide oxide gold intervals that will continue to advance the size of the project. I think if you look at the advanced stage exploration companies in the region drilling over 50,000 meters a year (Prime Mining, for example) and the results they are reporting, we are outperforming with our drill success. I like to think that is partly because of our talented team and partly because we have an incredible mineralized system at Pilar.

Picacho

Are you planning to do any work on Picacho, or are you solely focusing on Pilar this year?

We will do a bit of evaluation work at Picacho but the primary focus is Pilar. We have seen some interest from the major operators in the region towards Picacho and the surrounding area. We will see how that develops. The area is very prospective and early drilling has indicated at surface gold-silver mineralization exist there as well. Picacho is a great secondary asset for us providing more upside for us down the road.

You have a US$250,000 cash payment coming up for El Picacho, followed by a US$650,000 payment in one year from now. Is there any way to renegotiate the 2025 and 2026 payments, as they total US$1.65M on a combined basis?

Given our focus at Pilar and the surrounding area, we will look to adjust these payments over time. We have an excellent relationship with the owner and feel confident that can be achieved to align with our interests. Picacho has tremendous upside potential to delineate sizable, mineralized corridors with excellent access to infrastructure. The project will have an increased importance to us as we move Pilar forward, allowing for additional resource upside later on.

Corporate

What are the land-holding costs for both projects this year?

In Mexico, a biannual mining tax is paid on any active mining titles. Holding costs for us across both projects is about $60k CAD. Very manageable for us.

You recently notified Colibri Resources (CBI.V) you intend to officially form a 51/49 joint venture instead of pursuing full ownership of the Pilar Main Zone. Does this mean Colibri will now have to contribute 49% of the exploration expenditures?

As we advance the original Pilar holdings which consists of two mining titles totalling 105 ha, yes, Colibri will contribute to the exploration expenditures if they elect to participate. Hopefully they can participate to assist in the advancement of the project, if not, then our ownership percentage will adjust accordingly. We have 100% interest in, the remaining 2,100 ha area surrounding the original Pilar claims.

Is there a technical committee that makes the exploration decisions? Are you the operator, and are you earning a management fee on qualified exploration expenditures?

There will be a committee going forward for the advancement of work on the 105 ha, we have majority interest so can help direct the path forward. Same for management of the property as operator.

You just signed a new deal with Sorbie Bornholm to the tune of up to C$1.5M with the capital becoming available again in monthly tranches. Can you elaborate on the details of this round with Sorbie?

The arrangement is similar to past deals with Sorbie. Unit price was $0.35 for the share issuance. Capital is released monthly as 20 day VWAP goes over $0.48 more cash is released with no added dilution to the shareholders. Sorbie has been an excellent partner for us providing us access to over $3M CAD of funding over the past two years. We look to continue that relationship with this new arrangement. It has really given us an edge over other peer companies, knowing that we have monthly capital coming in, shelters us from the other challenges of needing to raise capital in this market.

As your drill cost is pretty low, what is your anticipated net working capital (or cash, if you prefer) level at the end of this quarter?

End of this quarter, we will have completed a minimum of 3,000 meters of drilling. After that, anticipating $1.8M of working capital to keep things rolling at Pilar. We will have another 4,000 meters of RC drilling scheduled for the fall months and a few other exploration initiatives ongoing across greater Pilar.

Tocvan raised a bunch of cash

As mentioned in the introduction, Tocvan closed a financing in the first ten days of May, raising a total of C$2.5M by issuing a total of 7.2 million units with each unit consisting of one common share and one warrant. Each warrant allows the warrant holder to acquire an additional share for C$0.50 during a three year period.

As the majority of the financing was taken up by Sorbie Bornholm under an agreement that sees Tocvan releasing shares on a monthly basis with the total cash inflow related to the share price when the shares are issued, the C$2.52M in gross proceeds versus the 7.2M shares issued are an ‘approximation’ of the total raise. A higher share price will work in Tocvan’s favor as it would have to issue the same amount of shares in exchange for more cash from Sorbie.

Conclusion

Tocvan Ventures is doing what it has to do: raise money and drill holes. The company would like to be in a position to start putting a resource calculation together by the end of this year so we definitely hope Brodie Sutherland and his team are able to complete the 7,000 meters of drilling they are hoping for. The drill results have been a mixed bag so far. Some holes were barren, but others recorded very strong gold values and grades most peers would be jealous of. It’s now up to the technical team to connect the dots, understand the structures and see if critical mass could be reached.

Disclosure: The author has a long position in Tocvan Ventures. Tocvan Ventures is a sponsor of the website. Please read our full disclosure.